You cannot blame on poor Corporate Governance. If you go through the last Concal, management had clearly indicated that big orders from Govt can start flowing any time.

Jan 2008 high for the stock was Rs 80 and now it is available at 100…

There is no harm in loosing initial 10 to 20% rally when there is a decadal opportunity… People now entering will have a benefit regarding certainty of Smart meter project… If you are looking for long term investment its always good to onboard when things are more clear…

Concal Excerpt for reference:

Capacity utilization is around 40% to 50% in the current times due to the shortage of raw material and what we feel the way we have done the planning in last two quarters and the

way that things are getting normal every day - by the end of June I would say second quarter of the next financial year capacity utilization will start getting better, will start

reaching the normalized phase from July end. Once the capacity utilization gets normalized

the margins will also get better than previous levels but it will be from Q3 or Q4.

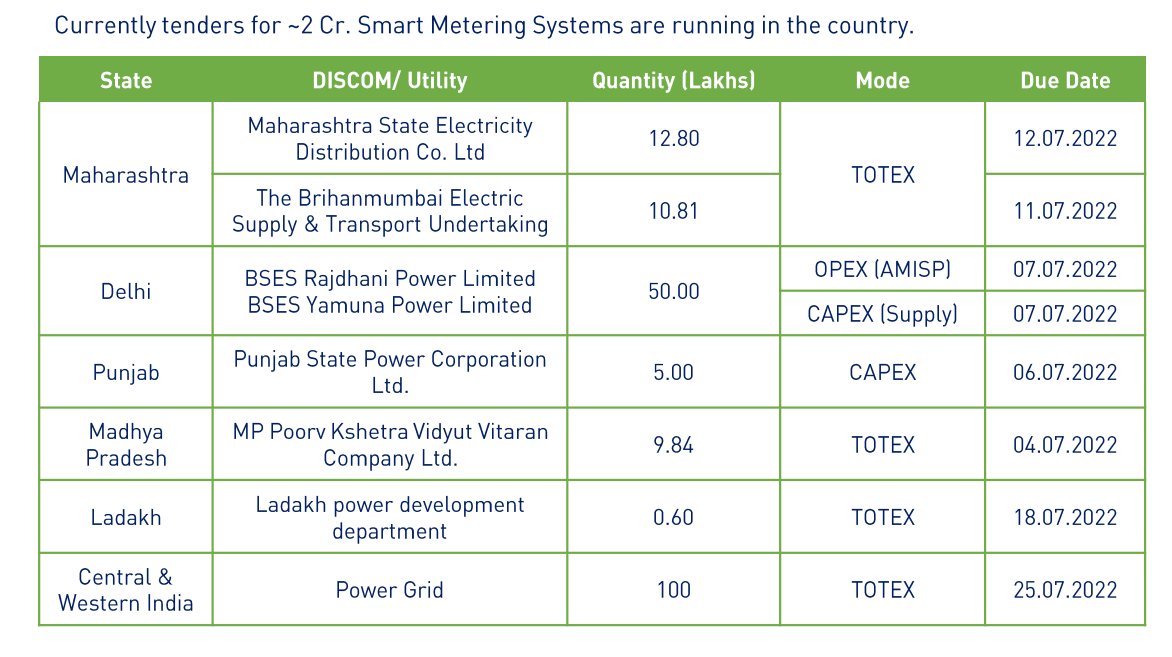

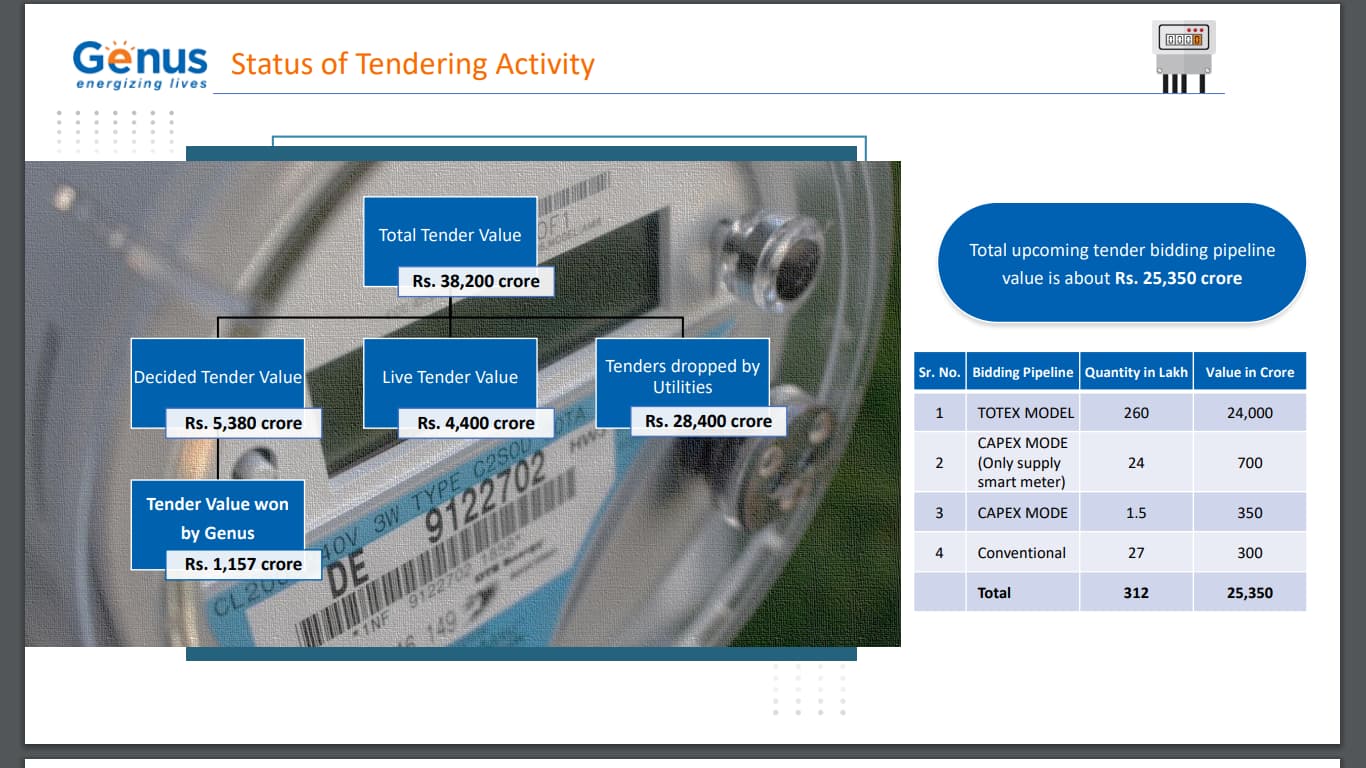

**The tenders are highest ever historically.So if I talk of as on date, , we have almost Rs.

13,000 Crores tender which are in the pipeline out of which almost Rs. 1,800 Crores has

been quoted and Rs. 7,000 crore tenders will be quoted in the next two to three months. And

even the order pipeline if you see the industry wise, like we got some orders from

Jharkhand, from private utilities, we have got some good order booking in last quarter and

this quarter also order booking will have some good numbers. Same way the industry wide

also you will see very good order booking. Otherwise also like EESL, they got an order of

Rs. 600 Crores from Assam. So now they have come out with a tender in the market where

they will buy meters. So order booking has also started from the State Electricity Boards to

system integrators like IntelliSmart. InAndhra Pradesh AP Board have given orders, so

again the tenders will be floated in the market to buy meters. When the order booking from

the SEBs has also started, from system integrators to people like us has also started. And

Genus plays both the roles that of system integrator and also a major supplier also. So we

are getting orders from both the works.

We have been maintaining this in the past also that we have enough capacity to take care of the requirements and enhancement of capacity for a company like Genus

because they are so well vertically integrated - currently we have a capacity of 10 million

meters to 12 million meters annually, and to reach to the level of 16 million to 20 million

meters annually, it is a matter of three to six months. So what I believe is from the next

calendar year onwards, we should be in a position where we are able to do 100% capacity

utilization, and then we can add on to our capacities. So thus we have planned internally

from May, June onwards looking into the way the industry is moving, we will start working

on our capacity expansion if required