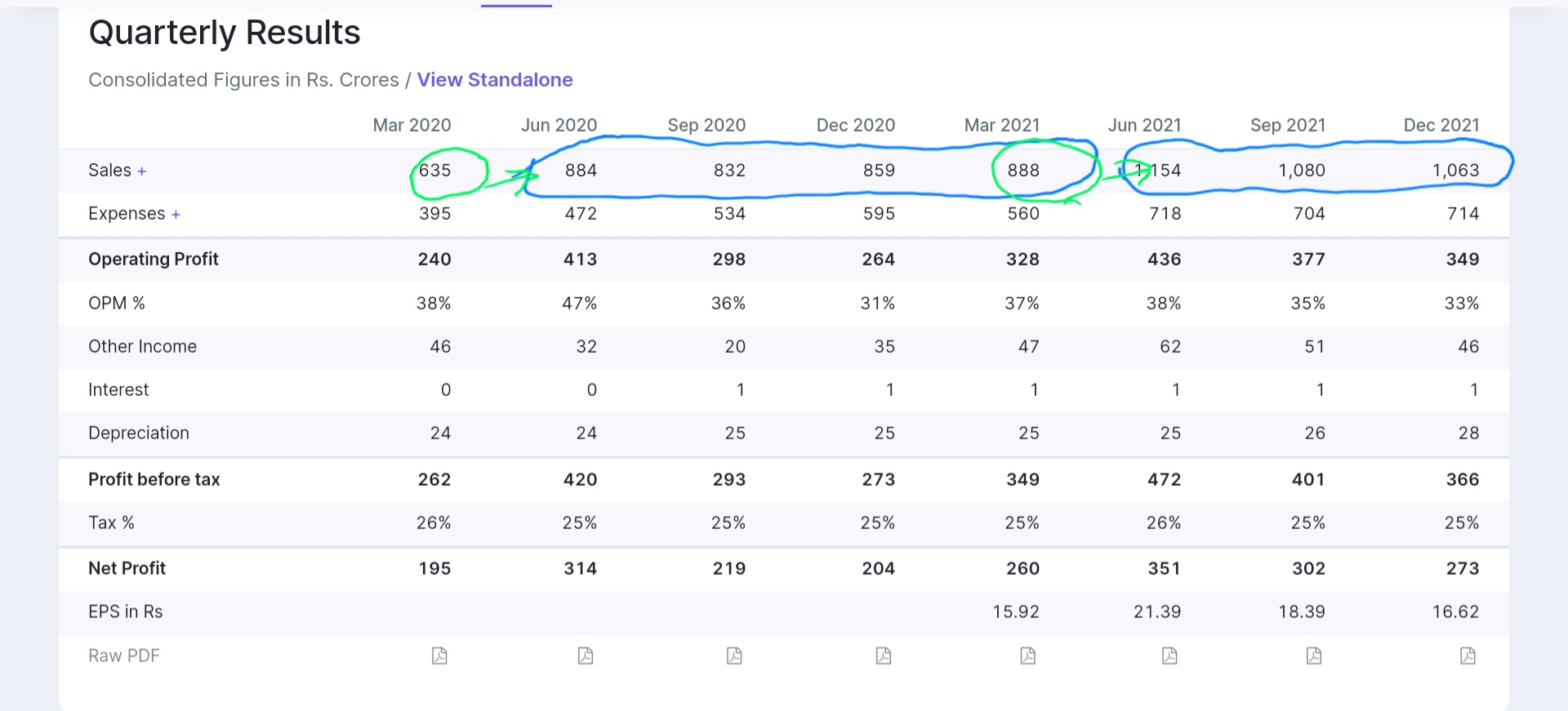

Gland numbers seem to show an interesting pattern

March to June is a sizable bump up, both in FY 21 and FY 22 and rest of year is kinda flat on QoQ for remaining quarters. Ofcourse limited data and Covid periods included.

One possibility on above pattern

- Meaningful Lanuchs concentrated in early part of year, for example. Q3 22 also they filed more Anda/dmf than they did in Q1+Q2 Together. Which will get approvals in 6 mo+. Not a fully convincing explanation but happy to hear others tracking it.

- Clear pattern of core markets contribution declining in overall pie and RoW increasing - inline to their long term ambitions of 60:40 - quick thought would be that this will dilute margins - not the case because they being B2B - capacity utilization matters more than gross margins to get similar EBDITA, RoW engine provides that lever.

- Competetitive landscape on Injectable- FY 23 will see lot of Indian players see capacity coming online, mgmt response was clear that we have 300+ approval, new players will take lot of time to build a meaningful approval base. Infact Gland can use their capacity as well ( assume they have good order backlog and chose to outsource some)

Growth areas-

- Complex Injectable - filing for four complex Injectable, seems lengthy and complex process and took them time higher than anticipated.

- Biosimilar CDMO as next growth engine - lot hinges on it, mgmt seem to be looking at development for now, no commercialization ready molecules. Going to be lumpy.

- Sputnik - Gland is ready but Gamelia and country specific production approval needed to start mfg - Q1 23 probably given didn’t sound sense of urgency yet.

- Capex of approx 500 cr by end of year - at historical 3X assets turn could add 1500 cr next year

- Peptide Foray - some APIs internal, mostly outsourced, looking at acquisition

Key monitorable

- Fosun related biz on biosimilar not materialized yet, delaying biosimilar ambitions

- RoW push shows developed mkt saturation in their approved 300+ molecules, new launch universe in Developed mkt may slow down growth

- Capabilty gaps to be filled on longer term growth drivers- biosimilar, Vaccine, complex Injectable, peptide etc.

- Competetion catching up faster than anticipated in Injectable and pricing erosion

- Being a B2B player - operating leverage is key, have delivered so far well. Smartly using RoW space to achieve it.

Valuations seem rich given upcoming competetion in generic Injectable and required capability built up around future growth areas being work in progress, will market start factoring transition risks to new era? As it is Pharma sector seems out of favor with stalwarts like Divis etc comfortably breaking key support levels. Gland key support levels being around 3400. Though long term story seems intact as long as they successfully transition to Futuristic bio tech landscape.

Invested