Yes, GLS management had always maintained that revenue share from GLP will keep going down and it was trending towards 25% but turned on its head and is close to 40% in Q4. Now they say the parent’s contrinution will continue to be significant which to me looks like a reversal of stands. We will get the correct picture in FY24.

(Btw, I removed that line from my previous post)

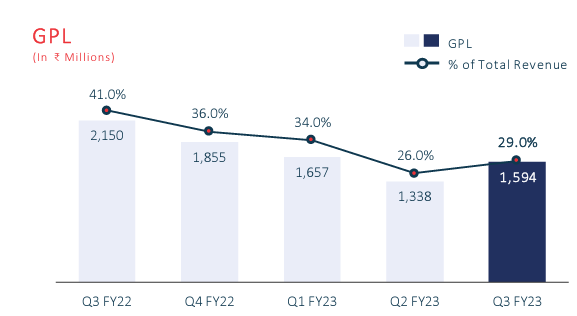

41% in Q3FY22 - went down to 26% in Q2FY23 - Is at 37% in Q4FY23

Hello I’m new to the company and I’m trying to understand what is the issue with this GPL and non GPl revenue. Why is that ppl are finding it bad for GPL revenue has gone up? and why the company is so cheap a 33% roce business at 13 PE. Anything to do with slow down in overall growth?

I think we could assume that the company will grow 15-19% CAGR for the next 4-5 years. My reasoning is based on management’s commentary, Dr. Yasir said "right now, we are around INR150 crores, INR170 crores, right, which contributes around 7%, 8%, right, So when we want to double it to 15%, the rest of the business is also going to grow, right, more or less double. So in order to sort of make it 15% of a roughly doubled business, INR150 crores will have to go to INR600 crores, okay. So I mean, that’s not bad, right, taking INR150 crores to INR600 crores in about four years to five years time. I mean, that’s what I would say. So to go beyond that, I think, it’s possible. I mean we won’t rule it out. But then, just like in whatever we do, we want to be very measured in terms of what we are able to see and how the overall global environment also shapes up.

@Souresh_Pal this may partially answer your query on future growth

what I understood from concall is next 2 quarters will be very good from topline point of view. But for full year 12-14% guidance is conservative becz they have good visibility for H1FY24 but due to some unforeseen reason if H2FY24 slows down then won’t be good. All the engines of margin fired up so margin expansion might not be on the cards. So next 2 quaters will be epic

Overall, I was highly impressed with the NPMs of this company for a business of this nature. Additionally, consistency in growth over the last 4 years as well as management of OPM margins has been good, far less volatile from single API companies. It has nowhere near the scale or the price leadership of Divis, but the company’s margin profile and sales growth make me wonder if it should still be valued where it is.

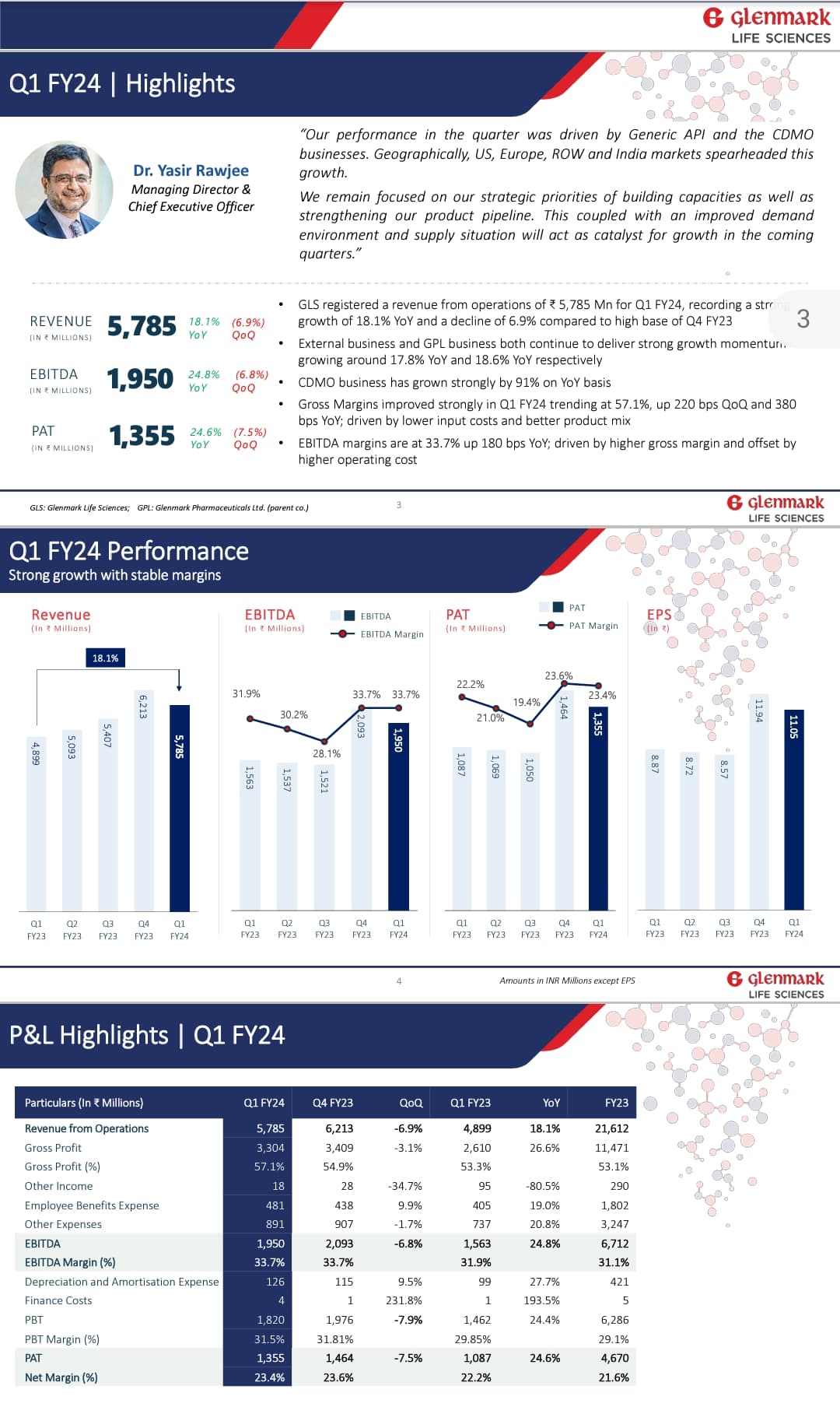

Additionally, the guidance in the last concall was very interesting. Management is guiding for 31% odd OPMs which are impressive and in fact several participants including Mr Madhusudan Kela were checking if it could match Q4 at 33%. Either ways we should get a solid 30%+ margin profile + topline growth with the capacity coming on line.

Eventually it was a company with what seemed like strong growth tailwinds including topline/bottomline, strong charts and volumes, at sub 14 PE/~3x book, with ~30% OPM, ~20% NPM and 4% Div yield and went ahead with the investment last week.

Disclosure: Invested in self and family accounts. As I am invested I am biased towards the company. I am not a SEBI advisor and this is not investment advice.

Yes. This was undervalued for quite some time. I have been tracking for the last 2/3 years.

But took the initial position after the trigger of Glenmark planning to sell its stake in it.

This was the TRIGGER / CATALYST the market was waiting for.

Please check my previous post a few days back.

dr.vikas

Thanks for the information. But I can’t see the whole article as it requires a subscription. But I have found the same kind of article on Business Standard. Posting it below for the benefit of the community.

So what is everyone’s opinion? In my view Nirma has no expertise in running a pharma business. While Sakhmet is just a PE firm. Is long term investing justified in GLS? Please share your views.

A PE firm (KKR) bought JB Chem from its erstwhile Indian promoters some 4 years back and the company got rerated like wow…

In GLS case the high promoter holding makes the threat of upside capping for minority investors should the new promoters opt for a delisting … There is a rule in sebi which compels someone who buys beyond a certain threshold to also announce open offer… the resulting minority stake post this offer may become even more redundant as to vote against any delisting proposal… This could be Nirma’s thought process given that they delisted some years back…

Still some room may be left for a quick upside as the deal finalizes keeping in mind the issue price of GLS when IPO happened and a possibility that current promoters would atleast settle for something in that range/above that to give up their stake …

A PE fund (Sekhmet) could persuade Glenmark to only sell controling stake and remain invested being non promoter minority stakeholders, then a growth story from long term perspective is a possibility…

If KKR (whose name was also mentioned in the first leak of prospective suitors) or similar PE fund scoops it up, it would be a compelling proposition for long term investing…

The necessity for the Parent to look for suitors for GLS became public knowledge around the time when Glenmark agreed to pay up 87.5 million USD (roughly 740 crores INR) to settle US lawsuits… I read somewhere that this is to be paid in 2 annual installments… In its books it has a net debt of 2880 crore INR as on March 31, 2023.

The continued dividend from GLS helps in the interest servicing of the parents loan. A minority stake sale of GLS would be enough to take care of the financial outflow obligation arising from the US settlement.

The Promoter of Glenmark had also replied to a question in the recent Q4 concall that to the extent they need to adhere to the settlement, they would explore stake sale in GLS…

As long as the valuations continue to improve…

Q1 results on friday and the concall therafter would continue to interest me… post Q4 results there was Madhusudan Kela asking the management questions… he was interested to know if the dividend continues going forward, the projected margins in the coming few quarters and so on and so forth… no question on management change from him…

if Nirma acquires Glenmark Lifesciences, it won’t be its first pharma rodeo. And if you think about it, this was right in Karshanbhai Patel’s wheelhouse. He was a chemist, remember?

.

In 2004, it took a bet on an ailing company called Core Healthcare that made IV fluids. Nirma thought it could disrupt the game with its low-price strategy once again. But here’s the thing. Nirma soon found that the pharma game was very different from consumer goods. Price isn’t the only factor that pushes buyers to turn to you. There’s the quality factor too. Other small pharma players were able to match Core’s prices. And Nirma couldn’t turn things around. Big Pharma continued to reign supreme.

.

Meanwhile, it spun off the pharma division. Gave it a new name — Aculife Healthcare. And began to sell medical devices.

.

So yeah, you could say that pharma runs in Nirma’s DNA. And with the recent success it’s seeing in cement, maybe it decided to double down on pharma too. And this isn’t coming out of the blue.

.

Last year, there were rumours that Nirma was eyeing a buyout of Maneesh Pharmaceuticals. Just a couple of months ago it acquired Stericon Pharma, a company that makes contact lens cleaning solutions and eye drops. And now there’s this news of buying Glenmark Life Sciences.

Good Results and better commentary on future growth prospects by management. Growth in high margin CDMO business and future capacity utilizations are likely to result in stock moving above its IPO price in coming months. Only overhang is parent company stake sale and new management rumors.

Current margins and future growth makes current PE around 16 very attractive and a PE re rating to 25 likely in coming one year.

My views are biased as I am invested from lower levels.

A general question:

If any company acquires the 83% stake of promoters from GLS, then they need to make an open offer equivalent to 25% of the stake they buy from promoters? (which essentially would mean that the open offer would have to be for the entire non promoter stake then?)

I don’t think the deal will go ahead with such low valuation. Looks more like a clickbait article. Glenmark will find some other way to reduce their debt or look for higher valuation for GLS.