Last Concal Extracts:

Capacity utilization is around 40% to 50% in the current times due to the shortage of raw material and what we feel the way we have done the planning in last two quarters and the

way that things are getting normal every day - by the end of June I would say second quarter of the next financial year capacity utilization will start getting better, will start

reaching the normalized phase from July end. Once the capacity utilization gets normalized

the margins will also get better than previous levels but it will be from Q3 or Q4.

**The tenders are highest ever historically.**So if I talk of as on date, , we have almost Rs.

13,000 Crores tender which are in the pipeline out of which almost Rs. 1,800 Crores has

been quoted and Rs. 7,000 crore tenders will be quoted in the next two to three months. And

even the order pipeline if you see the industry wise, like we got some orders from

Jharkhand, from private utilities, we have got some good order booking in last quarter and

this quarter also order booking will have some good numbers. Same way the industry wide

also you will see very good order booking. Otherwise also like EESL, they got an order of

Rs. 600 Crores from Assam. So now they have come out with a tender in the market where

they will buy meters. So order booking has also started from the State Electricity Boards to

system integrators like IntelliSmart. InAndhra Pradesh AP Board have given orders, so

again the tenders will be floated in the market to buy meters. When the order booking from

the SEBs has also started, from system integrators to people like us has also started. And

Genus plays both the roles that of system integrator and also a major supplier also. So we

are getting orders from both the works.

We have been maintaining this in the past also that we have enough capacity to take care of the requirements and enhancement of capacity for a company like Genus

because they are so well vertically integrated - currently we have a capacity of 10 million

meters to 12 million meters annually, and to reach to the level of 16 million to 20 million

meters annually, it is a matter of three to six months. So what I believe is from the next

calendar year onwards, we should be in a position where we are able to do 100% capacity

utilization, and then we can add on to our capacities. So thus we have planned internally

from May, June onwards looking into the way the industry is moving, we will start working

on our capacity expansion if required

According to the bid, according to our need of the bid we are making the participation. Like

in Andhra we are working with the system integrator - we were very clear that we are not

putting the application. In Assam we quoted directly also and EESL also quoted. And EESL

is using our meters in the bid. So all kinds of strategies are being worked out in the market.Genus has a very flexible approach. We are working with system integrators as their

suppliers and we are also doing some of the projects directly as system integrators.

Mohit Kumar: How is the competition in the system? Has it increased? Is it increasing given the expected

large opportunity - of course it had not materialized as of now but FY2023 could be a very,

very big year for the entire industry?

Jitendra Agarwal: Competition will always be there. It is the important part is how well you are prepared for

the competition and fortunately Genus is sitting in the sweet spot where we are prepared

ourselves and also are very well prepared to take onslaught of any kind of competition.

Vishal Prasad: Thank you. Good afternoon. I have a few questions. I understand we have not won any

orders in capex plus opex model up till now. But Sir could you probably spend two minutes

to explain the modalities of the contract, the capex plus opex, how does it work and how

does the payment works, how are the capabilities of different vendors is taken into

consideration while giving the contract?

Jitendra Agarwal: The capex model is very simple - mostly as a system integrator we have to bid of per meter

per month and this we have to maintain for ten years. 2 to 2.5 years are given for the

installation, and 7.5 to 8 years are given for the maintenance. So total for ten years the

whole project will be under the system integrator, where the system integrator will do the

end-to-end job from installation of meters to maintaining the daily SMS, monthly SMS and

quarterly SMS, everything will be done by the system integrator. SMS means service level

agreement which will be done between the electricity boards and the system integrators and

mostly the system integrator will be paid by per meter per month. So this is how the whole

system will work – not only from the meter reading, billing and in some cases they are

even talking of collection - everything is managed by the system integrator. So the end-toend solution of metering will be taken care by the system integrators, which is EESL is

doing currently… So this is how the whole system is going to work.

Vishal Prasad: Last question if we have to compare our capabilities in software with our competitors so let

us say for example L&T sold it to one of the multinationals - so could you elaborate on

what are the advantages that we have with respect to our multinational competitors and

what are the areas where we are lacking and we will still have to catch up?

Jitendra Agarwal: Currently Genus is the only company which is providing end-to-end solutions. I do not say

that others are not capable of providing that - but they are still little behind us in providing

end-to-end solutions in the current state of affairs and we are probably the only company

which is working in all the communication spheres. So I think technically if you want to

compare with Schneider we are much more vertically integrated in comparison to

Schneider. I do not say that these are not good companies. They are all very good

companies. There is competition, but currently when it comes to smart meters, we have an

edge over them.

Nikhil Jain: Second thing is that in one of the earlier calls you suggested that there are something like 90

to 100 people who are working in the R&D side, who are working in doing the

development work for the smart meter. So if you can just give a little more idea about what

they actually do and what is the value add that is coming in from there? How is it different

from let us say a commodity kind of a product right that’s available off the shelf so based on

the work that the team is doing? So if you can just give some perspective that will be very

helpful? Thank you.

Jitendra Agarwal: Meter being a very custom-built product, it needs a lot of customization according to the

customer requirement. Just to give you a simple example like in doing a smart meter project

in a city like Jaipur, the end customer is concerned about the SLA (service level agreement).

He is not much concerned that how we are going to get to the data. So for him the most

important is to meet the SLA. We are currently working in Jaipur, what we have seen in

Jaipur, is we are using all the technologies, in some places we are using others for

communicating, in some places they are using GPRS. Genus has the capability looking to

the condition of the geography, because we are vertically integrated, we have our own

design. We are not dependent on others for design of the product. We have almost 300

engineers in the R&D (not just 90 to 100) just to give you a perspective - we are very solid

in terms of R&D. And it is not only when we talk about smart meters, it is not only about

hardware, there is a lot of embedded software, which goes into this. It is the only electronic

product in the world which has an electrical application. This is where people have to

understand is that smart meters meters, will never become a commodity and I am confident.

Strong tailwind for the Company and it seems that the Smart meter business is at an inflection point.

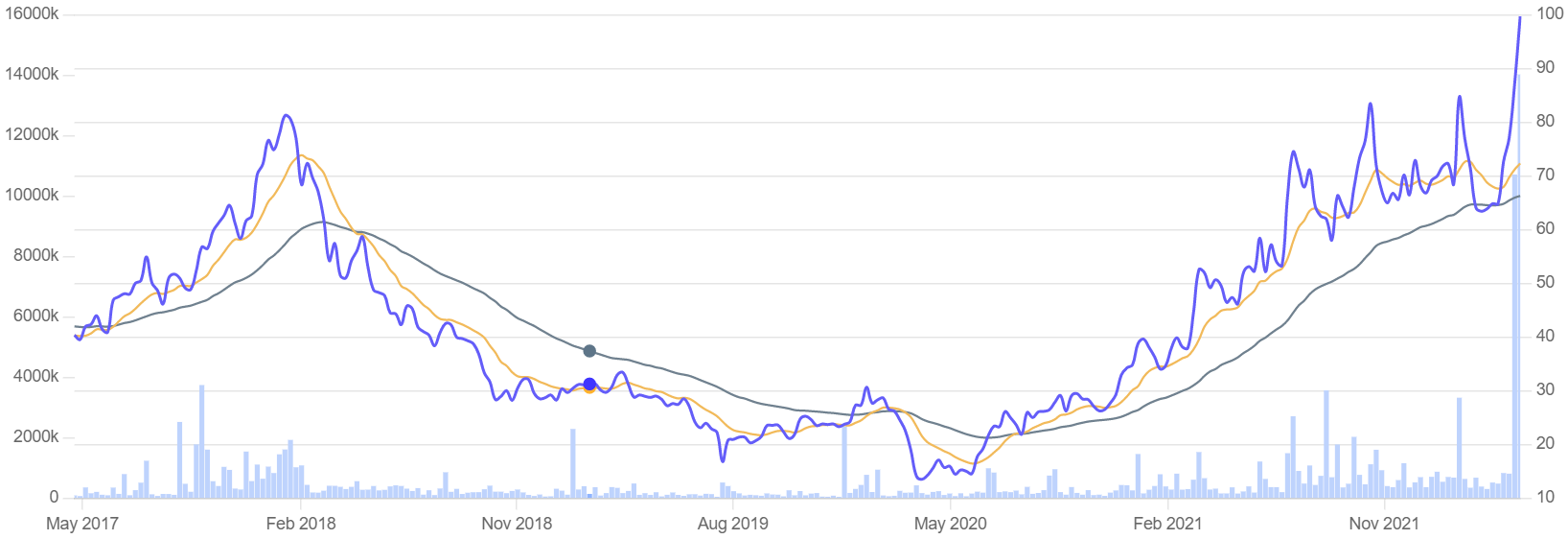

Disclosure : Invested at levels of 90.