May I know the significance of the investment by MIT in GLS? Investing in equities seems to be a regular income generation activity for MIT and they do invest in a wide variety of companies. So, wondering how different it is from any other FPI

1 Like

GLS has signed a new CDMO deal worth $5 millions. Hopefully, the change in promoter company brings in lot more CDMO deals (as the new promoter is not a pharma company itself, at least as of now)

2 Likes

Its a good development for GLS. Management was talking about 3-4 CDMO deals since last 2-3 quarters and its good to see they are getting the traction now. CDMO revenue is very small (7-8%) currently but they plan to take it to around 15% in next 3-4 years. In last quarter they said they plan to do more with new management than what they are doing currently. We should get more updates on the ownership change during the Q3FY24 concall on 24th Jan.

2 Likes

MIT choose some selective small cap companies in india, most of the companies delivered good results & returns so far.

I know few companies Calcom, AWHCL, Equitas SFB, KPIT, WPIL. Their entry is mostly at the bottom of the trend

3 Likes

Thanks for sharing details about MIT.

Attaching below is the screener link for their current holding

https://www.screener.in/people/131399/massachusetts-institute-of-technology/#shareholdings

Hope you find it useful for further study.

1 Like

Here are the latest results and presentation by GLS.

PLEASE go through it and give your opinions.

1 Like

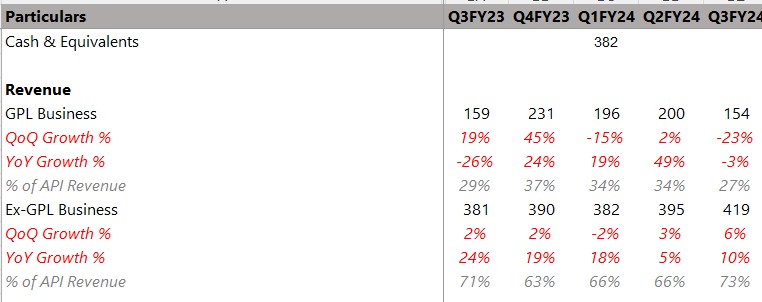

Summary of Q3FY24 Highlights:

Macroeconomic Trends:

- The US economy has shown improvement, and inflation is under control.

- China’s supply situation has eased, contributing to positive macro conditions.

- The Red Sea issue might impact freight costs, leading to a 15-day inventory stocking for the company due to reduced ship arrivals.

Quarterly Performance:

- Volume growth exceeded 10%, with a price erosion of 3-3.5%.

- Geographical growth saw positive trends in India, the US, and LATAM, while the EU business remained flat, and Japan experienced a decline.

- Expectations of a slowdown in the GPL business.

- Gross margin improvement attributed to better input prices, validated supplies, and improved margins in CDMO.

- PLI had a 1-1.5% impact on margins.

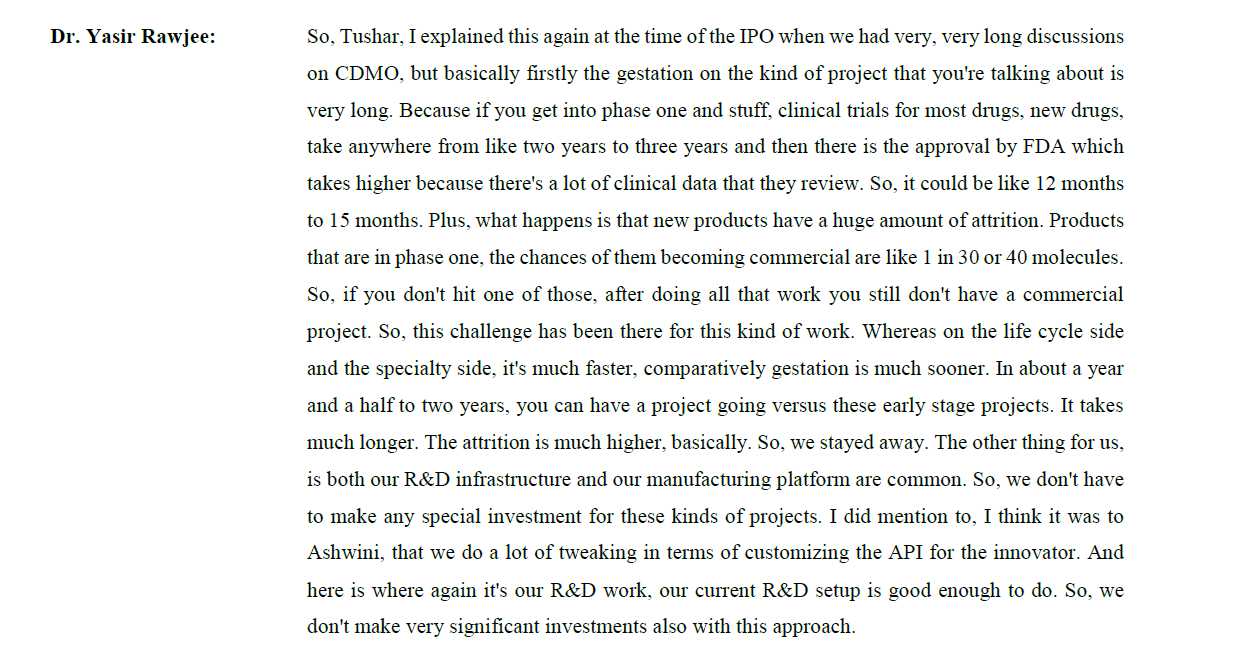

CDMO Segment:

- Confidence in the CDMO segment is high, with a minimum offtake commitment of $5M, commercialization in the next financial year, and ongoing projects in advanced stages.

- One project in the range of $5-10M are expected to be signed in late Q4FY24 or Q1FY25. Company is in advanced talks for one more project.

- Management showed Confidence in the order book buildup, with expectations of CDMO contributing to 15% of the business in the next five years.

- Anticipated CDMO growth implies a target of Rs 4,000Cr topline in the next four years.

- CDMO projects have a long gestation period, with 10-12 projects in discussion.

- USFDA inspections, expected in a 3-year cycle, could happen at any time.

Other Financials:

- Higher employee costs expected in Q4FY24, returning to normalcy thereafter.

- Anticipated reduction in employee costs to 9% from FY25.

- Capex for FY24 estimated to close at Rs 150-160Cr.

- Asset turnover for newer facilities expected to remain at 2.5-3x.

- Opex for newer facilities improving on a per-kilo basis as the company focuses on larger batches.

Product and Filings:

- DMF and CEP filings have exceeded 500, with the addition of four new products in Q3FY24.

- Strong generic pipeline and order book contribute to positive business growth expectations.

Nirma Acquisition:

- CCI approvals received for the Nirma acquisition, awaiting additional approvals.

- The company plans to provide updates on the acquisition in the near term.

View:

- The company anticipates achieving a growth range of 10-15% over the next 3-5 years, propelled by factors such as organic expansion, the introduction of new capacities, and the onboarding of CDMO partners.

- An area of concern for the market was the parent business, constituting approximately 35% of the overall topline (analysts believed it is a inflated margin business, which posed challenges for acceptance). However, in contrast, the company has demonstrated one of its lowest contributions from GLP, and despite this, it has successfully maintained margins as guided, standing at around 30%.

*With ~30% margins, 30%+ ROCE and net cash position, the company can further re-rate. This is particularly anticipated as the looming impact of GLP diminishes with the entry of Nirma. I believe companies like GLS can trade anywhere between 15-20x EV/EBITDA (vs 12x currently and 7x at low).

- One thing to be Aware of: The newer capacities will be giving lower asset turn-over (2-2.5x) vs previously reported by company (3-4x). This is because the assets currently generating topline are derived at slump sale, hence the Asset turns are inflated. Thus, ROCEs are expected to trend downwards too. Nevertheless, the company still can do 20-25%+ ROCEs easily.

Disclosure: Educational purposes only, Not a buy recommendation, I am not SEBI registered analyst or advisor an I am invested in it hence my views may be biased.

18 Likes

I am posting a YouTube video and a PDF of the conference transcript for Q324.

Hope it helps.

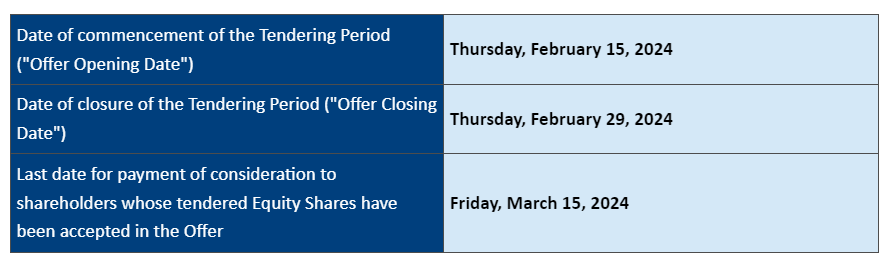

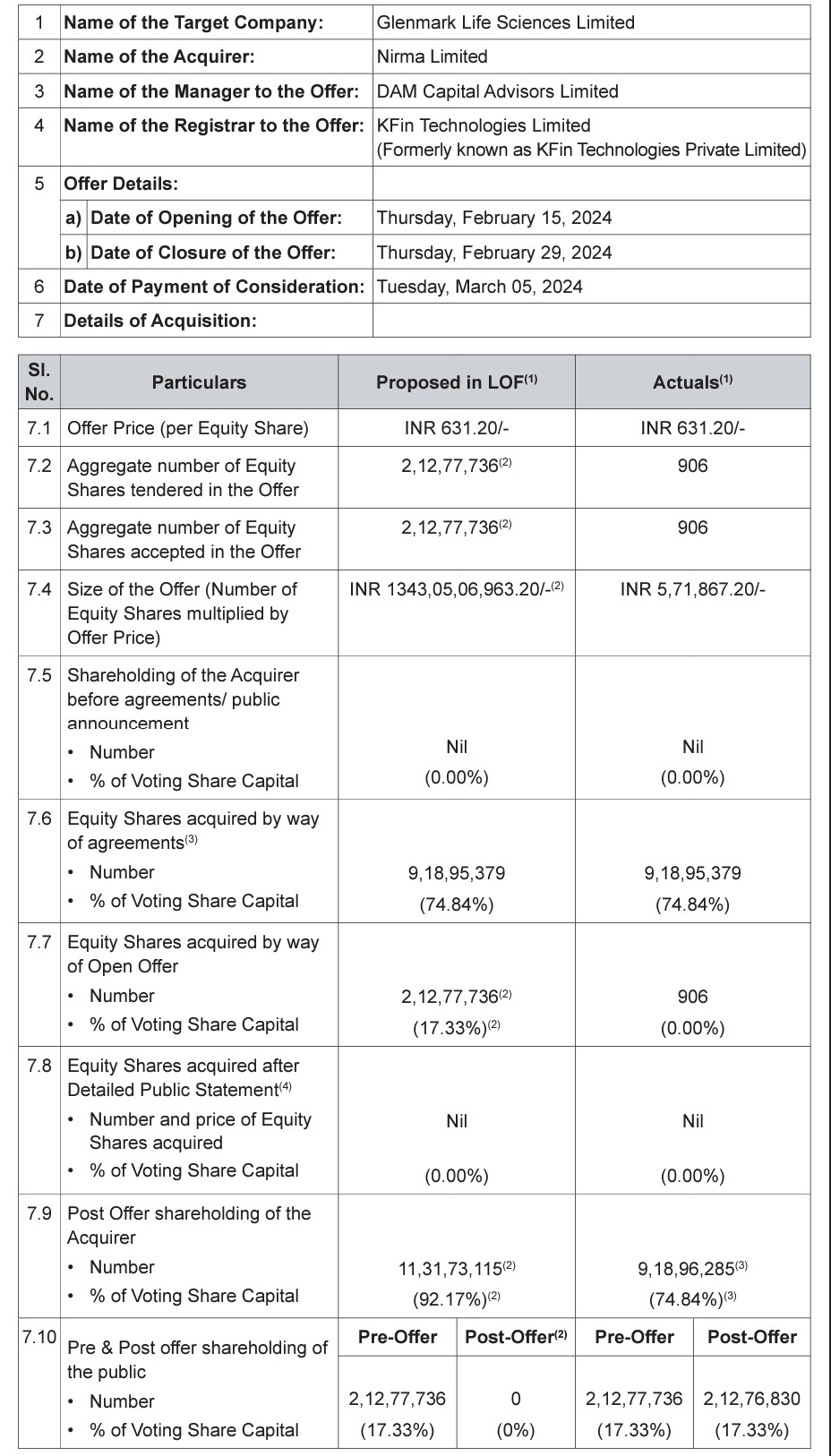

Received the mail intimation about the open offer. Wondering why would anyone tender their shares @ 631 when the CMP is 884 today

1 Like

Seems they are just making offer as the same was earlier announced to happen on 20th November. Anyways, seems its a formality only as no one will offer shares.

1 Like

Yes, also when they buy 75% from Glenmark Pharma, any excess shares they receive has to be sold off within 3 years as part of minimum shareholding norms

1 Like

Nirma Limited is officially the new promoter of GLS after GPL transferred 55% stake to Nirma. Remaining 20% stake will be transferred soon and then the process of sale will be complete.

1 Like

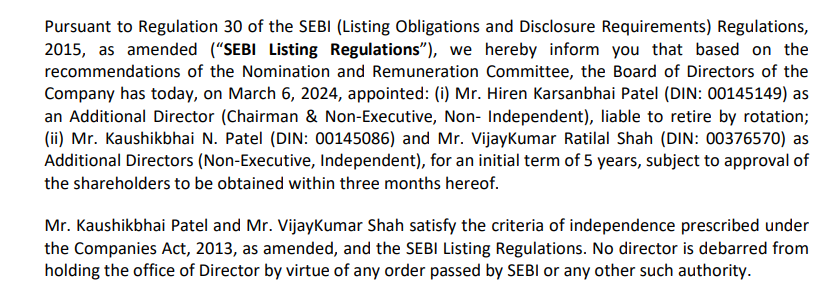

Along with the old promoter, one “independent” director exits

and two new “independent” directors belonging to the new promoter join the Board. Nice! ![]()

Source:

1 Like

(Editing my earlier message as there was a notification by the company about number of shares tendered against the offer)

Expectedly, hardly anyone tendered their shares due to higher market prices

1 Like

Q4 numbers has so many surprises like one time bonus to senior management, differed shipments due to red sea issue & unavailability of flight cargo, differed revenue recognization, Margin drop from Q1 onwards due to loss of PLI benifits

Still i feel lot of value is left in GLS as compared to any other API companies, CDMO rev can hit 1000 Cr on medium term with decent margins.

3 Likes

In Q3FY24, they said since they use air route for their international deliveries, they do not expect much impact except the raw materials which comes via sea. However, they did not anticipate air slots will also be filled due to red sea issues. However, the main concern for me is sudden revenue drop considering they were still maintaining mid teen growth till Q2FY24. Now when they again guide for mid teen growth in FY25 we do not know how it will pan out. GLS management is conservative which is good but drop of almost 10% in revenue from the guided level in 2 quarters is concerning.

Also, there has to be clarity of accounting policy of Nirma as it impacted almost 45cr sales in Q4. Nirma management has also not addressed the takeover so far which is surprising. Reason may be GLS will be run as an independent entity which they mentioned in Q4 concall as well and its good. However, would like to know Nirma’s rationale in GLS takeover and what are their future plans.

Disc - Invested from lower levels.

5 Likes

Any views on OFS by Glenmark?

Personally, I feel that this will remove the overhang of Glenmark balance stake sale and may be long term investors get in around 810 levels.

I am also considering adding more and pyramiding my stake as the margins are amongst the best in category and Mr Yasir leadership will help in decent growth in coming years.

Nirma future plans remain unanswered but seems there will be more clarity incoming quarters.

2 Likes

OFS proved to very successful, probably institution got allotment near 828-830 and retailers got allotment 841-842, heavy volume with high delivery in last 3-4 days has significantly absorb the supply, Probably within weak the full supply will be absorbed. Now stock performance will depend on quaterly results specially the topline growth as everything else is fine.

GLS is expected to continue its 90% Complex Generic API supply with 10-15% CDMO until Solapur Plant comes online.

But a interesting thesis has come from Sh Kenneth Andrade of Old Bridge Capital that by 2030 Indian Generic Pharma will be at the same spot as Indian IT Sector. Indian Generic Pharma will consolidate & capture world Generic Market by 2030. If his thesis remains valid than GLS will be a major beneficiary. Hopefully the Growth will start appearing in GLS in next couple of quaters which is missing from last 2 years.

4 Likes