50% of order will be executed in next 6 to 8 quarters(meter supply). Only remaining 50% will be collected in next 8 years as part of managing network and maintenance work fees.

1 Like

The payments shall come from customer bill payments on a monthly instalments basis based on better collections

But worry is Adani order cancellation by up electricity board

I hope they r not sub suppliers

And Adani ouster may lower the speed of smart meter growth

2 Likes

Hi Folks, few queries for those who are tracking this co for long:

1/ Does this issue of management being overly bullish in guidance and not able to meet it quarter after quarter is a temporary issue because of supply chain interruptions or there is some structural flaws in the company operations?

2/ They keep on mentioning that due to supply chain issues their capacity utilisation is low. Does it mean that they already have demand and not able to fulfil it because of capacity issues? If this is the case then are they losing customers/market share? Or the case is that the current demand scenario is not that good in short term?

Thanks very much

1 Like

Hi Mukul,

What I think is existing orders in their hand were based on old raw material prices. So margin got decreased due to higher raw material and semi conductor prices.

On the other hand, many tenders were cancelled to upgrade from 2G to 4G network. This reduced/delayed their order book. They do not want to put more resources and complete the existing order and run out of order by paying higher semi conductor and raw material prices. So, the capacity utilization is low at the moment.

Once they get favorable raw material prices and order visibilty, they will ramp up production & complete old orders. Then capacity utilization will improve.

My two cents:

Smart Metering is coming in a big way and that is for sure as I have discussed with my friends who are in State Electricity Department. There are real movements at the ground level and smart metering is bound to happen…

Presence of Adani would have been good, however their absence is in no way going to slowdown the process.

We will have to understand and appreciated how things move in government projects.

This project had been in conceptulisation mode for last many year and now we are at the cusp and the proof is the amount of tenders that are floating in the market. There may still be delay of one or two quarter but one has to be patient while investing in B2G businesses…

Management had not been able to walk the talk mainly because of delay in tender process but since they are in this business for long they should have given calibrated guidance…may be because of the size of opportunity they are not able to control their emotions and guidance ![]()

Disclosure : Invested at current levels and is around 8 % of my portfolio.

6 Likes

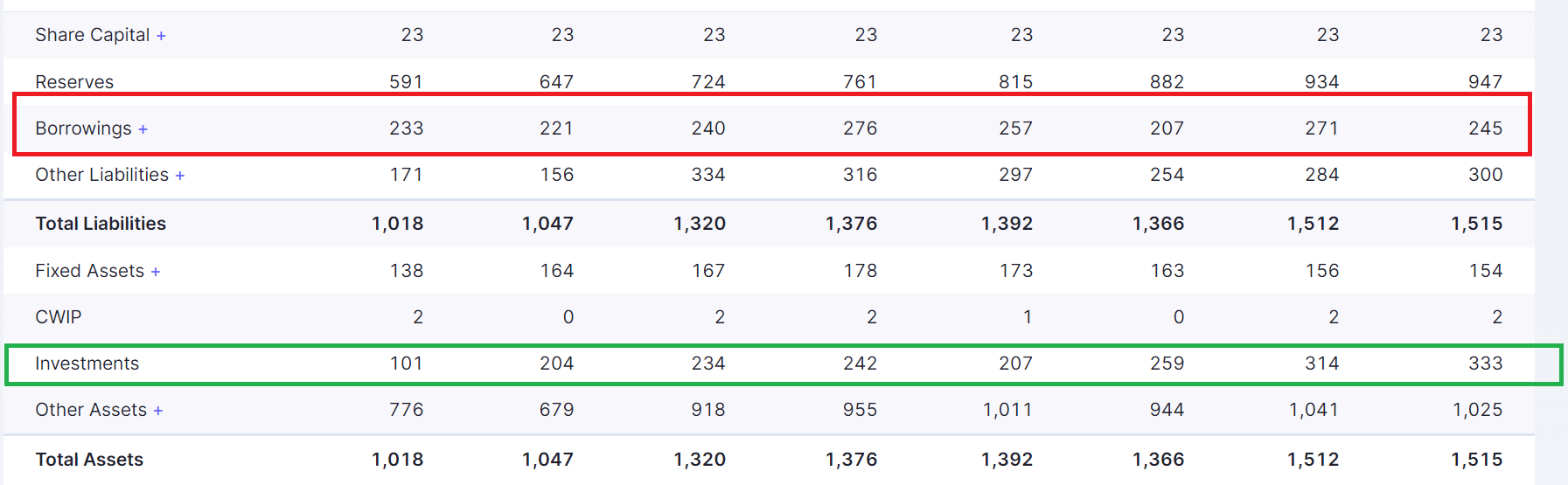

Investments (333 Cr)in balance sheets is more than Borrowings (245 Cr).

They can repay debts instead of investing in others fixed instruments.

Can not we get more profits in There business.

They are paying 25 Cr interest for 245 Crs

1 Like

No company won’t keep money in investments for so many years. its keep on increasing.

If some know exact answer please guide me

Kindly go through page 86-87 and 106 of AR… Investments are made in associate and subsidiaries… 118 cr made in corporate bonds yield higher than interest cost…

Cash credit and suppliers credit of Rs. 21,923.20 Lacs (March 31, 2021: Rs.17,418.54 Lacs) of the Company under consortium arrangement from Bank of Baroda, State Bank of India, IDBI Bank Ltd, Axis Bank, Punjab National Bank, Yes Bank, Export Import Bank of India and Qatar National Bank (Q.P.S.C.), is secured by way of first pari-passu charge on entire current assets of the Company both present and future and collateral security by way of 1st Pari-passu charges on the movable fixed assets of the Company and equitable mortgage of properties on pari-passu basis situated at SPL-3A & SPL-2A, Sitapura, Jaipur (Rajasthan) and Plot No.12, Sector-4 , IIE Haridwar (Uttarakhand) and 2nd charge

on Equitable mortgage of Factory Land & Building situated at Plot No 09 & Plot No 10 situated at Sector -2, IIE, SIDCUL, BHEL, Haridwar and further secured by personal guarantees of Mr. Ishwar Chand Agarwal, Mr. Rajendra Kumar Agarwal and Mr. Jitendra Kumar Agarwal.

Other facilities for Rs. 4,248.15 Lacs (March 31, 2021: Rs. 1,184.23 Lacs) of the Company availed towards financing payables of creditors. The rate of interest is the respective period MCLR and generally in the range between 6.35% to 7.00%.

2 Likes

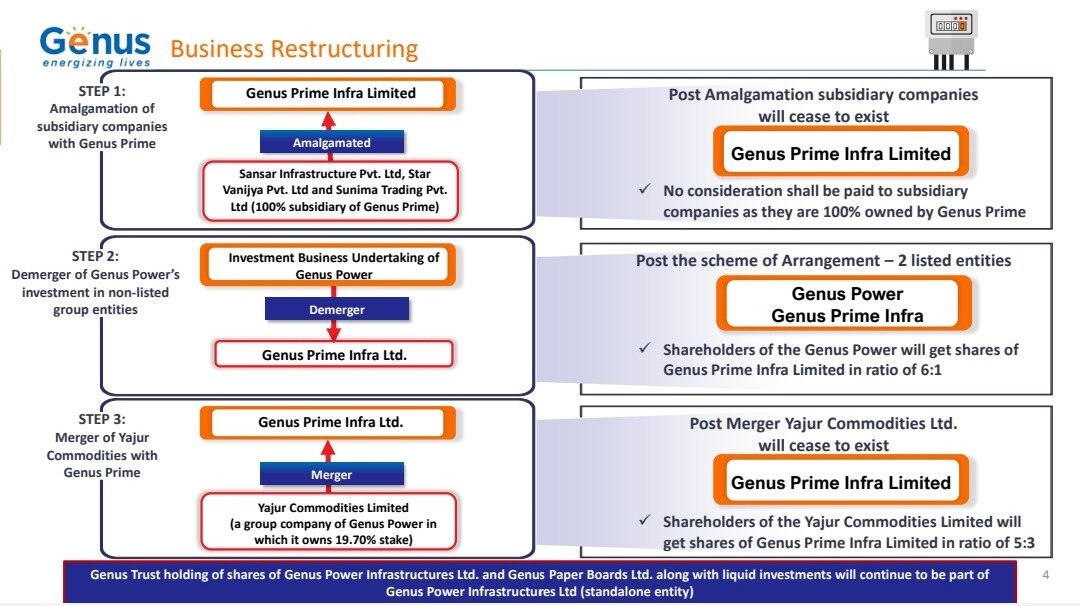

The company plans to hive off the investments section and amalgate it with Genus Prime Infra. The power biz will then not have these investment distractions. It’ll be easier to hold Genus Power post this restructuring. Should be a good move and it’s progressing well.

3 Likes

Thanks Krishna, getting basic doubts (New to investments , please bare with me).

What ever investments we are doing in subsidiaries it will come as a Gross profit of consolidated p/L statement right ?

Associates i am not sure where it will come ?

My understanding is Company MOAT should be to Expand there Core business.

why to put in bonds , Associate companies.

2 Likes

2 Likes

Management is guiding for 1500Cr revenues in FY24 with 15% EBITDA margins. Given their track record of guidance over the last 2-3 years I’d take this with a pinch of salt.

Even assuming they will fulfill their guidance, the nos. translate to around 225Cr EBITDA. Given the company’s dismal track record of generating returns - median ROCE of 12% over 11 years - the most charitable valuation multiple one could assign would be in the range of 10-12x EVEBITDA I suppose. The company is right now trading at 25x EVEBITDA but that’s purely because of the market discounting future growth from AMISP revenues. Net debt of the company is around 200Cr.

Assigning a 12x multiple to 225Cr EBITDA and adjusting the net debt gives an MCap of 2500Cr for the metering business. In addition they have about 300Cr of investments assets mostly invested into corporate bonds and public and private equities. Let’s value them at 1x BV. Put together, the projected MCap would be 2800Cr, about 25% up from today’s MCap.

Since Sep 2022, the company has won about 3700Cr of AMISP orders - Bihar and Assam. To the best of my knowledge, 60% of the order value involves the meter cost and 40% is service which is to be provided over 8 years. Now the tricky thing is, the meter cost (~60% of project cost) needs to be funded by Genus because the State Electricity Boards will make EMI payments each month during and after installation. Assuming Genus makes a 20% margin on these meter supplies, that means Genus needs to fund about 1800Cr (60% of 3600Cr is meter value, 80% of that figure is Genus’s funding need considering 20% sales margin). This funding can be spread out over 30 months, so average annual funding needed would be 720Cr. The average CFO generated by Genus over the last 5 years has been 80Cr at a ghastly CFO/EBITDA ratio of < 20%. Even if cash flows double under RDSS, the company is still probably looking at 550-600Cr debt per year or 1400Cr debt over 30 months.

That’s going to stress the balance sheet a lot. So, while the order visibility is clear and attractive for Genus, I am not so sure about their ability to execute these orders without stressing the balance sheet significantly.

Disclaimer: Was invested, exited recently. May re-enter again if execution and funding visibility improves.

15 Likes

I completely agree with you . The thesis here seems to be somewhat broken . Plus i cant figure why so many many subsidiaries are being formed.

The only golden period seems to be when the company recieves a good order but the execution has been lagging quarter after quarter . It seems more like a hope trade .

Disc: invested considerably at rs. 42 . Going to make a exit soon

Genus Power Infrastructures wins order worth Rs 2,207.53 cr

Genus Power Infrastructures Limited has received a letter of award (LOA) of Rs.

2,207.53 crore for appointment of Advanced Metering Infrastructure Service Provider (AMISP) including design of AMI system with supply, installation and commissioning of 27.69 Lakhs Smart Prepaid Meters, Feeder Meter, DT Meter level energy accounting and FMS of these 27.69 Lakhs smart meters

In the earnings call transcript, the management had mentioned that as on March 2023, the company has already received Letter of Awards worth about Rs. 2,419 crores net of taxes for installation of about 29.49 lakh smart prepaid meters.

2 Likes

- Gem View Investment Pte Ltd is an affiliate of GIC (Singaporean sovereign wealth fund)

- Genus and Gem View have signed a definitive agreement to set up a Platform for undertaking Advanced Metering Infrastructure Service Provider (“AMISP”) concessions

- GIC will hold 74% (seventy four percent) stake while Genus will hold 26% (twenty

six percent) stake in the Platform - They have committed to an initial pipeline with a capital outlay of (approx.) USD Two billion. Genus would be the exclusive supplier to the Platform for smart meters and associated services

- Chiswick Investment Pte Ltd (an affiliate of GIC) will invest INR Five hundred and nineteen crores by way of a preferential allotment of warrants which shall constitute (if and when GIC elects to exercise such warrants) 15% (fifteen percent) of the issued and paid-up share capital of Genus on a fully diluted/as converted basis

- This explains the earlier intimation by Genus (on 17th June) about the incorporation of a wholly-owned subsidiary in Singapore namely “Gemstar Infra Pte. Ltd.” on June 16, 2023

1 Like

Smart Meter hypothesis seems to be taking off, Large Order to HPL Electric.

Source : https://www.bseindia.com/xml-data/corpfiling/AttachLive/3b183210-3a67-4403-9787-d6b490f9c825.pdf

1 Like

HI

Can you help me better understand how this setting up of Platform benefits shareholders ? will this “Platform” be used to bid for more AMISP tenders ?

And since Genus will be sole supplier to them, won’t they be supplying to the “Platform” at discounted rates ?

Is this an attempt to move the pie from minority shareholders to these private foreign entities ?

Apology in advance if you feel it’s naive or silly question.

5 Likes

I have exited my entire holding. Seems the best is over.

Let me take a shot at explaining what this “platform” means in the smart meter ecosystem

Platform refers to the “Advance Metering Infrastructure Service Provider (AMISP)” or the “AMISP” for Design-Build-Finance-Own-Operate-Transfer (DBFOOT) the Advance Metering Infrastructure (AMI) Project.

AMISP is responsible for financing and implementing the entire project. ( Think of it like a road contractor at the risk of oversimplification)

AMISP is also responsible for the Asset Management and Control (AMC) operations for meter-months of all meters and related infrastructure after the Operational Go-Live of the AMI system.

Utility pays AMISP Service Charge on a monthly basis, following the terms and conditions of the AMISP Contract.

At the end of the Contract Period, AMISP transfers ownership of the entire system, including hardware, software, valid licenses, and any collected data during the Project, to Utility for seamless operation of Utility businesses.

The scope of work for AMISP includes end-to-end metering, covering Feeders, Distribution Transformers (DTs), and all end consumers in the selected AMI Project area, enabling complete energy accounting with zero manual intervention.

5 Likes

I think AMISP is like a toll collector, Genus listed will not have much risk of delayed payments due AMISP funded by GIC. Only thing not clear is 26% stake held by Genus whether they fund AMISP and how they are going to raise funds for that

2 Likes