Absolutely. Happy to be proven wrong. With such generous dividend, we can assume that Q4 would be strong (Management also hinted during Q3 call). Lets hope there is final dividend also announced in Q4 :). If they can execute their capacity expansion well I think GLS can turn out to be a great dividend paying stock at current valuations. Below are some of the reasons I see company getting valued very poorly.

1 - Parent group does not have a good track record of capital allocation.

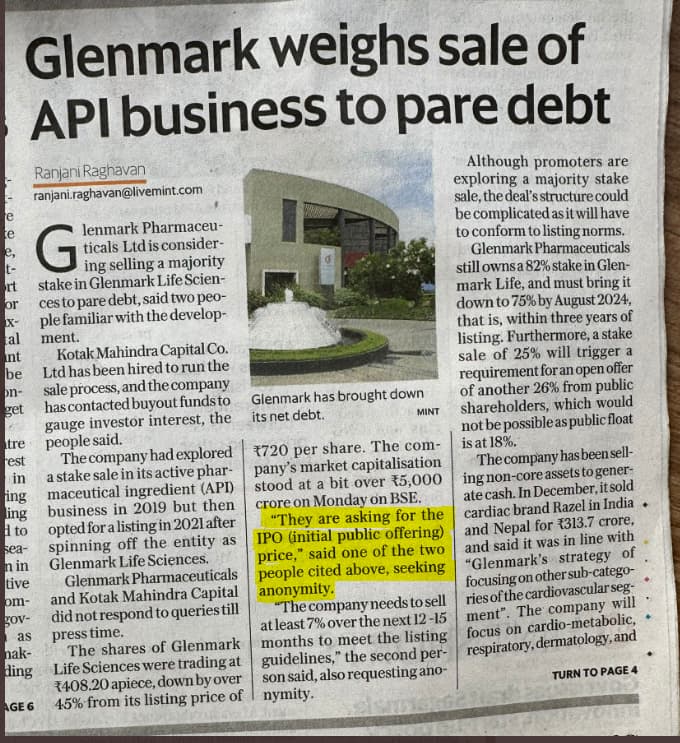

2 - Overhang of stake sell by the parent group. Currently they hold 82% and have to bring it down to 75% within 3 years of listing.

3 - Pending USFDA inspection of GLS facilities. Last inspections happened more than 3 years back as per management and its due anytime. I had sent an email to GLS around 3 weeks back to find out if there is any tentative date for the audits. However, there is no response. Since its a sensitive information, i guess there will not be any revert on the email. We will have to wait for Q4 result call to get some idea on that.

Requesting forum members to add more negatives which might be impacting the stock price.

Based on information shared by valued members it looks like things are not right at parent Gelnmark Pharma. GLS 40% of revenues come from orders from parent. GLS has reported decline in orders from parent which is a red flag. I wonder if parent company is not in pink of health then what is fate of GLS?

Note: Invested since last 2 years (3% allocation)

If in the tweet GLS is referred, then 2 points on which I disagree…

A. The GLS management is not going to scale up CDMO materially, they have guided “Aspiration to double % share of the business from current levels by 2027”…not significant I guess, in fact they may not even achieve this aspiration.

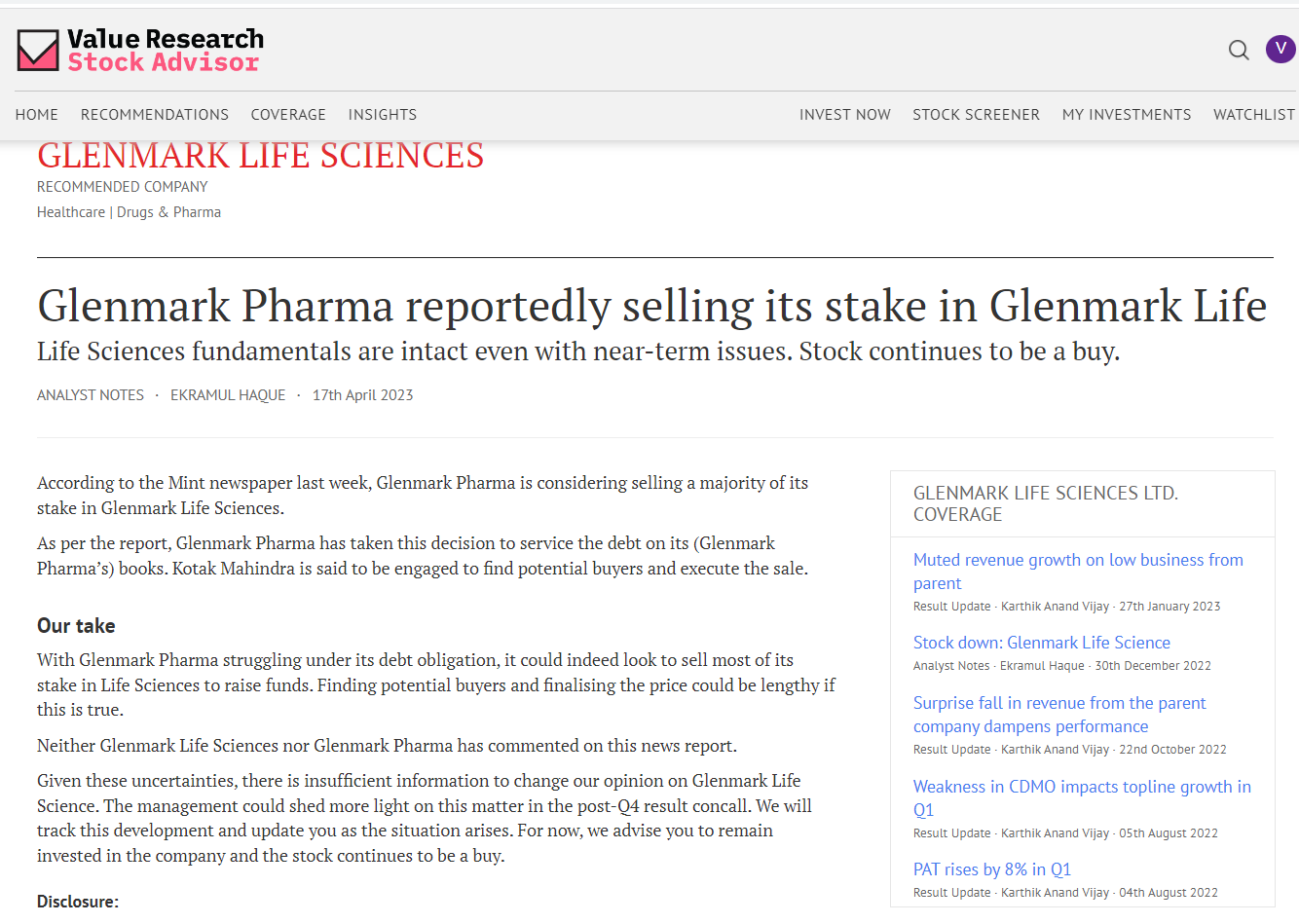

B. I doubt if Glenmark Pharma will sell majority of its stake, no doubt they are in need of money to pay off the debt, but will they give up a huge/controlling stake in GLS, I guess not.

Much awaited results and management conservative guidance makes this margin expansion vey good.

Gap from 500 to720 levels is likely to get covered in next few months and that will pave way for management to offload their partial stake to FII.

Long term capex plans in Solapur will take care of future growth of 3/4 years.

Yes good results. But need to note that the revenue contribution from parent Glenmark Pharma has gone to 42% when it was actually trending downwards towards 30%

QoQ, business from parent has increased by 70 crores from 160 to 230 crores whereas business from other customers has just increased by 10 crores from 380 to 390 crores

This was well addressed by Management in their earnings call. Any company will look for best margins and best capacity utilization. GLS achieved their best margins in this quarter .Cash flows and cash position post 21rs dividend indicate inherent strength of their business.

Good to hear Madhu Kela also asking questions in earnings call.

A year back or so there were times when GLS calls were not attended by enough audience. In fact, I still remember the operator had to literally wait so that someone can ask questions. Today Madhu Kela joined. That shows a changing trend. While you cannot get excited after just one quarter results, if GLS can execute what they are guiding for then the stock is available very cheap and at a very good dividend yield.

GLS did not have any DII holding till Q4FY23. I suppose that will change once the Q1FY24 shareholding pattern is out.

Nothing wrong with that. They expect it to remain around 30% of the overall sales in medium term and it will go even lower in longer term as their external business is growing well.

Instead of focusing on quarterly gyrations so much, its better to look at slightly longer term trends. Glenmark Pharma business had dipped by 40% in Q2FY23 due to inventory correction on part of Glenmark Pharma, and the current sales revival is just normalization of inventory.

More importantly, non-Glenmark business is growing at a healthy pace and it is very diversified across a large customer base, which gives them some degree of pricing flexibility.

It didn’t look like a quarterly gyration as the 4Q revenue from GLP is the highest in 2 years and has deviated hugely from the declining trend, which was promised by management in almost every quarterly con-call since listing. They have give a 15% guidance for next fiscal and are very sure that contribution from parent will be substantial. This would mean, the share from non parent customers would have very muted growth. In any case, we need to wait and see the trends in next two quarters at least

Management never promised that revenue will start declining from Glenmark Pharma, they have consistently been saying that over a period of time % contribution from Glenmark Pharma will come down i.e. incremental growth from other customers will be higher. This trend is also visible in the last couple of years.