Delivery % is up because of upcoming 10.25 Rs dividend ![]()

Company does have valuation on its side, so that could be another factor.

1 Like

A comparison between Divi’s and GLS…taken from respective ARs.

Divi’s has a total of 39 drug master files (DMFs) with USFDA and 25 CEPs (Certificates of Suitability) issued by EDQM authorities. Divi’s has filed for a total of 41 patents for generic products.

GLS…As on June 30, 2022, we had filed 436 Drug Master Files (DMFs) and Certificates of suitability to the monographs of the European Pharmacopoeia (CEPs) across various major

markets (i.e. the United States, Europe, Japan, Russia, Brazil, South Korea, Taiwan, Canada, China and Australia). As on June 30, 2022, we owned or co-owned 76 granted patents in several countries.

Divi’s also mentions the following…

“Oncology, Immunology, Anti-diabetics, Neurology, Cardiology, Anti-coagulants, Respiratory & Pain will be the top 8 segments by value. The therapy areas with the highest forecast spending in 2026 are oncology, immunology, and anti-diabetics, followed by neurology. Oncology is projected to add 100 new treatments over five years. Generic share will rise, driven by, ongoing market dynamics around the use of medicines, the adoption of newer treatments, the impact of patent expiries and new generic competition, will all contribute to the market growth for the next five years.”

Both the companies look interesting.

4 Likes

Company has received GMP certification from ANVISA for 7 APIs manufactured at its Dahej facility. Finally some good news

1 Like

Sir I am unable to find this news in exchanges. Can you share the source of this news. Stock is making new lows day by day. Is there anything that market knows nd we don’t?

Regards

It was posted on their official LinkedIn page.

Thanks for this. It’s actually quite surprising that they haven’t reported this to the exchanges since IMO results of regulatory inspections (pass/fail) has an impact on stock price movement.

1 Like

When I googled Anvisa, I see it’s Brazilian FDA. Perhaps Brazil is not a very big market for GLS to report to exchanges

Any specific reason sudden spike in price spurt in volumes after a long time. Did not find any thing in any media channels.

Parent Busienss : Degrowth from 41% to 27% this is due high base effect which was due to covid related drugs (30-32% Long term target)

External Business is doing good (Japan, Europe, LATM)

Mid Term: low to mid teens growth

This year will be muted

Margins are maintained (28-31%) , this is mainly due to process efficiencies that lead to cost reductions

5 Likes

3 Likes

9e69fa3c-e575-4997-a596-b46ac5ef7de5.pdf (1.7 MB)

I am looking for fresh investments in GLS and looking for comments on my below assumptions:

- Being conservative investor I always look for some dividend yield just to ensure cash being made by company. At 5.65 yield and 11 PE with 40 ROCE it seems a Great value buy.

- China opening should support in Raw Material and China Sales

- Dahej capacity addition to boost growth in coming quarters with additional support from Ankleshwar intermediate capacity addition

4.Greenfield capacity addition of Solapur in coming 2-3 years give good growth visibility

I am a novice in interpreting API business and its headwinds/tailwinds and investment thesis is purely based on Valuepickr and other online resources.

I am comfortable in Holding this stock for long-term unless any structural issues crop for Company or business.

I feel below Rs 400 its a safe buy and intend to keep sipping till build my significant exposure.

Am I missing anything on GLS ? Or its a similar case like ITC whose time is yet to come.(Invested in ITC at 165-180 and exited at 340 , IRFC at 24 and exited at 35 and now trying to find investment thesis in API company but unable to conclude as lot many companies like Divis, Laurus,… in same field and No much MOAT like IRFC or ITC)

5 Likes

For Dividend yield, I feel we will have to wait for couple of years to see if they can sustain that yield. They have degrown this year compared to last year so I assume the dividend will be less and the yield will not be 5.65% or even 5%.

Yes, there is margin of safety at CMP but markets still see it as Glenmark company and not an independent entity to give a better valuation.

Disc - Invested at higher level. Did transactions in last 30 days.

1 Like

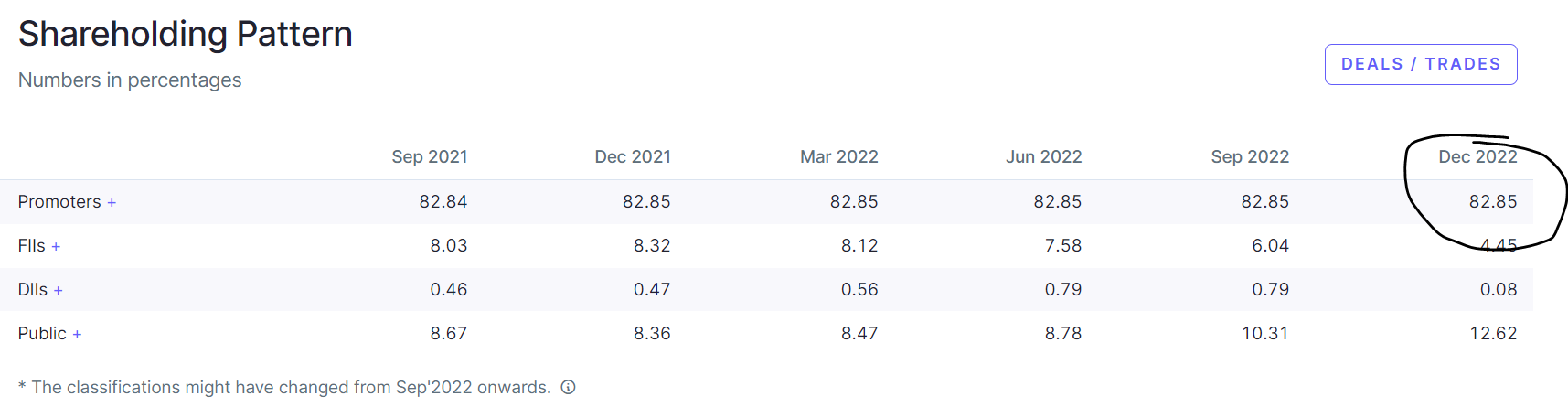

Can someone pls comment on the share holding pattern ?

My understanding was promoters group can hold only a max of 75% of the share holding. How does GLS is holding 82.85%. Is there any exception to this rule? Please help to understand.

Your understanding is correct. For new listings (IPO), SEBI gives a time period (3 yrs I guess) by when the promoter should bring down the holding to 75%

this would happen only in the listing of IPO time and for the tentative deadline period. You could watch vedant fashions, mazdock, irfc etc… to witness this analogy.

BABA RAMDEV is facing similar issue where in they needed to off load shares of RUCHI SOYA to being at par to 75% but they did not abide by the timeline and has the trading has frozen…so there is some time period

Dividend is maintained and lets hope if the results are also as per guidance and capacity expansion is on track.

1 Like