anyone sees any fundamental concern for API manufacturers or Gland in particular? Why is stock getting hammered so much?

- India Business : Intense pricing pressure, they can’t say anything now on what would be the base

- US : Earlier when a new product is launched they usually enjoy very high gross margins for almost first 12 months, not anymore, there is huge pricing pressure on new launches as well

- GCC Markets are good in terms of margins compare to other ROW markets

- Biologics CDMO , burning cash of 19cr a quarter, some customers in the final discussions

- China - This quarter they are hoping for some breakthrough

- Overall this year will be very flat

5 Likes

“Mr Guo does not appear in imminent danger of sharing their fate. But his company is in trouble. On October 25th Moody’s, a ratings agency, downgraded Fosun’s debt deeper into junk territory. Chinese banks have been asking the firm to provide more collateral for loans. To meet its obligations Fosun has already divested $5bn-worth of assets this year, according to data from Refinitiv, a research firm. By 2023 it could shed $11bn-worth. That is quite the reversal for the asset-hungry group. It also marks the end of a freewheeling era in Chinese business, which is turning inwards under President Xi Jinping.”

Disclaimer:

Experience from past learnings. Saw my friends burn their hands in GE power on the thesis of FGD installation inspite of problems at parent level.

Gland at parent level seems to be going through multiple problems as indicated by the article. Always tread with caution in such cases.

Not invested. Studied the business, ended up avoiding as didn’t pass the management filter due to parent level problems.

8 Likes

Thanks Ishmohit,

Besides parents issues which you highlighted, Gland also seems to have their own issue. In Q1 concall they gave the reason for shortage of syringes - my mistake 1 trusted them.

In this qtr they say shortage of bags and stoppers etc. As per me no other co says such a shortage. Also gland doing capax with 500 people - I don’t like it. Q1 call they committed margin and growth numbers - in Q2 call they seemed confused, noncommittal as of now.

Mistake 2 not fully exited post results (take more time for me to listen to recorded concall, loss of investing part time).

Disc: Have invested in IPO, Partially exited this week. Good lesson learnt not to trust management fully.

This is my views - I may be wrong - not an advise to sell etc.

6 Likes

https://twitter.com/ETNOWlive/status/1597481581975072769?t=L1Lc-VimgI751M3uHjNAqQ&s=19

Interesting news

From BQ

Key Benefits

- Cross sell products to Gland’s existing customers that are doing business in Europe - at the moment these customers are sourcing for their needs in Europe from other vendors, now Gland can offer them services from Cenexi plants

- Gland can cross sell products to Cenexi customers

- Gland can leverage from the technology strengths that Cenexi has, in terms new technologies like NDDS, needleess injections, ampoules , Ophthalmic suspension Gels etc…

- Unlike US , Europe market is dominated by branded Generics (same like India), so the price erosion is not an issue, product portfolio is pretty stable

- Key customers have very long relationships and Cenexi is the sole supplier, these customers very big in branded Generics

- Gland can explore the opportunities to cross sell APIs (At the moment Cenexi is sourcing from elsewhere ) to Cenexi

- Europe is very strong in Pharma Manufacturing, Europe capacities are more or less same in terms of production, their fixed costs are high in terms of labour costs but their capacities are same as Indian players, they have achieved this due to more spending on automation, this is the key strength that they have, Gland will learn this and implement in Indian sites

- Most of the product portfolio is in licensing type and do contract manufacturing for branded players

- There is a strong trend going on since covid, to produce more locally in Europe (especially key products ) , this trend will continue, current energy crisis just slowed down this process bit but this trend will continue

- No product or customer concentration

- Current management is working for many years so they will continue to run the business (the way Gland is working right now )

- More focus on existing capacity utilizations (some new lines are added )

- Current capacities (other than one in France) are running around 30%, some capex is in progress in these sites by adding in lines, the utilization will go up in coming years

- Biologics - Working on three products, validation batches delivered

- Gross Block - 90 Million Euros

- Working capital days are stable

- Unlike US, in Europe all the contracts are written with a review clause that is linked to inflation hence the margins will be stable (current power issues are kind of one off )

- Some of the approved products manufacturing can be done from India

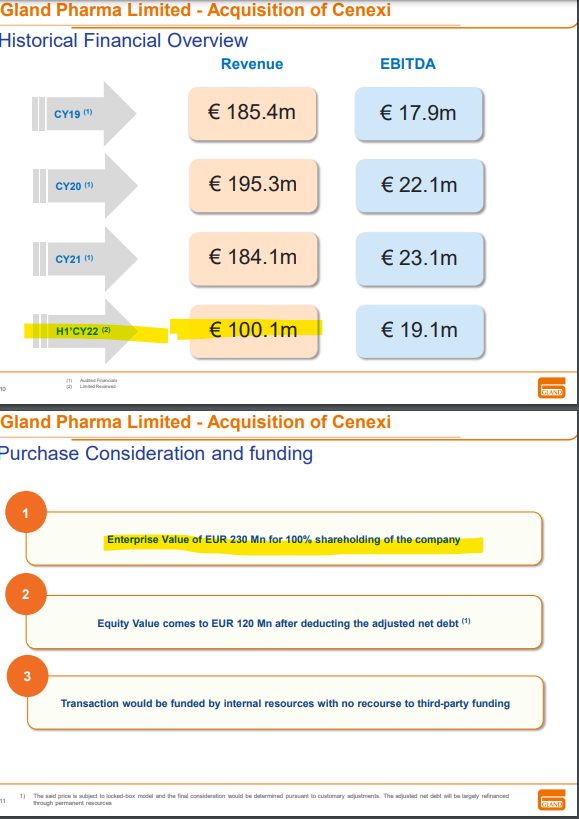

- Deal will be completed by March 2023 , post merger consolidated margins will be down , they go back to normal over a period of time

- Apart from this acquisition, still exploring other inorganic opportunities

Gland Updates

- Supply Chain issues are normalised (syringe shortages issues are sorted almost 90% )

- Logistics costs are coming back to normal

- Due to high price erosion many players are getting out that is causing some shortage and some assets are put on sale , in another 3-4 months this will settle in

- Though there are shortages in some products but unable to react due uncertainties in building inventory to capture these opportunities

5 Likes

1 Like

Does stake sell by Fosun have negative implications? Isn’t it good if a global pharma major purchases stake?

Red flags were there

https://twitter.com/BeatTheStreet10/status/1577154825124737024

4 Likes

Did not see this earlier but seems like a secular downtrend in their business and poor management execution. Very worrisome especially withe the ownership overhang.

Disc: Invested but reducing size

Hi Everyone ,

Went through the red flag’s tweet shared by @StonePitbull , really helpful indeed for anti-thesis pointers. But as the stock is driving into deep pessimism(CMP - 895) and Stage 4 . Felt like diving deeper and saw some positive pointer’s in place too . Do your own due diligence to see what outweighs more : But I have summarised it in this tweet - https://twitter.com/Lakshayy_99/status/1660518460932386816?s=20

Putting it on this thread too :

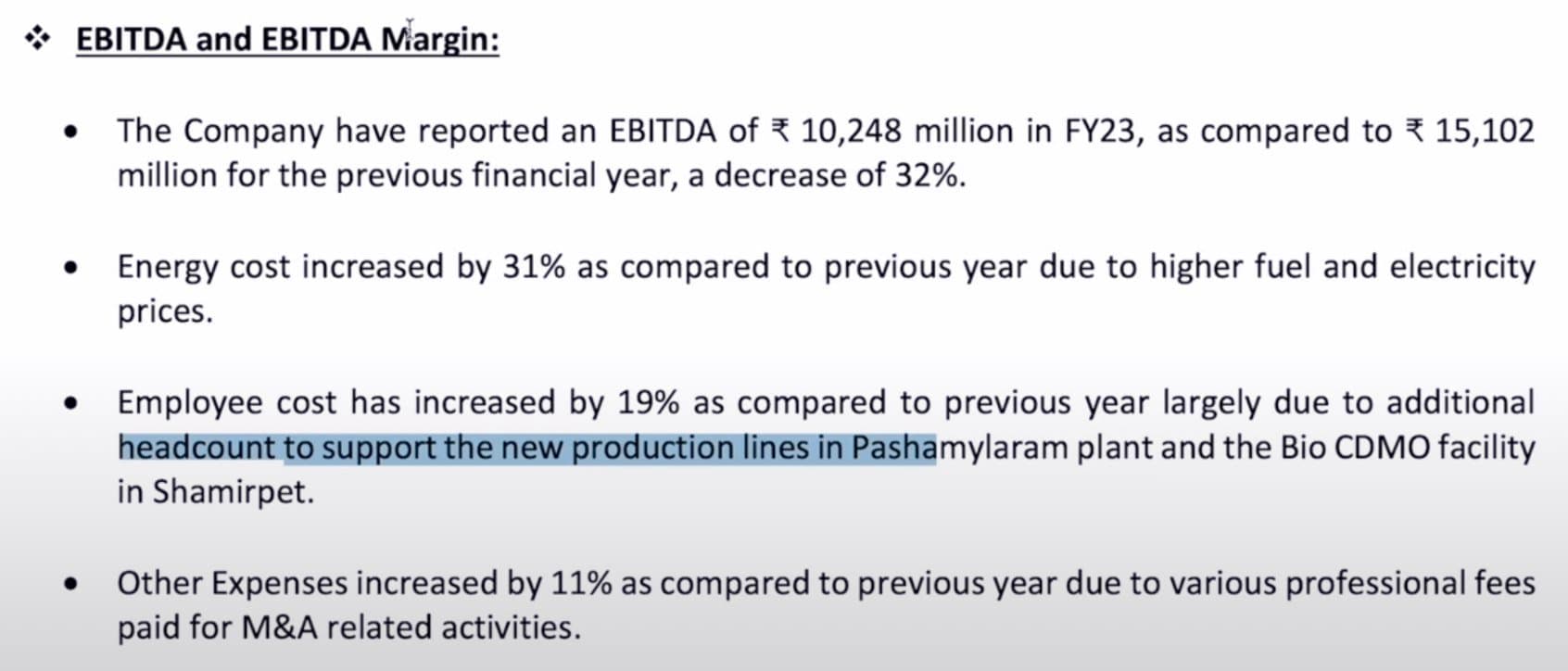

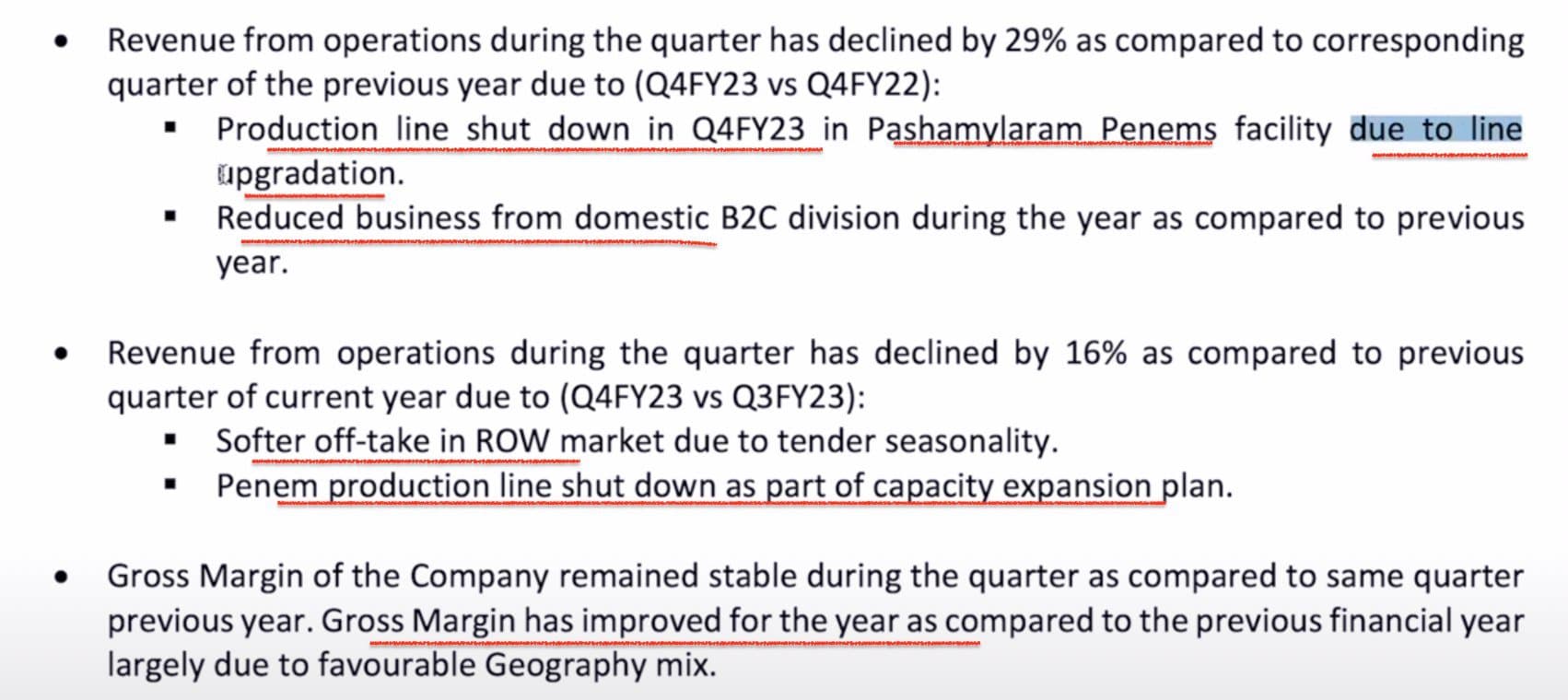

The fall in the profits have been tied to the fact because of one of the plant enhancement due to which there fixed cost causes an impact , with additional employees leading to further impact on EBITDA

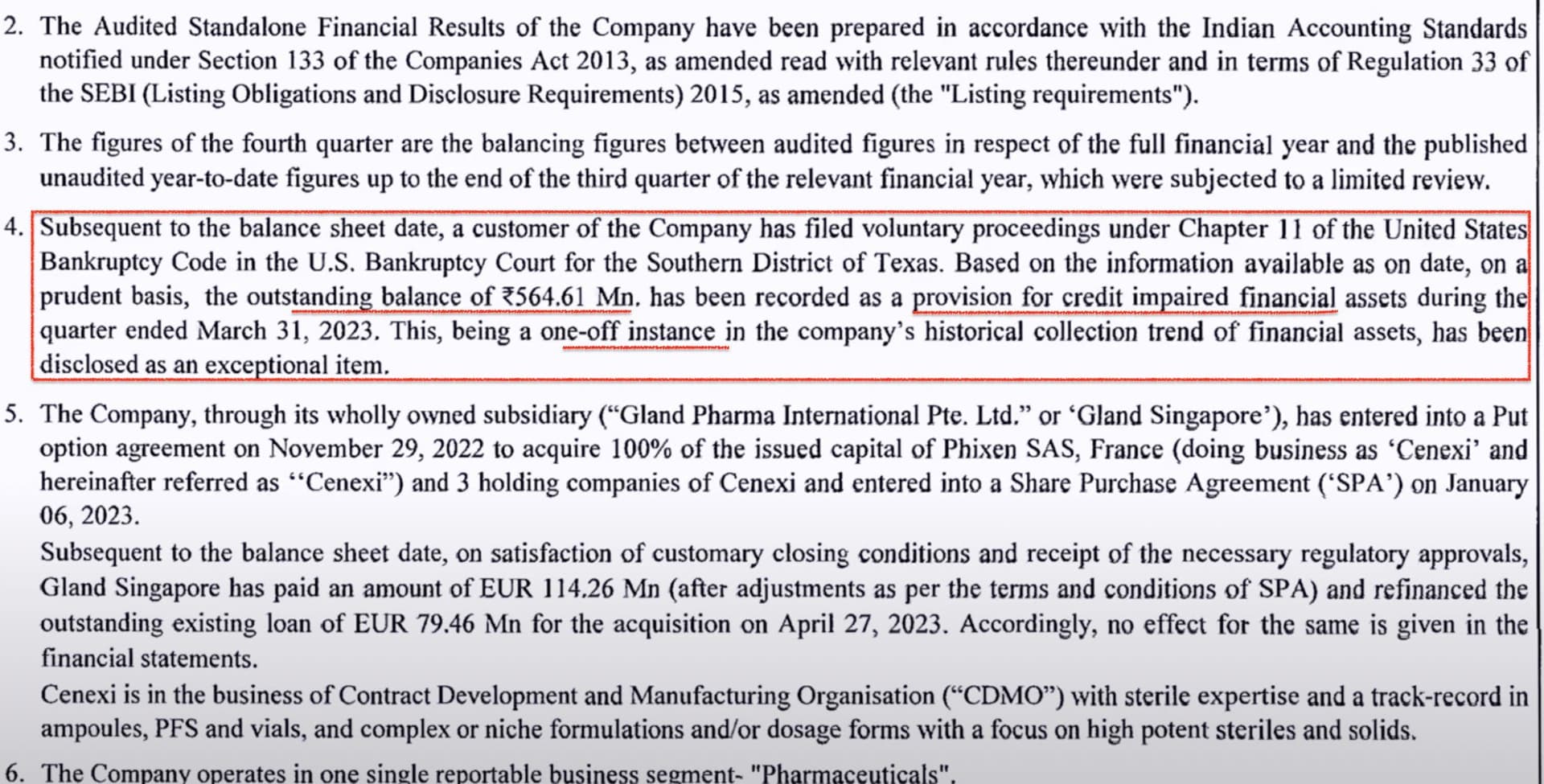

Reasoning as to why the profit has taken a toll this quarter , Additionally 56Cr one off expense because of a US company defaulting as it filed for bankruptcy (Highlighted below)

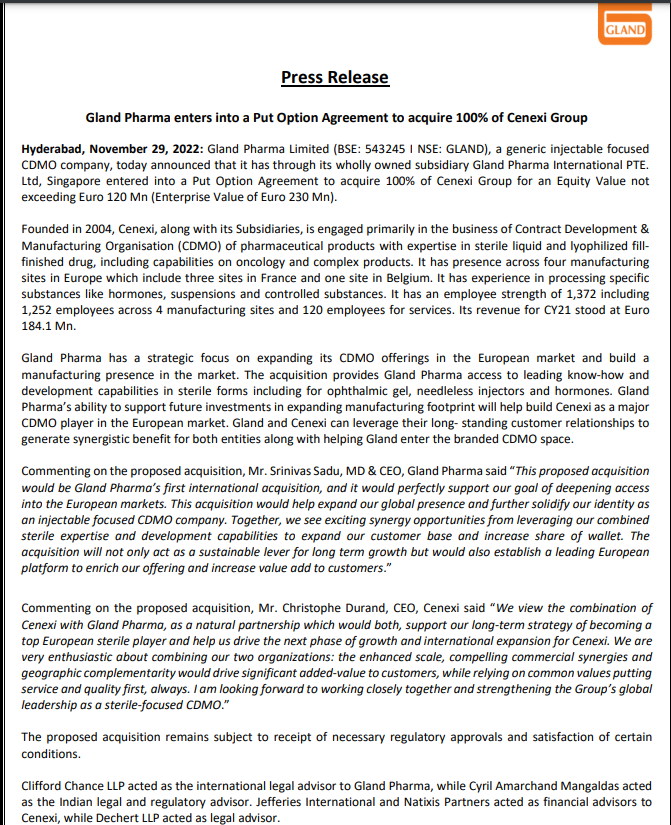

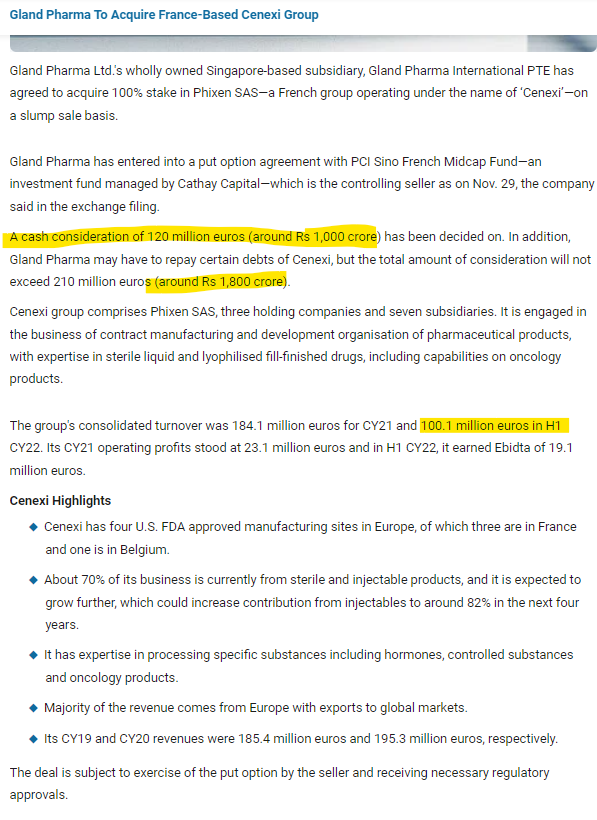

Also if you see point 5 , the acquisition of Cenexi(1000 Cr ) . Whose payment would be taken care from it’s cash equivalents of 2770 Crs ( It’s revenue of 1600 Cr on a yearly basis would be added considering the current euro price ) .

So in future can see top-line inching north of 6000 Crs.

Please correct if I am wrong somewhere , and would appreciate other investor’s view on this .

Disc : Studying and tracking , no recommendation !

7 Likes

Vivek Singhal has shared this info in youtube video Gland Pharma Latest News | Best Stocks To Buy Now - YouTube

1 Like

above all pointer are disclosed in vivek singhal sir video,as such this company likely to grow fast bcz its in a stage 4

1 Like

Anyone tracking this company? The results look solid. There is a cup and handle when it comes to technical patterns

1 Like

Gland Pharma Limited disclosed the unannounced US FDA inspection at their Pashamylaram Facility in Hyderabad, resulting in three 483 observations.

1 Like

Despite accumulation of shares by institutions, the stock price has corrected sharply from ~2200 highs to 1700 right now, looks interesting

2 Likes