40% of revenue from parent Glenmark Pharma

1 Like

Glenmark Life sciences–Q2FY22–Earning call Highlights --12th Nov21

( Disc : Dont have any position , just tracking it , some points i may have missed as Transcripts have not been released yet ) :

– 7 molecules in the pipeline & in the Dahej expansion we have an oncology Plant which will start functioning in Mar22. We have 3 cancer products ( part of above 7 molecules ) up for validation in that plant from Apr-June22.

–Parents contribution to the topline --40% & for 6 months its 41%.

–Contribution of Covid --Low single digit in the Qtr & 1st Qtr was 12%

–Any US FDA inspection in Ankleshware --last inspection happened in July2019, Dahej --nov2018 & this month we complete 3 yrs in Dahej. We could expect an inspection in the next few months.

– Steady state Margin guidance --given depth & less commoditized portfolio we can expect 30/31% despite head-winds

– Sourcing from RM from China --40% we take & our dependence is well below 10% , its just that we have steady-relation with chinese supplier.

–Gross margin improvement is a result of Product mix , we have input cost pressures ( largly solvents) , this Qtr we had a lot more on CDMO side and lot less on Covid ( favipiravir) so margins are better last Qtr. Had we not had the challenges in the input & energy cost it would be better.

–CDMO uptick sustainable , Gross of 50/52% & EBITDA will be 30/35% sustainable

–Qtr 2 for entire API pack is weak --why we had a good performance in API —its due to nature of portfolio ,stayed away from commoditized portfolio so have done better. We had cost improvement projects in last few months. Headwinds in input cost is relatively smaller % of overall product cost --result is lesser commoditized molecule --so its a combination which has resulted in growth & Margin --QnQ growth is 7%. If we take away Favipravir contribution our growth is 15%

–Capital Allocation --Capex next few yrs will be 360/370 Crs , this yr we will spend 150Cr, next Yr sholapur greenfield site --210/250 Cr–most is capacity expansion , increasing R&D capabilities with new chemisteries in flow chemistry etc.

–Latam & Japan has had significant growth with new business addition --new projects to existing cust. & new customers.

–Business drivers —CDMO driver is a big one , new launches ,new geos .

–CDMO --we have 3 commercial projects which are going well , we have a 4th which can come online in Q4/Q1FY23

A Cust. wanting to launch in 52 mkts & their challenge is due to covid doc/ patient interaction , germany has covid & US also is showing signs of increase in Covid, so this will pick up but due to Covid the pace will be slow.

–we have derisked china suppliers over the past 2/3 yrs by establishing sourcing from other sources i.e India / Europe & dependence on China there is less than 10%.

–Sholapur as a site --advantages --We have a small facility in Sholapur & we had to do rapid execution ,there is a MIDC in sholapur & infra is on par with other places , we had couple of facilities in the neighbourhood so we found it advantages within 15/18 months we will have a good running facility in Sholapur. & Its cheap compared to other industrial areas

–Interim dividend --25/30% for the yr , we are generating close to 450/500 Cr cash flow pre-capex & once we account for Capex we have good profits and good cash flow so we will aspire to keep this dividend %

–Orderbook & Pipeline for H2 in CDMO—Momentum will continue for the next 2 Qtrs , there are 3 commercial opport. driving it , & 4th one may come in Q4 as that cust. has applied in many mkts.

–Why Glenmark Pharma contribution to growth is that high at 40% , was expecting this contribution to go lower ? --Favipiravir --was a high base & if we adjust for that we had a growth of 13/15% in the Qtr.

–Glenmark Pharma contribution historically has been 30/35% and this will continue as we have quite a few APIs with Glenmark Pharma.

–Capacity Utilization --90% , its even higher than 90%

–new capacity in the near term ( Q4) & Q1 will add 240Kls of capacity ( By June22) & it will give us a runway of for the next 1/1.5yrs. so we are managing through product mix to push high margin products.We are running full and it wont impact our growth

– FY23 Capacity utilization --CDMO & Generic APIs growing with CDMO pace is higher. Both our FDA approved sites --Dahej & Ankleshwar we have expansion ability eg. of 20 Acres of land in Ankleshwar , if need be we will grow there and it will require a minor approval.

–Every yr we have 3/4 Molecules for launch , we have 2 very big molecules coming up in Q3&Q4 and its regular & big launches with multiple customers

—Will backward integration change in Ankleshwar the RM landscape for us --it wont completely normalise but our plan is to protect top 20 Molecules which will drive our growth & Business 80% for the next 2/3 yrs & to look at back-ward integration where-ever possible , we started with that work & right now we have 3 molecules ready to get into the plant.

– This backward integration will help our margin profile and supply reliability.

–Some clients have agreed for Price rise & we have convinced them but for most cust. we have been able to get cost improved process & that has helped us in helping some customers.

9 Likes

Good insights shared by the CEO

5 Likes

H1 FY22 EPS is around 20. Extrapolated to annual FY22 EPS of 40. At CMP, the PE is 15.

For a company with very good financial metrics (net profit margins at 20%), valuations look quite less. Is there any issue that we retail investors are not aware of?

In Q2FY22 concall, the last question by an individual investor was why the valuations are low for the company, considering the high ROCE and margins, and if this could be due to some corporate governance concern among investor community. The answer was they have an independent board and follow the best corporate governance practices. Also MD & CEO Dr Yasir Rawjee joked that It is a good time to buy then.

A few reasons I can think of is Glen pharma still holds around 82% of the stake and they could dilute it further to reduce their debt, 35-40% revenue dependence on parent (this could be seen as a positive as well in the sense that 35% revenue is guaranteed) maybe the market is waiting to see how this dependence plays out. Also as their parent is already engaged in formulation their CDMO business might not scale as expected due to lack of trust from CDMO customers.

Disc:- Tracking position

2 Likes

Agreed. It would be good if they bring an outsider as chairman to GLS. (Similar to how Solara brought in Aditya Puri).

Biocon’s subsidiary Syngene does well in CDMO biz even though promoter is a pharma company. So if there are no clashing product lines (and non compete agreements signed), CDMO should do well. Glenmark Pharma has no major history of such issues I guess and are quite professional.

1 Like

One reason on why this is trading discount compared to other API companies is their parent size. Parent company is at 15000 Cr market cap and GLS is at 7500 Cr.

If someone expects GLS trading cheap and it should rerate similiar to peers, then obviously it will reach somewhere near to market cap of parent and it will push the price of parent, so some may have taken position in parent instead of GLS and also some may think parent is worth 15000 and so a subsidiary can be worth so much only

Disc: Tracking, Not Invested

2 Likes

Any idea where we can find their historical data before it got listed?

Ebidta margins have always been in similar range of 28-30% or was there a shortage of api they supply because of which margins are so high?

Not including Cdmo as it is still at 10% only.

You can check Draft Red Herring Prospectus

Any views on Q3 results? The margin pressure is understandable but topline growth is quite muted

1 Like

I genuinely feel the growth in API space is slowing down. Coupled with RM increase companies like GLS might feel the heat for few more quarters until the Gas and RM prices soften more. I think it might be range bound for 2-3 more quarters before some kind of upmove. Disc: Invested in GLS

Yes, there is some slowdown in growth in general. Perhaps we can wait for results from Divis Labs tomorrow. But GLS seems to be quite well managed. (Especially considering what happened with Solara yesterday)

GLS share price is bordering 500 - valuation of around 6000 crores and FY22 PE of 14 or so. With the planned capex, EPS will increase slowly but steadily. Just want to check if 400-500 will give sufficient comfort to enter keeping long term in mind? The company’s prospects look good but I just don’t understand why the two Glenmark companies (Pharma & Life Sciences) are trading at lower valuations. Is there something (negative) about the management that’s not known well in public OR any of the past actions of Glenmark Pharma management that doesn’t give confidence to institutional investors?

Appreciate any kind of inputs on this.

Try to answer the below questions

- What is the niche API that they produce which will give them steady revenue

- Dependence on parent (I understand they sell more than 50% to their parent), this is a huge risk in itself

- Do they produce commodity kind of APIs ? (Like Ibuprofen )

- CDMO /CMS - These two words are seldom used now a days by all the companies , in investor pitches . This is very very hard to understand. When ones thesis fails it fails very badly (example is Solara , where industry was thinking it has dependency of 30% on Solara but it turns out to be they have many other products which are very low in demand )

- Try to scan through all the research reports / RHP etc… , export data (little hard but not impossible if you can search around ) for the niche molecules that they are in , if is niche then you have pricing power , if it is commodity kind of molecule then either one has to be lowest producer and at the same time there should be enough demand for the same.

IMHO , CDMO / CMS - though they are separate listed entity but I guess they still have strong relations so the question one should ask is , why would an innovator trust Glenmark on a discovery opportunity ?

2 Likes

My previous post was after checking all those points, hence felt the prospects look good but not reflecting in valuations. They are not into commodity APIs and hence charge premium pricing to their customers. Their website has details of all their products. Even their latest quarterly results showed yoy growth although a bit muted and were to able to maintain a good profit margin inspite of raw material price pressure. This is not the case with many other companies, as you know.

The contribution from parent company is 40% and not 50. I guess it’s up to individuals on how they view it. Even HDFC group companies get and give businesses to each other. In the Q3 con-call, the MD has mentioned that contribution from the parent is a steady business, so why worry about it. He also mentioned that their contribution as a percentage will come down in a few years especially when their CDMO business takes off. Their new greenfield capex is primarily for CDMO opportunities. This is to be watched - on how they would grow their CDMO part.

Most of the peers (except for the likes of Divis) have shown issues either in topline and / or bottom line but Q3 for GLS was relatively stable. They will also be completing some capex for backward integration this year which would help in sustaining margins. So, on a relative scale, the prospects look good. We need to watch their execution of course but looking at past few years track record, they have been growing quite well.

8 Likes

Hi,

My understanding is they are into non-commoditized APIs primarily focussing on regulated markets- which require stringent quality checks for impurities as mentioned by CEO, which is very difficult for any manufacturer.

As far as Parent contribution is concerned, CEO said in a call that that is a very good business, and IMO too I feel that is kind of sure business for GLS which will gradually be reduced.

During the question regarding new drugs for new covid variant, CEO mentioned that for one drug there were already 6 manufacturers who had approvals and one among them was backward integrated. So even though they had the process and product ready they refrained from getting into race. That shows that their focus is more towards sustained margins. And which reflects in latest quarter results. We can see that margin has been cannibalized at many API companies.

During last quarter, they have primarily changed their expansion schedule. And it seems market did not like it. They have fast tracked backward integration project so that they can have stability in supply of raw materials, and which will enhance the margin but not increase topline much. And they have kind of delayed greenfield expansion which suggests to me kind of reduced demand environment. And that seems to me the biggest worry.

IMO margin will not be much problem for GLS, but growth in topline is something which will not be as guided earlier by management(which was in the range of 16% - maybe in a first concall). Growth in topline needs to be monitored closely in next 4 quarters. Even their onco and complex molecules will take few quarters to get reflected in topline. CDMO growth will be there but on a small base. And the 4th CDMO project which was supposed to be started in Q4 after 2 postponement, has been delayed again by almost 3 quarters. Apart from that inspections of USFDA is already due and can be expected any time, the uncertainty of the same will be there and may linger over stock price.

All in all I think, good company, good R&D capability, good set of diverse products, good sustainable margins, wide set of geographies, good set of new product launches planned, large penetration in regulated markets, good set of approvals in hand, good track of regulatory compliance, focus more on sustainability in operations through backward integration, reduction of outside dependence, attractive valuations, But slower topline growth trajectory for maybe next 2-3 quarters.

Disc : Invested, haven’t taken full position, waiting for next 2-3 quarters

7 Likes

There is a thin line between commodity API vs specialty API company , if we fail to spot that we will end up with companies like IOLCP , Solara etc…

To me only DIVIS is the one which stands out, they have niche molecules + scale. Niche molecule(s) + Backward Integration (they maintained their gross margins by investing in the KSM ) + Large Opportunity size

@harsh.beria93 if you are tracking this company please share your thoughts.

Edit :

This Pharma play is something like Digital (every IT company says their digital revenues are growing ) , everything is painted with CDMO

4 Likes

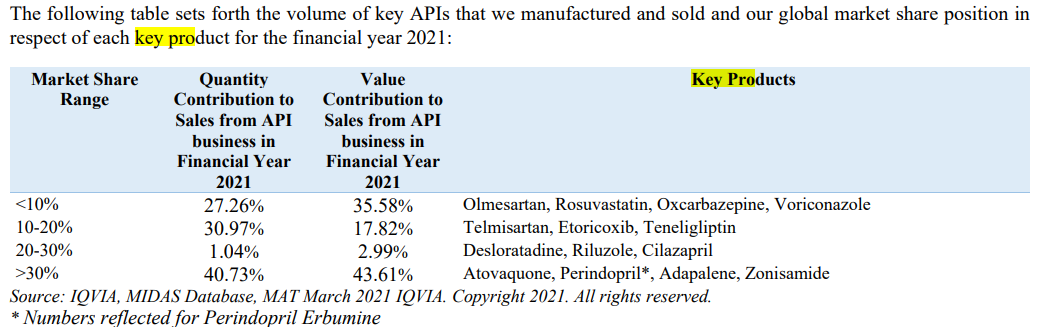

Everywhere I read about GLS, I see the word ‘non-commoditized’ for APIs mentioned. As per the DRHP below are the key products. I am trying to understand how can we come to the conclusion that these are really niche products or not. If somebody could guide here that would be great.

Disc: Tracking position.

1 Like

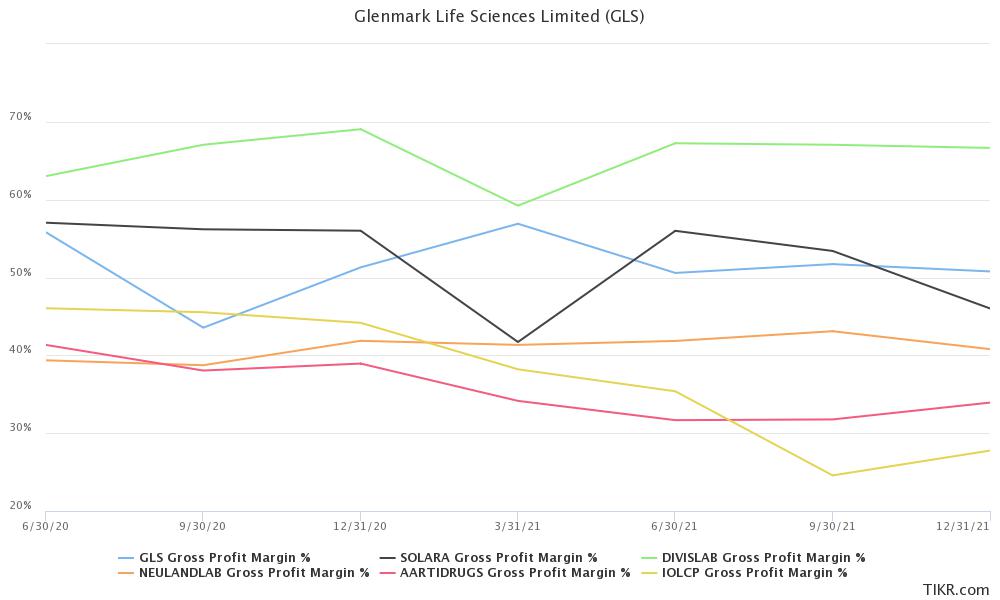

For an outsider like me its hard to differentiate b/w commodity and specialty API. However, I can track gross margins which should reflect the amount of value addition which goes into products. Its very clear that Divis has highest gross margins among API companies (60%+). Solara and Glenmark have similar gross margin range varying b/w 50-60% and others (Neuland, Aarti Drugs, IOL) operate at lower gross margin (<45%). In terms of gross margin, I will slot companies as (based on tikr and screener data):

Divis > (Solara ~ Glenmark) > Neuland > (IOL ~ Aarti)

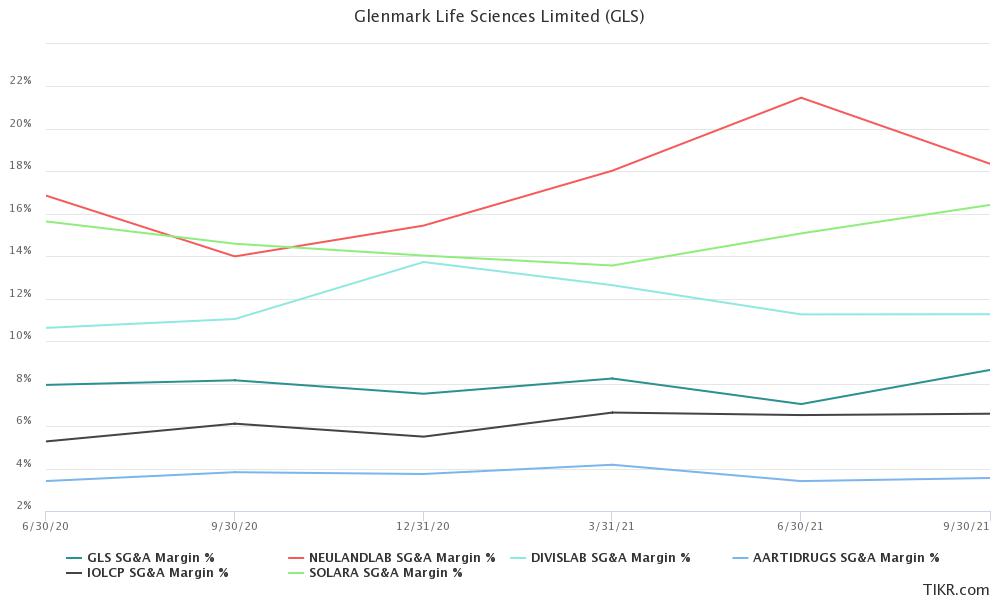

I think Glenmark Life’s operating margins are higher due to their lower SG&A costs, a big reason for this is they have only 1 major customer (Glenmark Pharma) that would not require much SG&A spends.

SG&A costs are also lower for bulk commodity API companies (see Aarti and IOL) as that would not require large marketing teams as most business will be based on spot contracts. That’s generally the case for bulk commodities. Even on employee front, Glenmark’s cost is quite low (7% of sales vs 12-14% for Solara and Divis). This is closer to that of bulk API players like IOL or Aarti Drugs (3-5% of sales).

In summary, Glenmark Life seems to have higher gross margins than commodity APIs and employee and SG&A spends in-line (or slightly higher) than commodity APIs. That’s why they have 30% kind of operating margins.

Additionally, Glenmark Life benefitted from sartan API shortage in 2019-2020 which made numbers looks even better. Apart from that, every company talks about complex APIs (oncology, peptides, etc.). This is like generic formulation companies talking about complex formulations, makes for good narratives (not good business).

Disclosure: Not invested

11 Likes

One of the easiest and generic way is to look for OPM. You can use this for any business. It is not deep dive but historical look. GLS.has. 31. Divis.40+, Solara less than 25.

When you see fluctuation in their OPM, it shows their pricing power. So OPMs are helpful for historical purpose. If a company is getting into high value products with higher margins, then historical OPMs will not make much sense.

Cheers

1 Like