In Concall GLS Management stated that they are confident that matter will be resolved shortly and in next 2 months of this quater they will makeup the production loss. Indirectly they are trying to say that by this month end matter will be resolved.

1 Like

I believe any closure notice revocation can happen after min. 25-30 days. It might take more time than that. Ankleshwar, Being a majority production site , production loss would be substantial. If not more they will lose atleast 25-30% reduction in production in this quarter.

More serious issue in my opinion, is the reason of closure. It seems company mistakenly or intentionally let out effluent in storm water drainage, which showed in the COD parameter. Being not so serious about local authority compliances when your foreign inspection like FDA are overdue is matter of concern. And one very big risk to look out for.

Evaluating to sell/reduce allocation here.

Thanks,

4 Likes

Is this speculation from your side, or you have factual information ?

No speculation. Just listened concall. First question was regarding closure. Yasir Sir answered that GPCB official collected sample outside premises of company from storm water drainage… During rains and so on… pls listen to concall.

Now logical reasoning says that rain water does not have high COD. And GPCB officials are very particular and has strong case while issuing closure notice. So if COD is higher then effluent or batch liquid (Which both would have high COD) must be mixed with rain water. Mistakenly or intentionally are not of question. This should not have happened.

Pls note : I own and manage Dyes mfg unit and regularly deal with GPCB officials since last many years.

7 Likes

Understood.

But Dr. Yasir also mentioned (in fact he sounded very confident) that they will resolve in less than 2 weeks…is that also difficult to achieve?

1 Like

More than a week has already passed. Although GLS management is very conservative, we should never put our assumptions/thesis entirely on management comments.

Disc - Invested from lower levels.

3 Likes

The GLS plant in Ankleshwar is in industrial Area its not in civil or population Area, and surrounded by other industries and empty land marked for other industries. My understanding is that Nirma or Earlier Glenmark Pharma has substantial hold/ link in Gujarat Govt or Politics which can easily influence GSPC officials not to pursue plant closure vigorously but to take care of corrective steps. GLS management has also taken proactive steps for future. So matter can be treated as deemed resolved. Which may be formally announced after 20/30 days. Otherwise when Dr Rawjee stated that Ankleshwar Plant gives 65 percent share in production the stock might had till now reached 500 but it jump upward after concall. So Donot bother about this issue its already discounted. And its also a good learning lesson for management in future as this issue has put their reputation at stake,

3 Likes

Closure means instruction by GPCB to electricity supplying authority of the area - where subject’s power connection is disconnected. They cut the power so all industrial activity of the unit comes to a halt.

I would not consider this matter as deemed resolved until company gets revocation letter.

The problem with Dr Rawjee is he is not fully transparent in his communication to shareholders. Especially if you have read each of his concall and compared the result and his guidance. Since listing. I can site instance where he CHOSE not to let us know bad news upfront. I doubt he has acted differently this time. PPl rarely change.

I don’t understand how and what market discounts.

My view is personal and I might be wrong in my thinking.

1 Like

I doubt that GPCB instruct Electricity Board to cut supply as both boards are independent and without having any power over each other. Industry also have Generators backup. GPCB instruct to Company for action.

I found Dr Rawjee , the best and Honest CEO not among the industry but also among the listed companies. Remains very conservative. Although some times he also proved some wrong in growth guidance which he gives in volume terms which we anticipate in Revenue terms.

1 Like

I understand that they could not meet their FY24 guidance and there was no clear explanation. All was lost in the discussion of ownership change and red sea shipping crisis. However, what other instances you are talking about where he did not let the investor community know about bad news upfront? Could you share examples?

2 Likes

If the closure is extended for few months then i would see it as an opportunity and i will add some more Qty at lower price.

If this extends for months then they will implement strict measures to avoid any reoccurrence at all locations

1 Like

Similar notice has been issued by GPCB to SGRL last week, it would be good to see how its resolved by SRGL as well.

Meanwhile the stock is up by 5% today ![]()

All GLS plants have regulated by USFDA, PMDA, COFEPRIS, Health Canada, MFDS (Korea), EDQM, other European regulatory agencies for various inspections and audits periodically and it doesn’t have any warning letters or import alerts from such regulatory authorities.

The closure notice by GPCB at Ankleshwar plant temporary affects the production, but it is negligible and will not make substantial impact beyond this quarter. If someone is invested with a short term horizon then that’s the different story. Nothing to bother for long term investors.

Regarding Dr Yasin Rawjee, company has a strong proven track record of strong EBITDA margins at 30% which reflects management capacity and quality. There is nothing wrong is being conservative while giving growth guidance because business scenario change with time or in given situation. i.e external factor can affect the demand just like red sea shipping crisis

Disc - invested

5 Likes

Pls try to find out about their initial expectation of start date of CDMO 4th project. Beginning from their first con call after listing. Try to find out how many times they have revised it. And still revising it. I would not call those guidance s conservative at all.

Try to find out about their capex timeline from each investor presentation and how frequently they changed it.

I shared earlier about few issues. You can check.

https://x.com/pankit66617087/status/1598977720377315332?s=46&t=rn4as_0nOnUYTgzw18ubZQ

3 Likes

Glenmark Life Sciences Q1 FY25 Analysis: Key takeaways!!

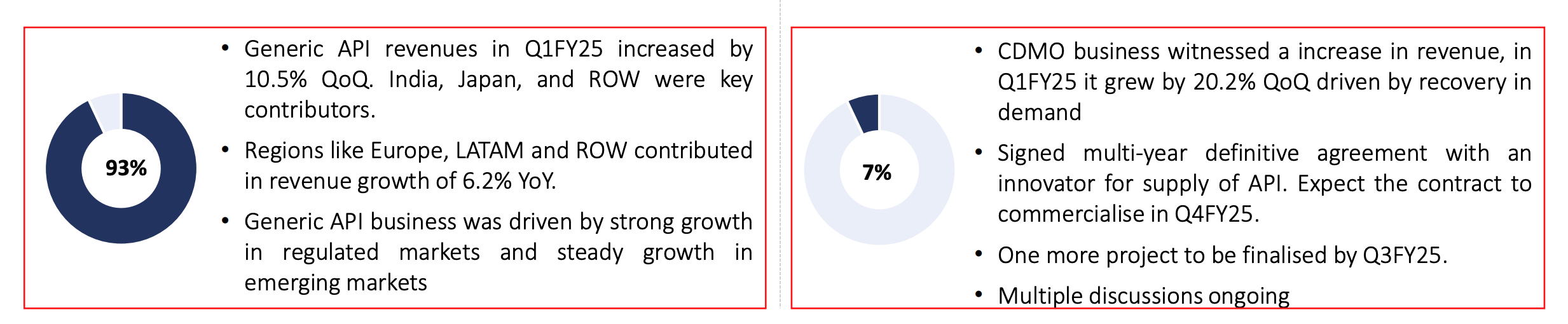

Glenmark Life Sciences has shown signs of recovery in Q1 FY25 with 9.7% quarter-on-quarter growth in revenue, reaching INR 588 crores. The company witnessed broad-based growth across geographies, with the Generic API business clocking a revenue of INR 535 crores, up 10.5% QoQ and 6.2% YoY. The CDMO segment also showed promising growth, with revenues increasing by 20.2% QoQ to INR 43 crores.

Strategic Initiatives:

- Expansion plans: GLS is focusing on capacity expansion with additional capacities at Ankleshwar and a new pharma capacity at Dahej becoming operational in Q2 FY25.

- CDMO growth: The company is actively pursuing growth in its CDMO business, with two new projects expected to start commercial supplies by Q3/Q4 FY25.

- R&D investment: GLS is planning to build its own R&D center to facilitate new technology platforms and portfolio expansion.

Trends and Themes:

- Recovery in demand across geographies

- Focus on chronic therapies (67% of revenue in Q1 FY25)

- Increasing interest from specialty pharma companies in the CDMO segment

Industry Tailwinds:

- Improving global economic outlook

- Rebound in pharmaceutical demand

- Growing interest from innovative pharma companies due to the CHIPS and Science Act

Industry Headwinds:

- Geopolitical tensions affecting supply chains

- Challenges in Europe’s demand outlook

- Raw material price volatility, especially in solvents

Analyst Concerns and Management Response:

-

Concern: Gross margin decline

Response: Management attributed this to discontinuation of PLI benefits and unfavorable product mix, expecting margins to stabilize or improve from current levels. -

Concern: Dependence on Glenmark Pharma

Response: Management emphasized that the relationship remains strong, with GLS supplying 90%+ of Glenmark Pharma’s API needs. They also noted that other business segments are growing faster, naturally reducing dependence. -

Concern: Environmental compliance issue at Ankleshwar plant

Response: Management expressed confidence in resolving the issue quickly and catching up on any production loss within the quarter.

Competitive Landscape:

GLS appears to be well-positioned in the API market with its diverse product portfolio and growing CDMO business. The company’s focus on expansion and new technology platforms suggests efforts to strengthen its competitive position.

Guidance and Outlook:

Specific numerical guidance wasn’t provided, but the management expressed confidence in continuing growth momentum in coming quarters with stable margins. They expect the CDMO business to reach INR 500-600 crores in the next 4 years.

Capital Allocation Strategy:

GLS plans to invest INR 300-340 crores in capex for FY25, with an additional INR 350-400 crores for the Solapur facility over the next two years. The company intends to fund these investments through internal accruals, maintaining a debt-free status.

Opportunities & Risks:

Opportunities:

- Growing CDMO business

- Expansion into new technology platforms

- Increasing demand from specialty pharma companies

Risks:

- Regulatory compliance issues (e.g., recent environmental notice)

- Raw material price volatility

- Geopolitical tensions affecting supply chains

Regulatory Environment:

The company faces stringent regulatory requirements, as evidenced by the recent environmental compliance issue. However, management appears committed to addressing these challenges promptly.

Customer Sentiment:

Customer sentiment seems positive, with growing demand across geographies and increased interest in the CDMO segment from specialty pharma companies.

Top 3 Takeaways:

- GLS shows signs of recovery with 9.7% QoQ growth, driven by broad-based growth across geographies and segments.

- The company is actively expanding capacity and investing in new technology platforms to drive future growth.

- While facing some near-term challenges (gross margin pressure, environmental compliance), management appears confident in resolving issues and maintaining growth momentum.

6 Likes

GLS was a Glenmark Pharma Subsidiary at the time of Its IPO in Aug 2021 ( Pharma & API Stocks boom period). Its IPO price was 720 and listed around 750. Its PE at the time of listing was around 24. Soon the stock start falling and after Russia Ukraine war in Jan 2022 the stock tanks to 400 (370 to 440) levels for more than one year from Feb 2022 to April 2023. Its PE at that time was 11-12 only. The API Stocks boom got busted in Jan 2022 and other API companies like Laurus and Divis showed compression in their revenue and very high compression in OPM and hence profitability. Thus their High PE also got elevated.

The average PE of API companies was above 40 in (2022-24) but GLS PE remained at 11-12 and than to 15 only. Unlike other API companies like Divis/Laurus GLS does not show degrowth and very less compression in OPM thus it profitability increased every year, but Market did not give high PE like other API companies.

Now after stake sale of Glenmark Pharma to Nirma the Price action is taking place. Although in next 1 year not much growth is expected but now share price is touching new high. Now its PE is around 28 which used to be 11/12 than 15/16 than 20 only.

What could be the reason

(1) Does Market thought that its a long story and its profitability over years gives it expected reliable longevity so its permanent PE rerating?

(2) After GPL stake sale now more institutions have entered and liquidity increased so price action is happening?

(3) Market is thinking that Pharma has not runup so Pharma Stocks are undervalued as compared to Market?

(4) Result of Promoter Change?

(5) Is PE rerating is temporary or now Permanent?

2 Likes

This is what i think

1 - GLS has always been a kind of under the radar stock since its listing and not the fancy ones we have in market so some of the underperformance was related to that. You rightly pointed out the PE range. Apart from that even the Price/sales ratio came close to 1 or below one during that time. You can imagine the perception market had that time ![]() Throughout this period they were able to manage their margins even though their earnings were volatile like their peers.

Throughout this period they were able to manage their margins even though their earnings were volatile like their peers.

2 - Not sure if the liquidity actually increased substantially. Other than the 8% GPL had after Nirma take over, there is no additional liquidity.

3 - All pharma stocks have done well since last 2 months. I think GLS just joined the party. Results are yet to validate the surge in price but we never know how market treats a company

4 - Promotor change will definitely have impact on GLS. They have mentioned this many times in concalls that Nirma is more aggressive for growth. In fact they are trying to complete Solapur much earlier than planned, establishing own R&D center and investing more in technologies now. Also GPL being a large generic player itself had lot of Conflict of interest for GLS’s CDMO opportunity.

5 Likes

Revocation letter issued by GPCB for GLS Ankleshwar facility.

Glenmark Life Sciences Limited.cdr (bseindia.com)

GPCB has imposed an interim Environmental Damage Compensation of Rs. 15,00,000 which was paid by the company.

1 Like

I feel this is the quality company with low valuations.

GLS is at very nascent stage in CDMO, this could be a big vertical down the line with good margins.

It can be consistent compounder over a long run.

Still there are some chances for PE expansion

4 Likes

Yes. GLS may be re-rated now after the management change.

The simple thing was that with GP promoters, GLS was mainly a CMO and now it’s trying to become CDMO. But it has a very ‘LONG LONG’ way to go. Check below the CMO & CDMO percentages of sales.

This is taken from the Aug 24 Investor Presentation.

Currently not invested.

dr.vikas

3 Likes