Hi Sougata,

Thanks for the heads up. I didn’t know that, will keep it in mind in the future. The report was available on BQ but behind a paywall. Anyways, I have removed the link from my previous post.

1 Like

Most brokerage/analyst reports from Indian companies is available on Trendlyne. Here is the link to GLS reports.

1 Like

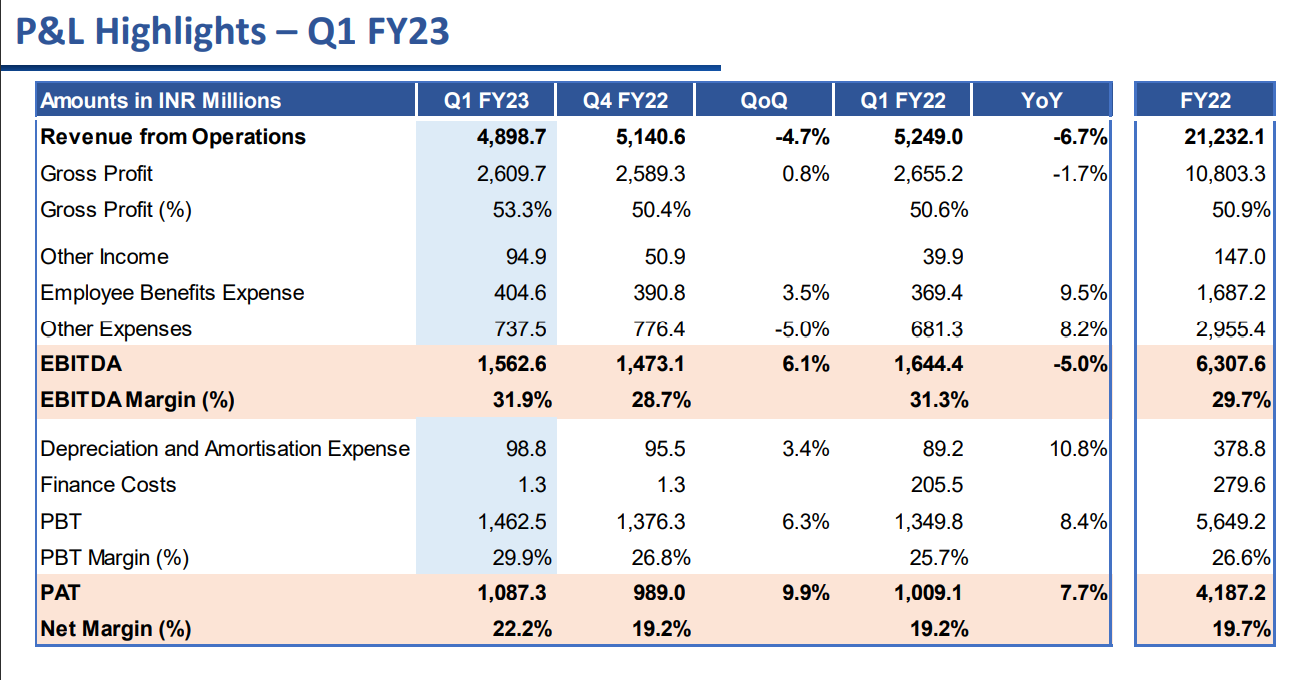

- Margin expansion by 300bps is a pleasant surprise

- Strong profitability in a tough environment. Shows resilience of business

- Marginal decline in topline due to covid sales. Ex-covid sales, reasonable growth.

- CDMO degrowth was a miss

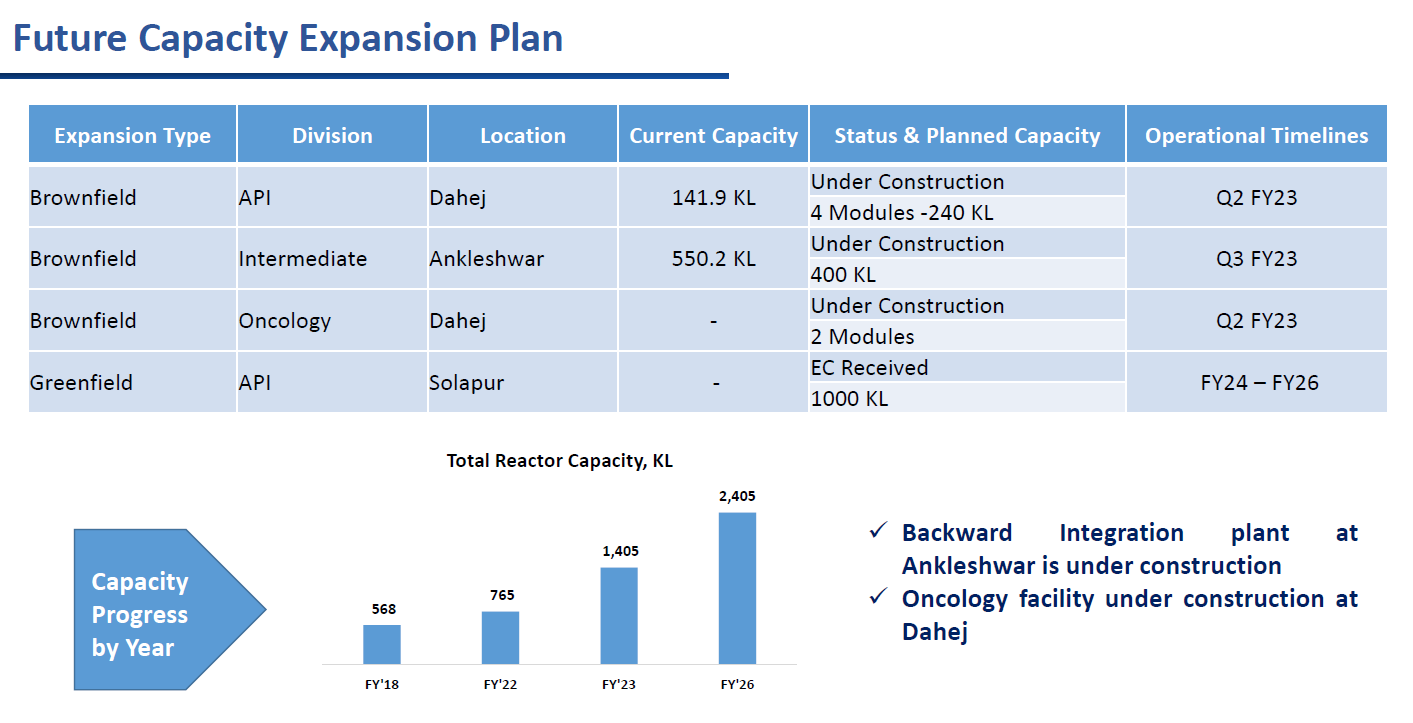

- Delay in capacity addition by one quarter

With:

EV/EBITDA < 10

PE < 15

ROICE of 37%

Cash on books ~514 cr

there is margin of safety in an otherwise expensive market.

D: Invested

9 Likes

All parameters look good but they seem to be struggling for growth for past 5-6 quarters. Probably why they are delaying capacity addition.

Also, the greenfield expansion plan seems to be of higher capacity than what was earlier projected.

3 Likes

Hello, I am a fellow investor/analyst and I have taken up a position in Glenmark Life Sciences Ltd over the last few weeks. Most of my following statements may be biased owing to the recency of my investment and hence may appear utopian. With the spirit of contributing to the community, here are some of my thoughts on the company’s Q1FY23, management commentary on concall this morning and the overall business in general:

-

OVERVIEW: The quarter seemed in-line with (my) expectations yet still slightly better than peers. Revenue declined, PAT increased, margins expanded, but overall performance looked flattish and lukewarm. The booking of PLI scheme benefit came as a welcome surprise, especially since it looks like a steady benefit every quarter until FY2025. Although supply chain issues appear to exist, but the management has so far ensured the company avoids any significant impact on the business, and appears confident for improving circumstances. Demand is expected to remain decent on aggregate across geographies with eyes on Europe to revive. Capex appears to be on track despite a slight delay.

-

REVENUE: Topline growth looked tepid and ex-COVID sales growth is not very high although it sounds comforting to announce it like that. But it helps to remember that the company is working in a competitive industry, during a sectoral slowdown, uncertain geopolitical situations and most importantly, almost at full capacity. The future topline growth will be a mix of Volume-Price but that might only begin to be visible from H2FY23. Although the management expects some revenue growth in Q2 but let’s be realistic. Now Volume contribution should come from Dahej with a capacity expansion of ~ 34% going online during Q2 and utilization going up by Q4FY23. Price contribution should come from ongoing initiatives in Complex APIs (Iron/Oncology), new Oncology block at Dahej coming online in Q2 and the expected comeback of CDMO business as customer’s inventory rationalization ends and 4 CDMO projects become active. (Why I assume CDMO inventory realization to end, is because it isn’t a huge segment yet anyway and it’s unlikely the customers would take so much time to take stock/budget for niche specialized products.)

-

PROFIT: Bottom-line looks increasingly more stable, satisfactory and promising. It is comforting that the margins seem to be getting better and the cash-flow history is evident in the nature of the business and the way the operations are structured. There appear to be no illusions for optics here.

-

MARGINS: It was a pleasant surprise when it came to the company conserving or rather improving the margins. First, the contribution to margin expansion by PLI seems to provide a good base support as it isn’t a one-off case. Second, as the pricing/input cost/energy issues subside and the company returns to normal scenario, the margins are expected to return with stability, or rather improve even further which would be a positive. Third, the Ankleshwar capacity of 400KL is expected to further contribute 80-100bps to margin expansion as it supports backward integration of important APIs. Fourth, overtime as the topline grows there may be some compounding effect on the margin contribution by the PLI benefits in particular, which may be a small change but worth noting.

-

CAPEX: There has been a disappointing delay in the BI capex at Ankleshwar now expected to become operational in Q3. Since the primary objective of that capex is stability of supply chain for KSMs, it shouldn’t affect the business much as we are building longer raw material inventories anyway. Now the brownfield expansion at Dahej (supporting 34% growth) is expected to be operational by September which is significant. In addition, the greenfield expansion work at Solapur is moving at a slow yet steady pace with the site receiving Environmental Clearance for 1000 KL. The management has also indicated an interest in increasing capex objective at Solapur from 800 KL to now 1000 KL as per the updated presentation. It is important to note that this expansion will be done in phases with partial capacities becoming operational every year until FY2026. It is comforting to know that the management is confident of demand and of catering to that demand, along with the visible growth runway for the next few years. Additionally, the oncology block at Dahej is also expected to be operational by September.

-

MANAGEMENT: The team led by MD & CEO Dr. Yasir Rawjee and new CFO Tushar Mistry seem able to manage this company. The CEO has displayed his grip on the unit economics of the business, a cautious approach to sustainable growth and a strong focus on relations with business partners. They are not forgoing their Chinese supplier impulsively due to long-standing relations while ensuring stability with alternate suppliers in India and doing some backward integration. On the customer-end they are not increasing inflationary prices for few customers that need support to maintain their market share in the front-end but at the same time improve their operational processes to protect margins. A caveat here could be that they are doing few of these things to in fact help their biggest customer, which is the promoter itself. Regardless, a management that actively protects the interests of all stakeholders in a balanced way is a management to bet on. Both CEO Rawjee and CFO Mistry come from leadership roles at other pharma majors, so they may be expected to lead well.

-

PROMOTER: There is a definite overhang of the pedigree of the company. The promoter group is their largest customer and that can be a concern of conflicting interests. A reassurance here is that the revenue contribution from the parent is rather a stable and regular business, and in fact has come down to 35% this quarter. Another concern is that the promoter might offload some stake to pare its own debt, which is a reasonable thing to do as well. A way to look at it is that they need to come down to 75% shareholding anyway in another two years as per SEBI norms. Also their lock opens on 6th August, 1 year after the IPO. Now if I can be a bit speculative and hypothetical here, then it makes no sense for the majority shareholder and promoter to sell in open market when there is low share volume in a business that’s doing well and when they came with IPO at 720. They won’t be able to offload much and yet reduce the value of their remaining stake as well. Their own debt is significant and they only sold a small % of GLS during IPO naturally to sell more later at a better price. It would make much more sense for them to do a bulk deal with institutions at a reasonable price that benefits everyone. Now this may be just dreamy wishful thinking on my part but that’s the way it makes the most sense.

-

RISKS: The FDA inspections are due at all three facilities and management expects them within a few months. Any negative remark/warning may be of significance to near-term growth. It is worth noting that the company has never received any regulatory remark or warning in it’s history so far but that doesn’t mean it will pass with flying colors every time. The most careful driver will also nick the car at some point. And hence that remains an important risk to factor in.

-

OUTLOOK: The business, as I see it, looks very solid given the demand situation, the sheer strength of the balance sheet and decent confidence of future growth being on track supported by capacity expansion with internal accruals. I won’t get into any DCF analysis here but it looks safe to say that the company should do well and is available at a discount to peers.

Disclosure/Disclaimer: I must reiterate that I have recently invested and hence biased. I welcome new perspectives so that I can educate myself further and reassess my expectations. Thank you!

16 Likes

I wonder if we have the CAPEX for each location expansion plan?

Also, what could be expected asset turnover ratio for each expansion.

2 Likes

Avg. asset turnover has been 3 so I think it will be similar for this.

1 Like

Thank you for the summary. Here are some additional points that I picked up from the call:

- Solvent prices have cooled in the past few months

- Prices of RM that are derived from lithium, iodine, sodium and phosphorus still at elevated levels

- Margin has bottomed out and can only improve from here. Oncology products to be margin accretive

- Participating in Januvia (sitagliptin) opportunity. Supplying to 2-3 customers. (Januvia global sales are $5 billion)

- Strategically increasing inventory of some key RM

- Cash on books - 478 cr

Key monitorable in the coming months, as rightly pointed out by @raghavbansal, is the possibility of a USFDA audit.

7 Likes

-

Capex for brownfield (240KL Dahej expansion, 400KL Ankleshwar BI and Dahej Oncology block) should be above 150 crores. They had projected 152 crores from IPO towards these plans, but since some of these were started before the IPO the actual capex may be slightly more. Although it should be noted that they have only used around 50% of these proceeds so far. Capex for greenfield at Solapur was projected to be 600-700 crores for 800KL but if they build 1000KL now then that should be around 750-900 crores.

-

Asset turnover ratio is currently 3 and they seem to be guiding to keep it at/above that in the future as well. However it would depend on: A. Capacity utilization of new facilities when they come online; B: The kind of business they run on these facilities. Absolute revenues and hence turnover ratio will be higher for CDMO > Complex APIs > Niche Generic APIs > Bulk Generic APIs. But since they do ATR of 3 with 90% business coming from non-complex generic APIs right now and they plan to move to more CDMO and Complex products that may increase. At the same time they said future growth will come from a mix of Volume-Price, so ATR of/above 3 should be expected to continue.

6 Likes

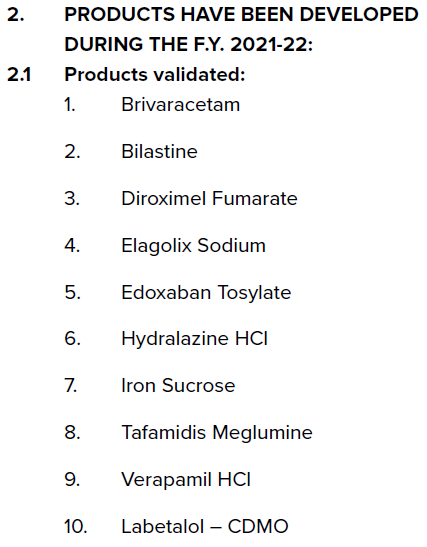

The first annual report of GLS is out this week and an interesting piece of information that was buried in the AR was the following list. It has the products that were developed & validated in the current fiscal. One can assume that these are ready to commercialize or already have been commercialized.

I’ve given their global sales and originator company name to give readers/investors a sense of the opportunity at hand.

| Sr.No. | Generic | Brand | Originator | Size ($mil) |

|---|---|---|---|---|

| 1 | Briviracetam | Briviact | UCB | $355.00 |

| 2 | Bilastine | - | FAES Farma | $290.00 |

| 3 | Elagolix Sodium | Orilissa | AbbVie | $39.00 |

| 4 | Edoxaban Tosylate | Savaysa | Daiichi Sankyo | $563.00 |

| 5 | Hydralazine HCL | Apresoline | Hikma | $51.00 |

| 6 | Iron Sucrose | Venofer | Vifor | $146.00 |

| 7 | Tafamidis Meglumine | Vyndamax | Pfizer | $561.00 |

| 8 | Verapamil HCL | - | $28.00 | |

| 9 | Labetalol - CDMO | - | Hikma | $6.00 |

| Total → | $2,039.00 |

13 Likes

The main reason behind the underperformance is i guess the fact that it’s sales are mostly focused to Glenmark Pharma if you look at the related party transactions which is a parent company.

7b66fd59-bf5c-40d6-b92a-a67024e71660 (1).pdf (792.3 KB)

2 Likes

Indeed. But that was very much known since the company began life as the in-house API manufacturing arm for Glenmark. However, the %age of sales to the parent has been consistently coming down over the past 4 quarters. It is the -ve perception of “related party transactions” that is resulting in the current mis-pricing of the stock.

D: Biased. Invested

2 Likes

One of the reason for not performing share wise is that promotor holds 82% and they have to compulsory bring down to 75 % and time line is nearby .they must offload 7 % in market or by placement

1 Like

Where do you see the timeline? Can you please post??

And personally speaking offloading 7% is not a big deal here… It’s a quality company with no limit to the potential.

Similar thing happened in Syngene and people sold it hearing some rumors of promoter going to sell, but nothing happened and it’s back to similar levels.

However i know regulatory requirements and so 75% has to be met in near future…but would be interesting to know the date i am supposing

It is valid argument but somehow other listed entity like Mazagon Dock is played well with higher stake of promotor holdings with above 80% and true that although it’s a PSU stock, undoubtedly doing good with a strong moat, business should have strong moat to perform well in consolidated market. And I believe, factors like pharma sector, geographic tensions, and most importantly thematic downtrend is the factor here rather an higher stake of promotor holding.

1 Like

PSU and other company have different criteria for bringing promotor holding to 75 %. So it’s not comparable. Details one can check in sebi s website or net. PSU have liberty and not compulsion in time limit for the same. So

I just said this could be one of the reason for share price not performing.

2 Likes

Personally, I feel the major reason for stock underperformance is lack of topline growth. Rest all parameters - margins, management credibility, industry segment etc are all good

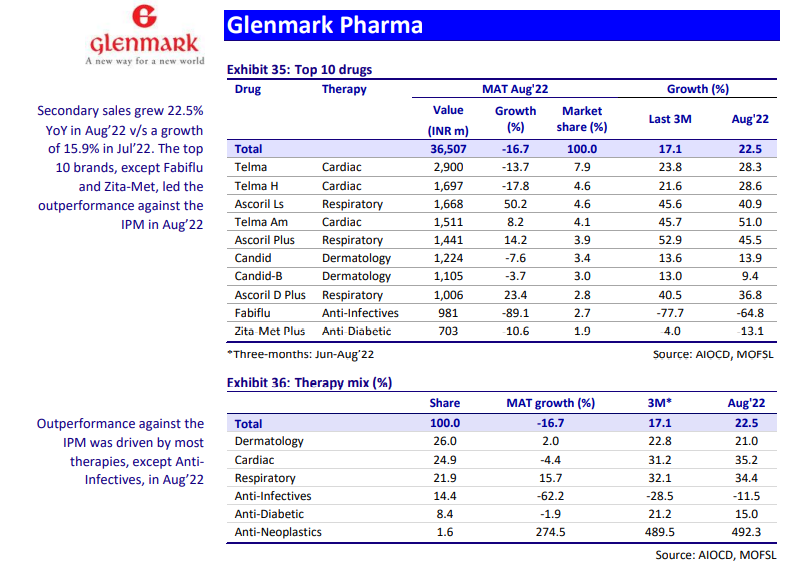

The domestic sales growth of the parent in the key therapy areas of cardio & diabetology has been quite good. This augurs well for GLS’ key products like telmisartan and one can expect growth to return.

D: Invested. Biased

3 Likes

Yes i totall agree. If top line does not increase no body will be interested.

Also too much dependency on parent Glenmark pharma

1 Like