Thanks for sharing the analysis on the gross margin and SG&A expenses, however your final summary seems to be quite misleading given it’s financial performance.

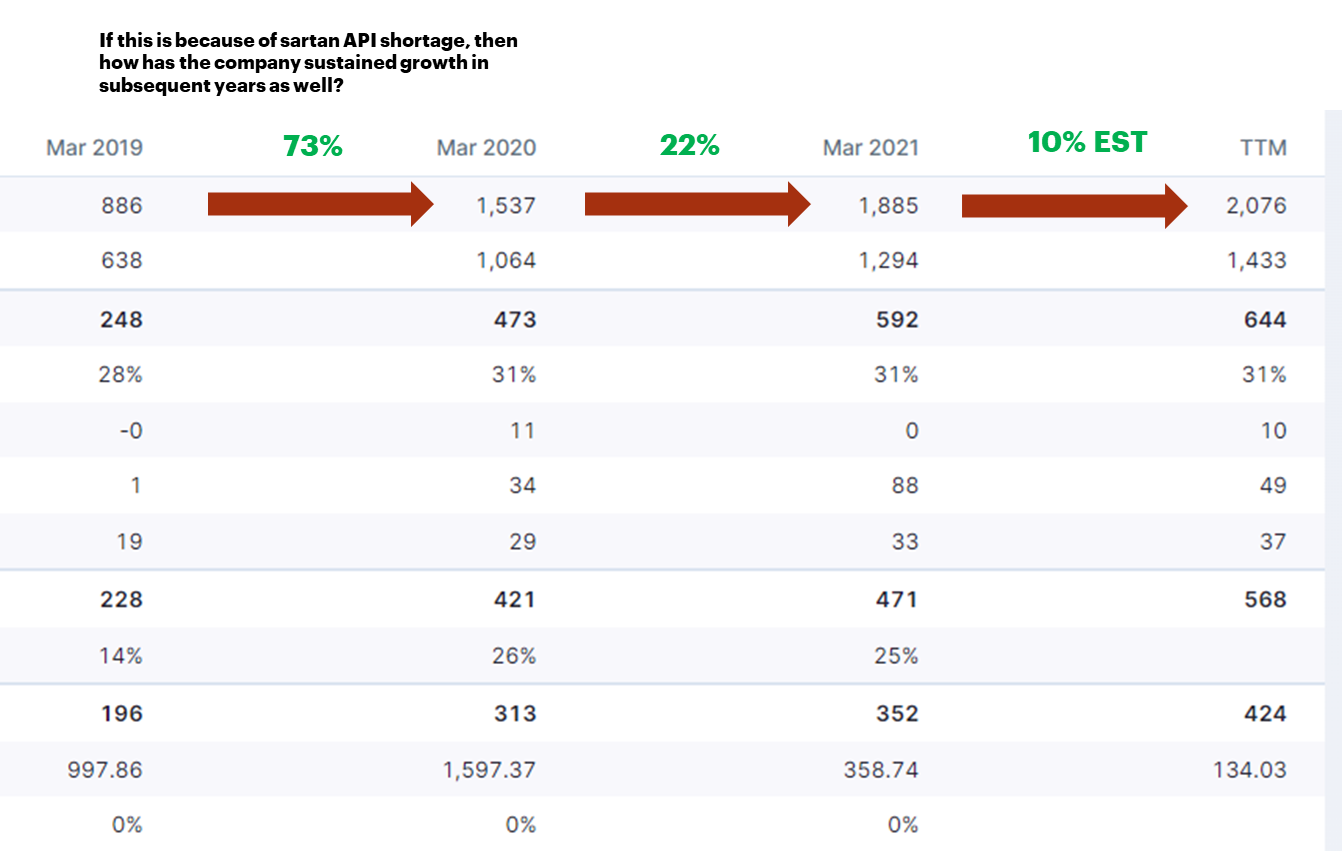

If you believe Glenmark benefitted a lot from the sartan API shortage in 2019-20 and actually does not operate with any competitive advantage in complexs/specialty APIs - why has it been able to continuously grow in the past 2 fiscals?

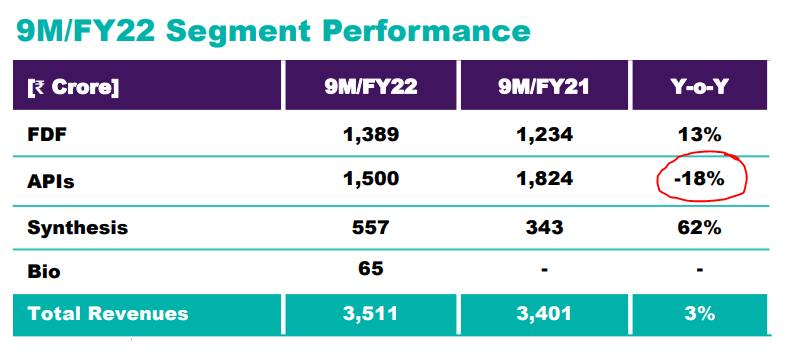

Companies like Laurus and Neuland have struggled to grow the API business in 2021-22 along with huge margin compression. Laurus’ API business has degrown 18%. A company like Alembic was the true beneficiary of Sartan drugs as you can see from their financial performance in the past few quarters.

Laurus Labs

Alembic

Glenmark management claims they operate in high value APIs, which range from $200 / kg to $800-900 / kg. Do you have any data to compare this with likes of other API manufacturers which would help us understand if these are commodity APIs or niche / specialty APIs?

Customer Concentration

I agree there is a parent concentration risk i.e. 35-40% revenue from the parent company, however It’s customers also include 16 of the 20 world’s largest generic pharma companies globally.

Regulatory Track Record

In the last 6 years, it has not received a single warning letter or import alert. Since 2015, GLS facilities have been subject to 38 inspections and audits by regulators including the USFDA, PMDA, COFEPRIS, Health Canada, MFDS (Korea), EDQM, other European regulatory agencies and CDSCO conducted on a periodic basis. GLS has not received any warning letters or import alerts from such regulatory authorities. GLS facilities have also been subject to 432 inspections and audits by our customers during this period

CDMO Business

Very sweet business, very high margin business, much healthier than generic business margins, business growing very rapidly - crossed 200 cr business in FY20 and FY21 business went down to 150 cr as 1 molecule got affected due to Covid, but expect it to comeback as Covid fades away.

Based on the company’s recent performance and track record, I don’t see why this is an average or bad business. If the company can maintain the revenue growth and EBITDA margins at 28% in Q4 as well, there is something special about the company where most other API makers have struggled on revenue growth (no new customer orders due to high inventory) along with 5-8% margin compression

Disc: Invested