Hello,

Since the thread was started by @gnaveen4 (Mr Naveen Gupta) only he can edit it. I have tried to elaborate on the company as below, hoping it would suffice the forum standards and expectation. If it does then I would request you to reopen the thread.

Company background

Glenmark Life Sciences (GLS) is an active pharmaceutical ingredients (API)arm of Glenmark Ltd. Glenmark launched the API manufacturing business in Kurkumbh in Maharashtra in 2001-02. In 2019, the API manufacturing business was spun off into a different company with sole focus on API business. Glenmark Life Sciences is engaged in the development/manufacturing of high-value, non-commoditised APIs. The company has a portfolio of 120 products that have a market size of $142 billion. These products are used in various therapy areas, such as central nervous system, cardiovascular, diabetes, anti-infective.

The business

API business:- The API business is engaged in manufacturing high-value raw materials to make drugs for chronic problems like heart disease, stroke, cancer, diabetes, and chronic lung disease. Due to chronic nature of these diseases, they require regular medication. The API business accounts for around 90 per cent of the company’s revenue (FY21). As of FY21, it had a portfolio of 120 molecules globally, sold APIs in India and exported APIs to multiple countries in Europe, US, Latin America, Japan and RoW.

CDMO business:- Besides developing its molecules to be sold as APIs, it also researches and develops specific client requirements on a contract basis. This business is called contract development and manufacturing operations (CDMO) and brings in 8 per cent of its business. It provided Glenmark Pharma, its parent, favipiravir, a covid drug that the former sold last year. The company has scaled up its contract development and manufacturing operations (CDMO), accounting for around 8 per cent of the overall revenue in FY21.

Capacity

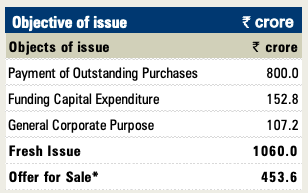

Currently, it has four manufacturing facilities at Ankaleshwar, Dahej in Gujarat and Mohol, Kurkumbh in Maharashtra with total installed capacity of 726.6 KL as of FY21. It plans to use the part of the proceeds from the IPO (152 crore) to expand the capacity of its existing API facilities by 28 per cent. These are expected to come online by 2023

It also plans to commission an 800 KL greenfield facility in Solapur, Maharashtra, in the next three to four years. This new facility will double the current capacity of the company. This facility is intended to be funded from internal accruals and debt financing (if required).

Glenmark’s addressable market size

The global API market is valued at $181 billion (in 2020). Of this, Glenmark’s 120 products have a market size estimated at $142 billion. This addressable market is expected to grow by about 6.8 per cent over the next five years to $211 billion by 2026.

Strengths of the company

Non-commoditised/Niche products:- The company’s API portfolio comprises specialised and profitable products, including niche and technically complex molecules, which reflects GLS’s ability to branch into other high value products. The future growth of these products is expected to remainstable driven by the increasing prevalence of non-communicable diseases (including heart disease, stroke, cancer, diabetes and chronic lung disease),

growing demand from the regulated markets for drugs indicated for hypertension, diabetes and cancer, and an aging population.

Quality track record:- Since 2015, its facilities have been inspected by the USFDA and other global regulatory authorities 38 times. However, it has not received any warning letter or import alerts from these authorities.

High ROCE business:- GLS has earned a high return on capital employed (ROCE). ROCE averaged at 33 per cent in the last two years.

No Debt:- Out of the IPO proceeds, it will pay Rs. 800 crore to Glenmark Pharma as payment for outstanding purchase consideration for the spin-off of the API business into a new company, so the company is debt free. The repayment of debt to its parent will allow it to use more of its free cash into building R&D and higher capacities.

Risks/Concerns:-

The parent, Glenmark Pharma, buys 40 per cent of Life Sciences’ sales. It will take some time to see how this plays out.

It sources 40 per cent of its basic raw material from China, so there is a geopolitical risk here as well.

Glenmark Pharma, the parent, does not have an outstanding track record. Its revenue grew at an annual rate of 7.5 per cent over the last five years while net profit compounded at 5.5 per cent. It has a debt of Rs. 4200 crore. There is a possibility that the parent could further dilute its stake to pare down its debt.

Glenmark Life Sciences operates at risk of regulatory restrictions. The fact that it cleared all inspections in the past is no guarantee it will continue to do so.

The company’s top 10 products accounted for 66.36% of FY21 revenue. If market growth in key products declines, or if profit margins on products sold

in key products decline, results of operations could be adversely affected.

Management

Dr Yasir Rawjee (MD & CEO) has headed Glenmark Life Sciences since 2019. His last stint was at Mylan as the head of Global API operations. He has worked at the SmithKline Beecham Pharmaceuticals, GlaxoSmithKline and Matrix Laboratories Ltd in his two-decade career.