Though not related to Gland Pharma, I thought it is worth sharing as the discussion is about ESOP.

4 Likes

Good Cogland Bernstein.PDF (1.4 MB) verage - Available in the public domain

5 Likes

Very comprehensive coverage (you will feel like you are reading DRHP ![]() )

)

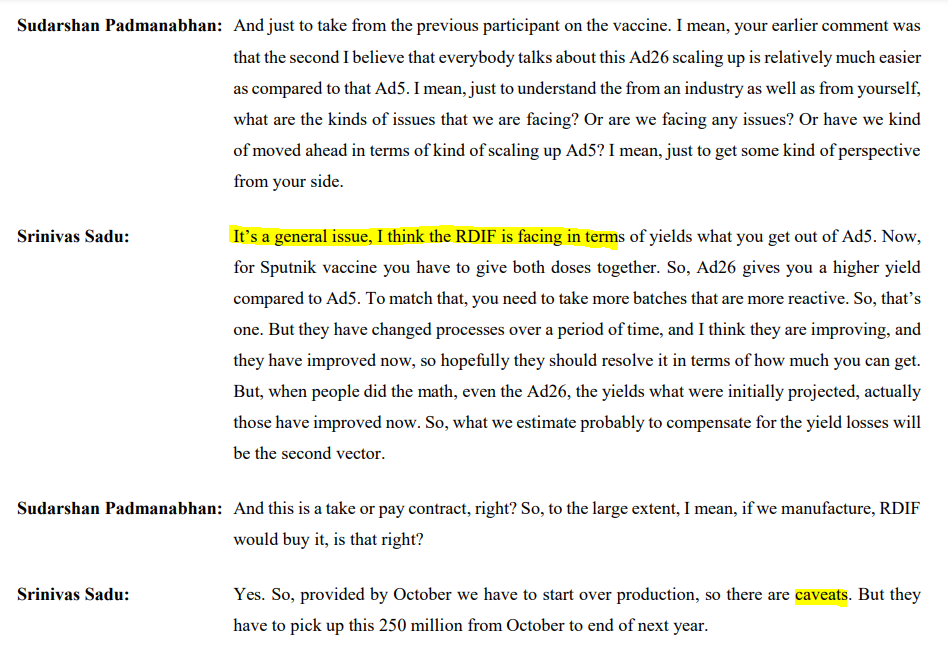

Last concall Mr. Sadhu said nothing much from China at the moment. China itself is huge market after US, with strong Parent backing I think has huge advantage.

Interesting to see (they have about 5 approval pending in China ) .

Multiple triggers to watch out

Covid gave the opportunity to get into non regulated markets , I guess this will become sticky in nature

Investments in biologics (starting with Vaccines )

Unlike other generics (where price erosion is quite common), injectables are still high margin products in NA , gland is the leader in this space from Indian origin players

Lot of cash in the books, so may go for some boltons (like they did last quarter Vitane Biologics to strengthen their vaccine manufacturing capabilities )

Regarding ESOPS, there very companies who don’t encourage this at all, for example SUMITOMO, this japanese company stands out from the crowd, no ESOPS and no royalty payments to the parent.

2 Likes

Could you please elaborate this article in a quick summary, as I’m unable to read it. Thank you.

GOOD NOS FROM GLAND.

Concall at 630 PM today

4 Likes

ROW Markets on grwoth path , continue to work on improving our market share

Are these numbers(gross margins) sustainable ? We will try to maintain

China - We can launch atleast one by end of this year

China Market Opportunity - $550 Million Opportunity

Vaccine - Partnership with Hetero for drug substance and fill - finish

Sputnik Timeline - October - November launch - on track

Gross Margins - We are B2B company so we cannot expect major changes on the margins front

India - Delta of 30 crores revenue this year is is due to covid related drugs

8% of the revenue from Profit Share model

What is driving indian and ROW ? (Cost or Supply chain issues )

Cost advantange and product basket and advantage of selling the products in US, so it is easy to getinto to these markets

3 Likes

It’ll be interesting to see what valuation the market assigns given 40% projected EBITDA.

Also no talk of dividend. Why?

1 Like

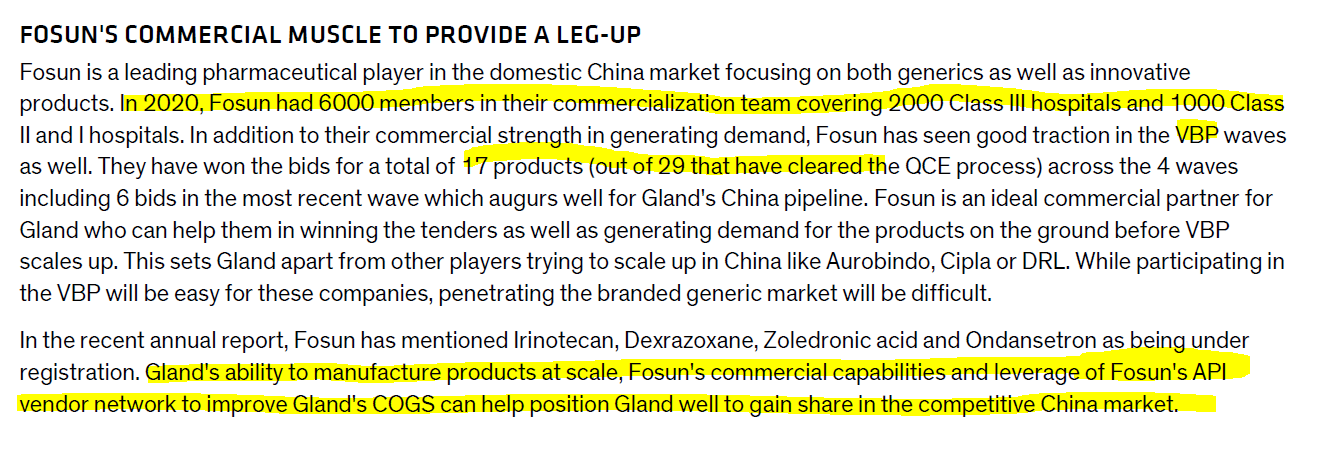

Adding few additional points

- CDMO opportunity :Shanghai Henlius subsidiary of Fosun is expanding thru new 2-3 plants looking to outsource some CDMO work which i think Gland can easily grab !

- Tech Transfer : If Gland is making ₹100 in total, approximately 75% to 80% actually comes from transfer pricing, and a much smaller portion comes from profit share in long term basis. Initially the profit sharing contribution are high but LT average is 20-30% in Tech transfer . Gland receives : A) cost of goods plus B) the conversion cost and C) some margin overhead. (Transfer Price: A+B +C ) + 40-50% in Profit . Looks like a great margin to me.

- Overall Market size: The U.S. market total generic injectables are almost $40 billion, $45 billion removing biologics 30 BN. ANDAs what we have already developed and approved, it’s around $ 11 billion.

“And we have five ANDAs to be approved around $3.5 billion. So, if you consider everything, around $14 billion already we have filed or tentatively approved And if you see next five years, another $13 billion products are going off patent, out of this complex will be around $5 billion. So, around $7 billion is still there in the normal injectables and about $5 billion on the complex, so we are also working on the complex right now”

3 Likes

From Motilal report

Gland pharma

Highlights from the management commentary

-

GLAND expects US sales to grow by 18-20% YoY in FY22.

-

It is working on 14 complex products, of which two/three will be filed in FY22/FY23. It is developing 25-30 complex products over the next 2-3 years.

-

The management indicated a capex of INR5.7b for FY22, of which INR3b is to be spent on the vaccine facility (INR1.2b spent till date). It has guided at an overall capex of INR3.5b in FY23.

-

The management expects to sustain fixed asset turn at 3.5-3.6x, including the upcoming investments in the Biological segments.

-

It has signed a contract with Hetero for the Sputnik vaccine. Trial batches of the same were completed recently. Manufacturing would start from Sep’21.

2 Likes

Business Overview

COVID Treatments

Enoxaparin, Rocuronium, Cisatracurium and Atracurium

Also started the manufacturing Remdesivir and supplied around 1.68 million vials in FY 2020-21

Financial Performance

Revenue Growth - 32%

EBIDTA Margin - 40%

PAT Margin - 29%

Market (Geographical) Growth

USA (21%) Canada(41%), Europe (29%), ROW(136%), Australia (23%), INDIA 19%

Our strategy of geographic expansion into emerging markets such as Singapore, Israel, Saudi Arabia and CIS (Commonwealth ) countries through our new partners also showed promising results. Our Rest of the world business grew rapidly at 136% y-o-y, accounting for 16% of our revenue in FY 2020-21. We expect to further strengthen our presence in the global markets, with multiple product launches scheduled in the coming fiscal.

New Launches

We have launched 47 product SKUs of 28 molecules during the year and the key launches for the year were Micafungin, Ziprasidone, Bivalirudin RTU and Olapatadine Ophthalmic (OTC).

Growth Levers

In FY 2020-21, total R&D expenditure was 1,220 million, which is nearly 3.5% of our revenue from operations. We have identified certain niche capabilities that need to be built on both the development and manufacturing front, towards which we are adding resources internally as well as evaluating external targets. As of March 31, 2021, we along with our partners had 284 ANDA filings in the US, of which 234 were approved and 50 were pending approval.

More focus on backward integration.

We are also exploring M&A opportunities to acquire companies, products and technologies that will add to our capabilities and technical expertise. We plan to acquire capabilities to strengthen product and technology infrastructure, such as long acting injectable’s, steroidal hormonal products, suspensions, anti-neoplastics and, nasal and inhalation products. We are also looking at niche API suppliers with complementary capabilities, especially in fermentation technology, corticosteroid APIs and hormonal APIs. Geographically, USA continues to be our primary market and we are looking at inorganic routes to enter the Controlled Substances market in the country, which is otherwise restricted. We are looking for assets that fit our strategy and culture, especially in terms of quality standards.

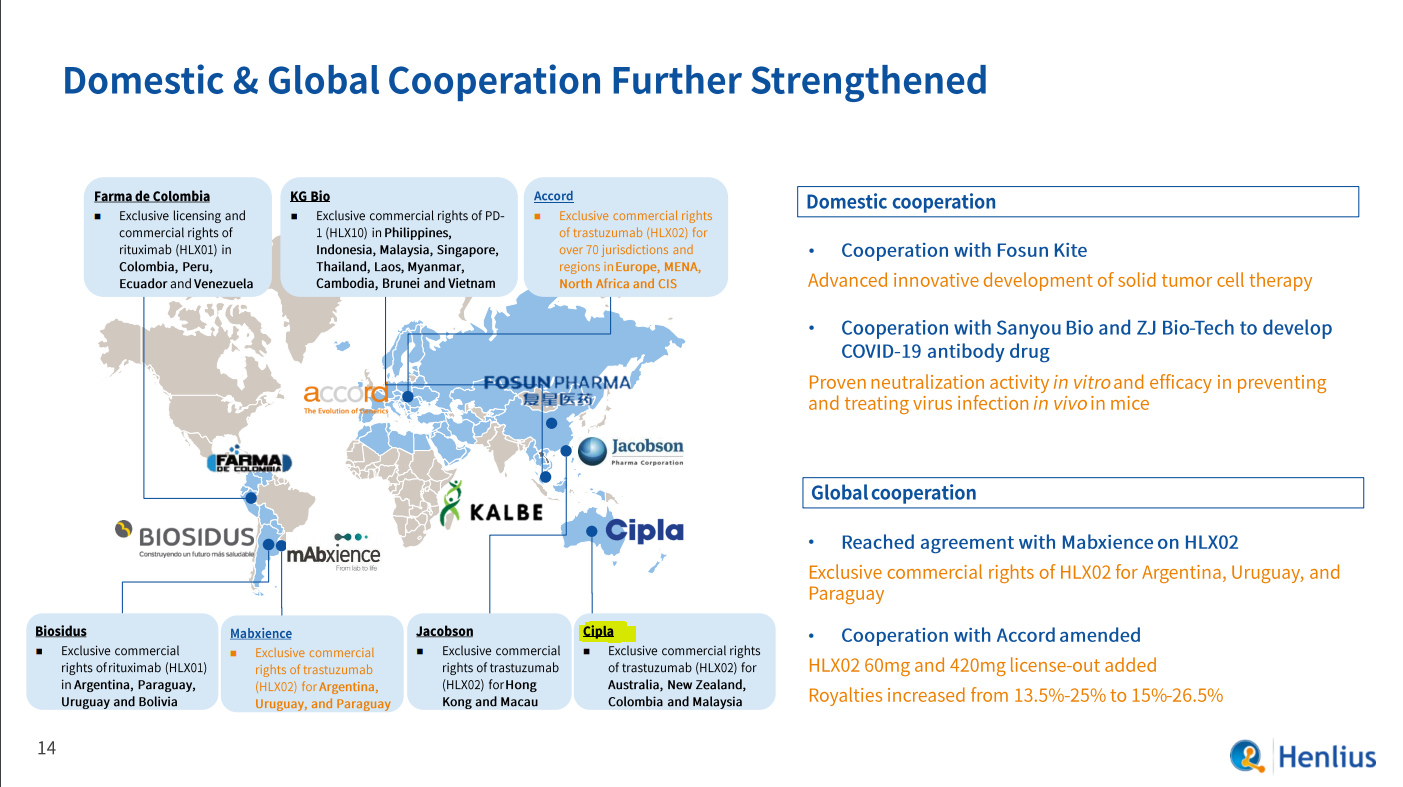

Fostering our ties with Fosun Pharma, we are taking strides to penetrate in an otherwise difficult market of China, where we have already made six product filings and are also developing China-specific products

Our agreement to manufacture Sputnik V vaccine of Russian Direct Investment Fund (RDIF) only validates our unique competencies. Enthused by the robust demand across product segments, we plan to continue investing in creating infrastructure in the vaccine and biosimilar space. Cost competitiveness, improving efficiencies and increasing speed-to-market will always remain our priorities. Going forward, our market leadership will be clearly driven by delivering sustained high margins and strong performance across key financial metrics.

Our growth strategy includes both organic and inorganic plans. We are establishing capabilities in niche technologies like LAIs, Suspensions, Hormones, Peptides, both on development and manufacturing. Our inorganic growth plans are focused on acquiring new technologies, strengthening vertical integration and also growing by way of geographic expansion, which are part of our long term growth strategy.

Top 5 Customer Contribution reduced from 48% (fy19) TO 40% (FY21)

Revenue contribution from existing vs new launches (89%/11%)

Attrition Rate - 15%

Capex (770 crores planned in FY22 AND 23)

Adding new lines at our Pashamylaram facility (Debottlenecking)

Capacity expansion of Visakhapatnam API plant with the addition of new block (brownfield )

Acquisition and expansion of Biotech Drug Substance plant (Brownfield capex for vaccine )

Inorganic Growth Strategies

Acquire Niche Technologies

Acquire assets providing access to new geographies

Investments in assets that strengthen backwards integration

Acquires assesses providing new manufacturing capabilities

Intellectual capital

268 Employees in R&D

3.5% revenue sepnt on R&D

85 own approved andas

149 approved partner andas

1501 product registrations globally

As on March 31, 2021, Gland Pharma has 12 registered patents. It has applied for the registration of 13 patents in India.

Technology Barriers

Some of our success stories include synthesis and characterisation of glycosaminoglycans, including heparin, low molecular weight heparins, chondroitin sulphate, hyaluronic acid and drug conjugatesof glycosaminoglycans. We also

possess the technology to develop complex steroids such as vecuronium, rocuronium, fulvestrant and vitamin D analogues

The sterile API technology has enabled us to successfully develop betamethasone acetate, paliperidone palmitate, loteprednol etabonate, aripiprazole hydrate and aripiprazole lauroxil. We have also developed non-infringing polymorphic forms of APIs, such as Tigecycline and Bortezomib, and novel processes for oncology APIs, such as cabazitaxel and pralatrexate.

Key Triggers to Monitor

Next inorganic acquisition (Zero debt company and cash of 500 crores on the books and strong promoter backing )

China market play

Growth in non regulated markets and other CIS countries along with India market

6 Likes

The dependency on US Generics is becoming a dampner going by the recent results of Dr Reddy and APLLTD. We need to see how far this phenomenon penetrates in to other companies. We need to analyse each company going forward on this basis and then take a call. In fact, APLLTD openly said that they are trying to mitigate this by getting into domestic market. One expert in pharma warned specifically Gland can lose market share and face price erosion. Need to be cautious on this

I have an counter example heard from an Pharma expert that Jubilant is doing quite well in spite of FDA warnings at India plants because of their US plant doing well and made in USA serving in USA gets far better realization which counterbalances india business. Can be checked . Haven’t gone and checked myself ! US market is tough that’s a valid point !

1 Like

@sethufan Gland is into Injectables segment which itself having lower players due to stringent regulations. Also, there are more shortages happen as if players in this segment gets USFDA notices then they cant manufacture the injectables in those plants.

If you see Gland has not got any observations in the past from USFDA. It does not mean they will not get in near future but the chances are less.

Most of the competition is in Oral Solids where the APL, Dr Reddy’s are present and hence the companies in this segment will face the heat.

Disc: Invested

3 Likes

A number of Indian generic players are going big into the injectable market which will lead to sharp price erosion over the next few years. Please see SOIC observations above or track the big players like Lupin or Sun getting into this segment. DRL also possible. It is a centralized hospital purchase in US.

About SOIC observations : Strides and Sun Pharma not entering injectable space

Source (Stride inv ppt Q1 FY22 & Sun Concall Q4 FY22)

APL has been a slow mover in injectables as they have not been aggressive in this space in terms of no of ANDA etc are stagnant ( not sure but that’s my reading on valuepickr forum says). I had made a detailed analysis video on Gland post Q1 call on my Youtube channel and for the benefit of this forum ried posting here but flagged by Admin:)

4 Likes

Why Kmps, directors selling shares in gland pharma? Is it sign fr some trouble?

1 Like

Mostly people sell their ESOPs, this is normal. There is no promoter selling,

Q1FY22 Concall

Transcript

Investor Presentation

So far (correct me if I am wrong ) none of the indian companies who secured orders from RDIF have announced they are ready to manufacture sputnik vaccine including Stelis.

Looks like there are some real challenges there …

@ankush12495 , please share your thoughts

Key things to monitor

Sputnik production by November

China product launch (end of this year they are aiming to launch one product ) impact will be next financial year

Cash of 3057 cr on which 570cr capex in FY22 , what they are going to do with the remaining cash we have to see

Diversifying the sales - US 55% and ROW 45%

Another interesting fact

Investor presentation of Henlius and Cipla is already working with them in Austraila

2 Likes

I dont think they are going to manufacture. It is only filling margin will be less. We dont have full details and there is no clarity on how much it will contribute can anybody help me in doing the maths