Agree with you, CMO will also grow along with CDMO so % of CDMO revenue in over all revenue would be not much, but growth rate in CDMO would be high by FY25 end as they are commercializing few more projects.

2 Likes

The most important part of the Q1 FY25 concall probably (besides calming the nerves on the GPCB notice) is this - Management says the new ownership is much more growth oriented and gives full freedom to make decisions, unlike before where the thinking was limited to what GPL wants out of GLS.

9 Likes

Good Efforts, But I think Pharma Theme is also Cyclical, DCF may remain a paper exercise only as almost with same revenue and same capex plan and same growth prospects it was available at 370 to 400 just 16 months ago, now promoter change, US Biosecure Act, Pharma Safety against other less growth sectors of economy, just 25 percent free flot availability as Nirma Type promoter will not loose even one share from his 75% stake are charging the sentiments and like it was available at 70% discount to its DCF value 16 months back it may now remain at 70% premium to its DCF value for some time.

4 Likes

For this FY only we can expect 208KL + 18 KL pharma capacity additions in Q2, we can expect some improvement in numbers of Q3 & Q4.

Real uptick start in FY27 as capacities mentioned as FY26 will be available 100% in FY27 and 2nd phase of Solapur will continue the growth movement.

Overall i think only some room left for re rating, if margins are back to 30% levels then valuations might move or else only uptick in the EPS will lead the growth.

3 Likes

If it start showing results than which is expected in H2 2025 to 2028 it will be rerated at some discount to Divis, it mean it can be further rerated further 70%, I think the present rerating will streach more as funds were not it’s shareholders earlier and supply is limited so they have to grab shares from retailers at some premium. As now market has started believing that from present Marketcap of 13000 it will be near 30,000 in next 3-4 years

2 Likes

hi

can you please share excel sheet here

thanks

1 Like

Sure

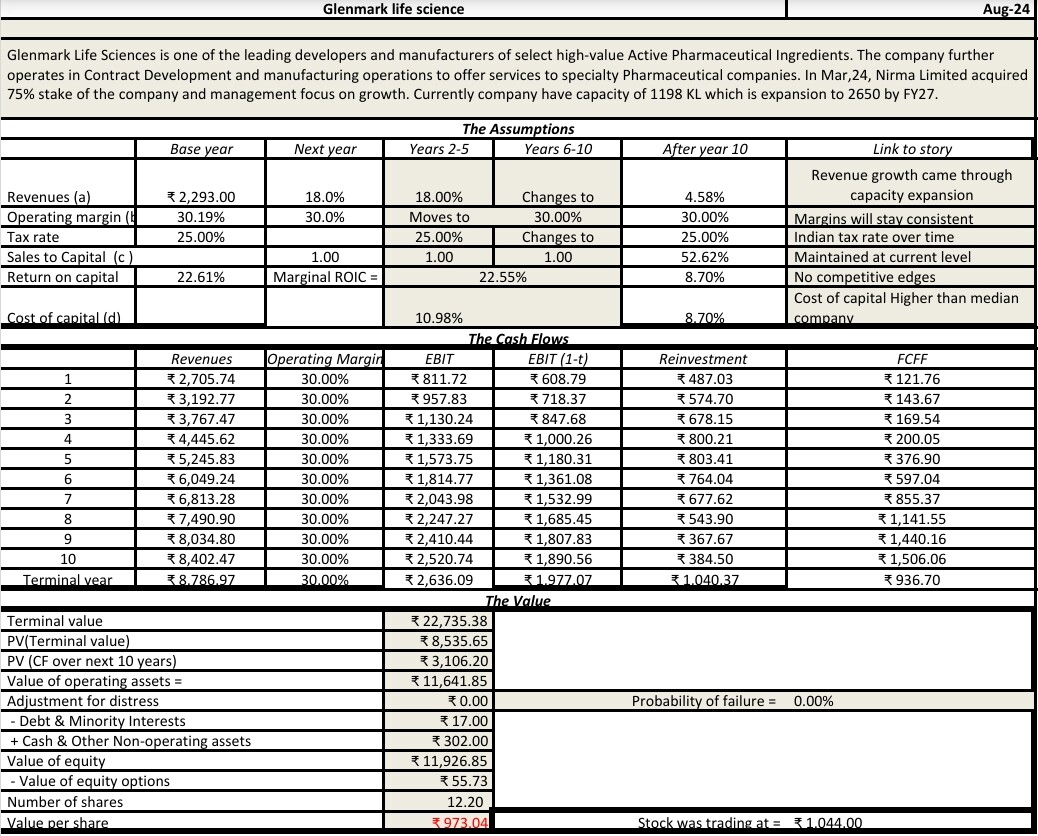

Glenmark life sciences.xlsx (244.7 KB)

2 Likes

Glenmark Life Sciences -

Q1 FY 25 results and concall highlights -

Revenues - 588 vs 578 cr, up 2 pc

Gross margins @ 51 vs 57 pc

EBITDA - 165 vs 195 cr, down 15 pc ( margins @ 28 vs 33 pc )

PAT - 111 vs 135 cr, down 18 pc

Cash on books @ 426 cr

Breakdown of revenues ( by customers ) -

Non GPL business - 392 cr ( 67 pc of sales )

GPL business - 196 cr ( 33 pc of sales )

Breakdown of revenues ( by business segments ) -

Generic APIs - 535 cr ( 93 pc of sales )

CDMO - 42 cr ( 7 pc of sales ) - signed a multiyear agreement with an innovator for supply of API. Expect commercialisation wef Q4

Breakdown of revenues ( by target markets ) -

Regulated markets - 84 pc

Emerging markets - 16 pc

Breakdown of revenues ( by therapeutic segments ) -

Cardio - 41 pc

CNS - 16 pc

Anti-Diabetic - 4 pc

Pain management - 6 pc

Others - 33 pc

Contribution from chronic therapies @ 67 pc

Have added 05 APIs to the development grid - 03 are high potency - Onco APIs and 02 are synthetic small molecules

Manufacturing facilities -

Ankleshwar Gujarat - 742 KL ( additional 208 KL capacity will come on stream wef Q2 FY 25 @ Ankleshwar )

Dahej Gujarat - 381 KL ( additional 18 KL capacity will come on stream wef Q2 FY 25 @ Dahej )

Mohol Maharashtra - 49 KL

Kurkumbh Maharashtra - 25 KL

Greenfield expansion @ Solapur - phase -1 of construction has started to set up a 200 KL facility. Phase 2 @ Solapur shall add another 400 KL of capacity. In addition, 400 KL of backward integration capacity is also planned at the same site

Future growth drivers - Onco High Potency APIs, CDMO ramp up, expansion into complex APIs and Iron compounds, pursuing 2nd source opportunities for top generic players, geographical expansion

Future drivers of operational efficiencies - Debottlenecking, backward integration, adoption of flow chemistry in manufacturing

Company’s business with GPL did suffer in Q4. In Q1, there has been a smart recovery and this business is up 18 pc QoQ

Q1 was company’s first Qtr after a long time without the PLI benefits. Hence the contraction in Gross Margins. Slightly unfavourable product mix also contributed to GM compression

Company expects their CDMO business to pick up significantly in Q2

Company had received a closure notice from Gujarat Pollution control board ( in Mid July ) for its Ankleshwar site - citing pollution outside their plant / site. The issue was finally resolved on 14 Aug. Company should be able to catch up for the production loss as 1.5 months are still available in this Qtr

Company doesn’t expect their GMs to go below 51 pc in future

According to the management, upcoming demand environment is much, much better. The brownfield expansion that’s coming on stream should take care of this additional demand over next 1-2 yrs. After that, the Greenfield capacity at Solapur shall kick in

The Bio-Secure act in US is a definitive tailwind for the company’s CMO business - they did acknowledge the the same in the concall

Capex requirements for FY 25 @ around 350 cr. Capex outlay for FY 26 shall also be significant. Hence the dividends payouts, going fwd should be smaller vs past. Also - don’t intend to take on any debt for the planned capex for next 2-3 yrs

Company’s CDMO business currently has 3 commercial projects. Should add another 2 products by end of FY 25. These 2 projects should add 100 cr / yr to the topline. That should take the total CDMO business to around 250 cr / yr. Aim to take it to 500-600 cr / yr in next 4-5 yrs

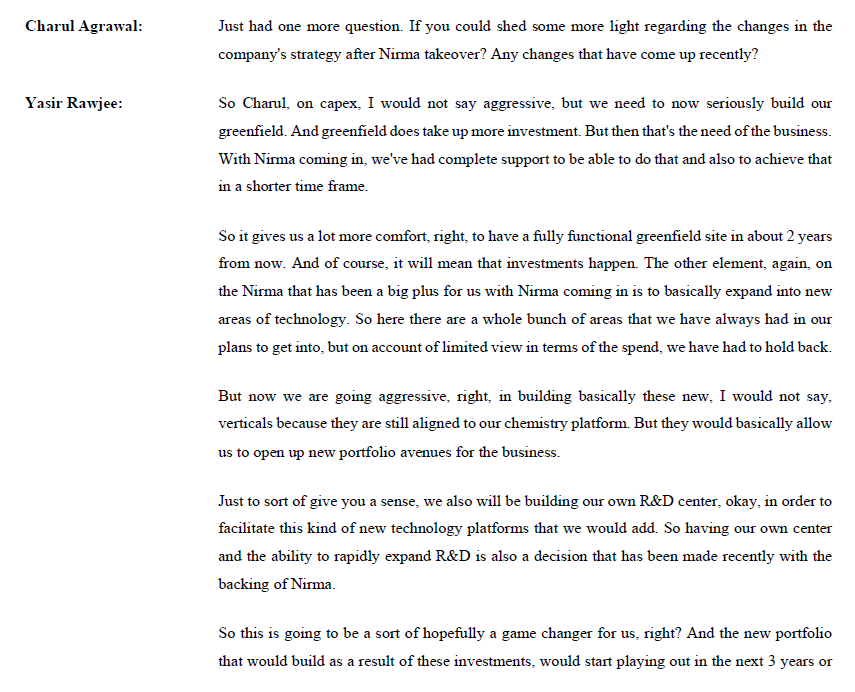

Post the change of promoters and Nirma group taking over, company has become more aggressive wrt Capex

Disc: initiated a tracking position, biased, not SEBI registered, not a buy/sell recommendation

3 Likes

hey thanks and do u use expectation investing tutorial sheets for price implied expectations ?

https://www.expectationsinvesting.com/online-tutorials

The most important risk for GLS is the fact that an USFDA audit is due and there is no line of sight of that. Its generally a surprise inspection and any lapse can derail the whole story.

5 Likes

Isn’t this was expected to complete by 2024? O r I’m missing something…

No, being a green field expansion its expected to be completed by FY26/27/28 in a phased manner

1 Like

Anyone knows what are the top 10 products or API for Glenmark life science?

How did you get the exact number of customers ?

Can anyone help me understand this ? and what happened?

So the doubt is … does the acquirer have to give an open offer of 25% other than 75%? … Won’t it lead to complete acquisition…?

Glenmark Life Science name Changed to ALIVUS LIFE SCIENCES LIMITED (ALS) to establish its separate Brand identity from Glenmark

GLS name Change to Alivus Life Sciences (ALS).pdf (325.9 KB)

3 Likes

I attended the concall. While the company is guiding for a strong H2, the overall guidance has been revised down to high single digit growth from the earlier mid teen guidance. This implies around 20% growth for H2 to meet the high single digit growth. Few things i am unable to understand are.

1 - Company maintained the earlier guidance during Q1 call even after knowing the impact of Ankleshwar closure.

2 - Ankleshwar closure was played down as a minor issue during Q1 call even after repeated queries on its impact. Now they are saying that it impacted in order fulfillment in both API and CDMO.

3 - Revision of guidance downwards is also attributed partially to softness in LATAM markets specially in Argentina.

While business is always dynamic, my worry is company is not able to foresee events unfolding even beyond a quarter or they are not sharing it with the investors. Last FY as well they guided for mid teen growth, maintained it after first 2 Qs but eventually ended up in mid single digits.

Disc - Invested from lower levels.

7 Likes

in Q1 concall Management was confident that the Ankleshwar Facility will start again before 31 July as they are expecting Pollution board closure notice will be taken back by 31 July and they can makeup this production loss bur Closure ban was lifted on 14 Aug (14 days delay from management expectation ) thatswhy they could not produce fully to complete the orderbook. You must been felt that for the first time in Concall Management is seen taking aggressive stance for growth from H2 2025 to 2028. So just keep patience for next 2/3 years

1 Like