I see Genus Power being mentioned in many peoples PF, but there is no dedicated thread on this company. I started looking into this company 2 months back and below is the summary of my findings… I am new to this and request seniors to provide their inputs.

Company Background

Genus Power is a leading player in the domestic electric metering market. It was incorporated in 1992 for manufacturing PCB Assemblies. Production of tamper-proof meters started in 1996 and since then, the company has installed more than 60 million meters.

In the course of 20 years, the company has expanded it’s range of metering products to include Pre-payment meters, smart meters, Smart Street Light Management Systems, Smart Distribution Transformer Meters etc. The company has a 27% market share in the Meter Industry and 70% market share in Smart Meters specifically.

Genus Power has two business verticals

- Smart Metering Solutions

- Contributes 87.5% revenue

- Diversified product mix for Residential, Commercial, Industrial consumers

- Provides Smart Metering Solutions, Prepayment Metering Solutions, Audit Metering Solution and Calibration Equipment.

- Engineering, Constructions and Contracts (ECC)

- Contributes 12.5% revenue

- Offers design-to-end-turnkey power solutions for power T&D sector

- Ongoing/completed projects in Karnataka, UP, Rajasthan, Maharashtra, WB, TN etc.

The company gets it’s revenues only from domestic market.

Financials

Company Financials

| 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | |

|---|---|---|---|---|---|---|---|---|---|---|

| Sales | 653.84 | 714.18 | 705.48 | 652.33 | 765.53 | 915 | 858.14 | 642.38 | 835.05 | 1055.47 |

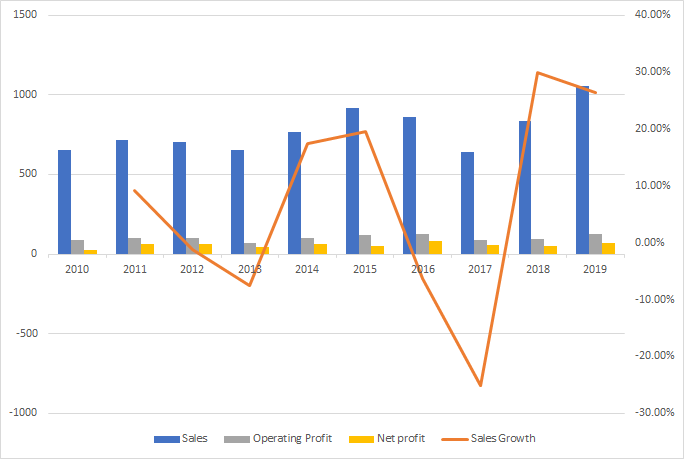

| Sales Growth | 9.23% | -1.22% | -7.53% | 17.35% | 19.53% | -6.21% | -25.14% | 29.99% | 26.40% | |

| Operating Profit | 90.69 | 100.21 | 98.59 | 71.32 | 98.12 | 119.16 | 123.57 | 86.64 | 94.25 | 128.51 |

| Operating Profit Growth | 10.50% | -1.62% | -27.66% | 37.58% | 21.44% | 3.70% | -29.89% | 8.78% | 36.35% | |

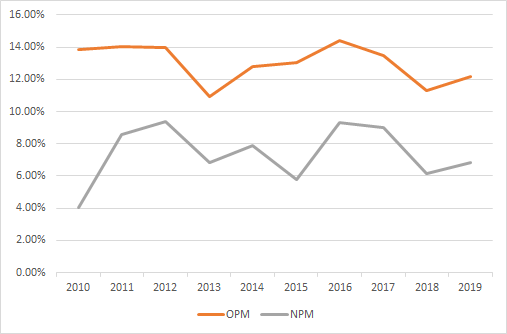

| OPM | 13.87% | 14.03% | 13.97% | 10.93% | 12.82% | 13.02% | 14.40% | 13.49% | 11.29% | 12.18% |

| Profit before tax | 31.04 | 75.57 | 45.41 | 46.84 | 61.3 | 70.8 | 100.55 | 70.37 | 75.09 | 92.54 |

| Tax | 4.65 | 14.49 | -20.69 | 2.27 | 0.82 | 17.67 | 20.46 | 12.46 | 23.55 | 20.17 |

| Net profit | 26.39 | 61.08 | 66.1 | 44.57 | 60.47 | 53.12 | 80.08 | 57.91 | 51.54 | 72.37 |

| NPM | 4.04% | 8.55% | 9.37% | 6.83% | 7.90% | 5.81% | 9.33% | 9.01% | 6.17% | 6.86% |

There are 3 years when the revenue growth was negative

- 2017 - Disagreements between central and state governments on procurement of meters resulted in slower offtake of tenders. Since the issues were resolved towards the end of the year, the order book reflects higher orders.

- 2016 - The revenue drop of -6.21% was due to discontinuation of the power backup solutions business during that year. Post adjustment, the revenue growth was actually +5.77%

- 2012~2013 - Attributed to ow government spending on infrastructure

OPM and NPM has been steady during all this period.

Segment Revenues and Margins

I was not able to find breakup between the two divisions in the annual reports. So revenue, margin breakup is not available

Thoughts

Market position: Genus is fairly well known and large player in a very competitive market. Competitors include companies like L&T, ITI, Keonics, JnJ.

EESL is currently handling the deployment of Smart Meters (About Smart Meters). The contracts are awarded through tendering process. Often larger infra companies like L&T participate. However, the actual supply of meters get further sub-contracted and end up with companies like Genus. Having all the necessary certifications helps Genus.

Examples

- L&T, two other bag Uttar Pradesh power meter deal - Genus quoted the lowest price and won 50% of the 10 million meters order.

- L&T loses government order to supply 2.5m smart meters in reverse bid - Genus was the second lowest bidder behind ITI. (I think they got 30% of the order)

- Companies upset over smart meter tender - ITI won this bid but later subcontracted to 4 companies, one of which is Genus.

The order book has seen healthy growth over the past 4 years

| 2016 | 2017 | 2018 | 2019 |

|---|---|---|---|

| 386 | 685 | 1276 | 1498 |

The process is also prone to corruption and consequently bad press

Examples where Genus has been quoted

- Electricity meter procurement scam: Probe is underway

- Discoms’ meters defective, oil quality inferior: CAG

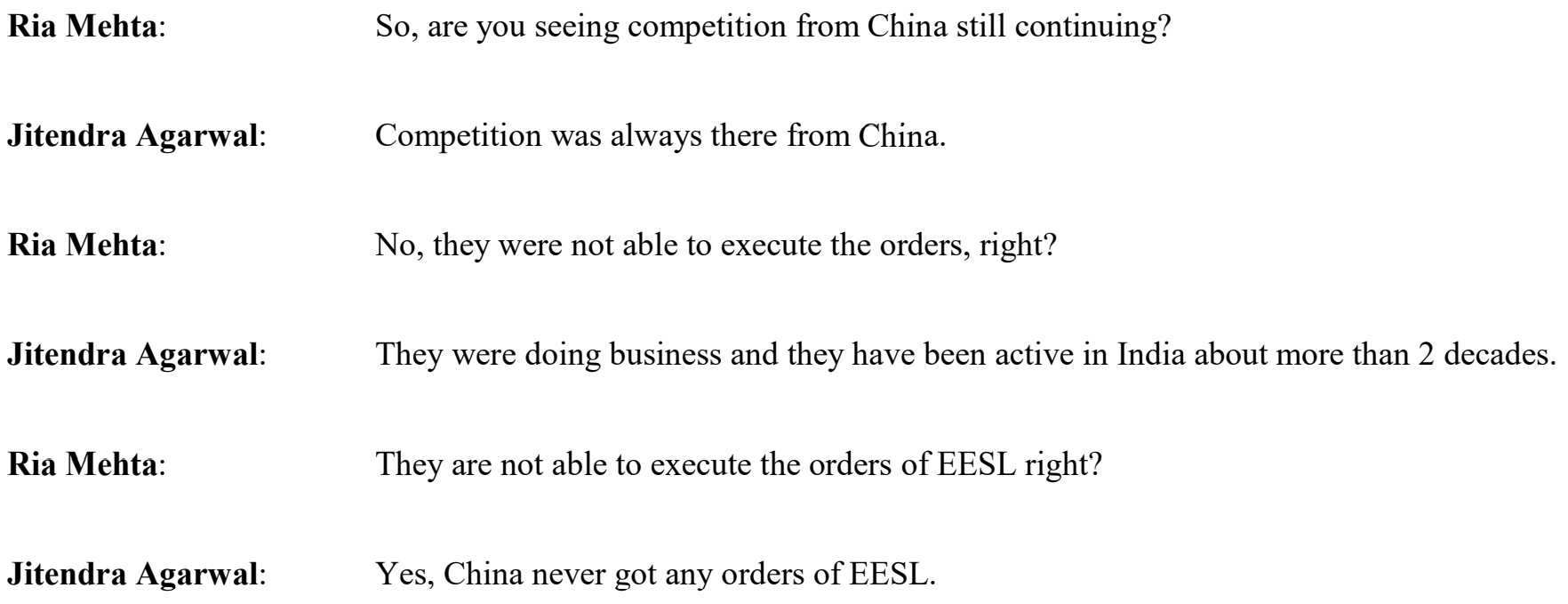

Imports, especially Chinese imports, are a constant threat as mentioned by Jitendra Agarwal of Genus Power in this interview - “Chinese imports have led to closure of many businesses”. However, in the last earnings call, he clarifies that no Chinese company has bagged a EESL tender

However, this seems to be a constant threat.

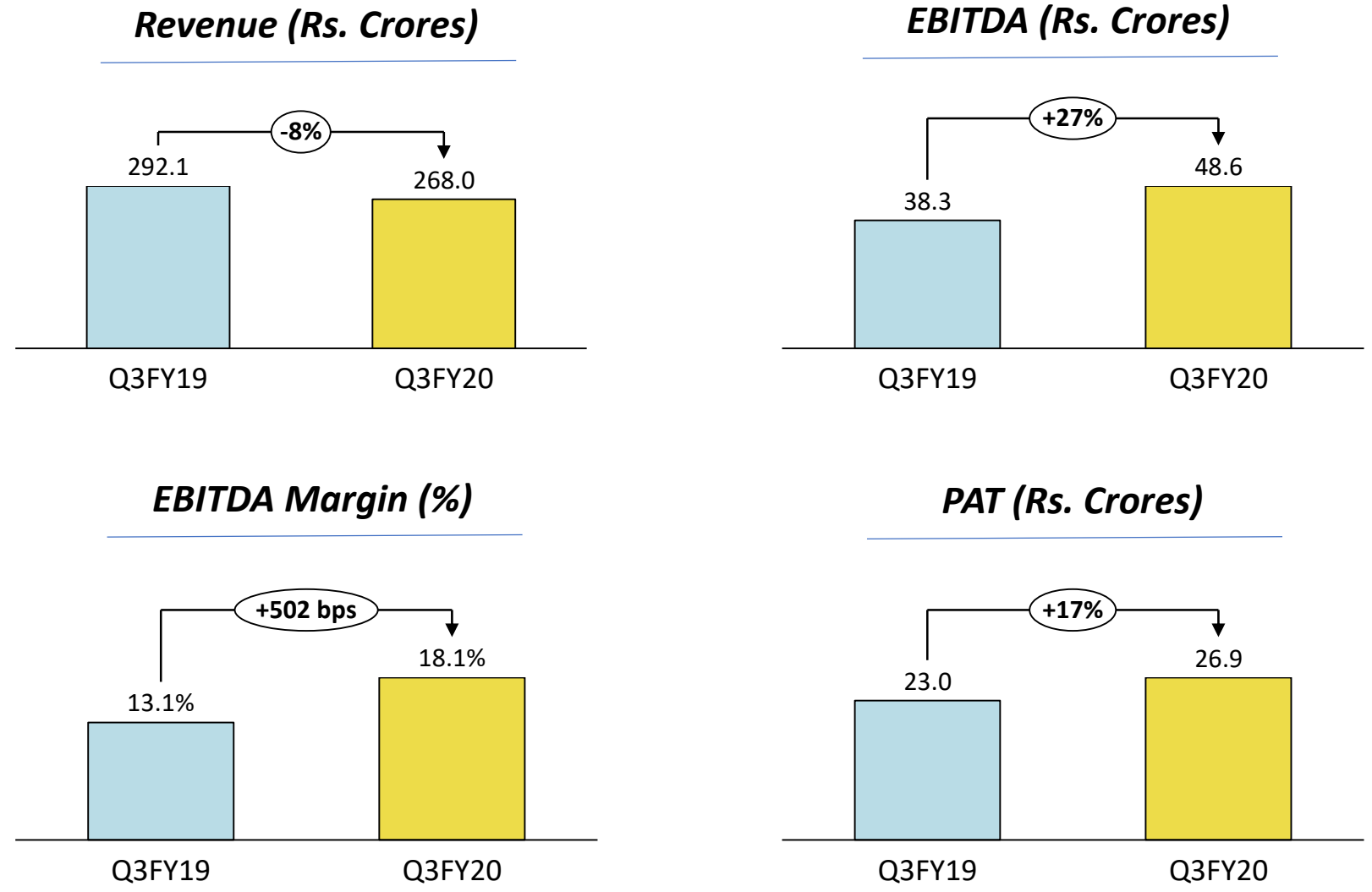

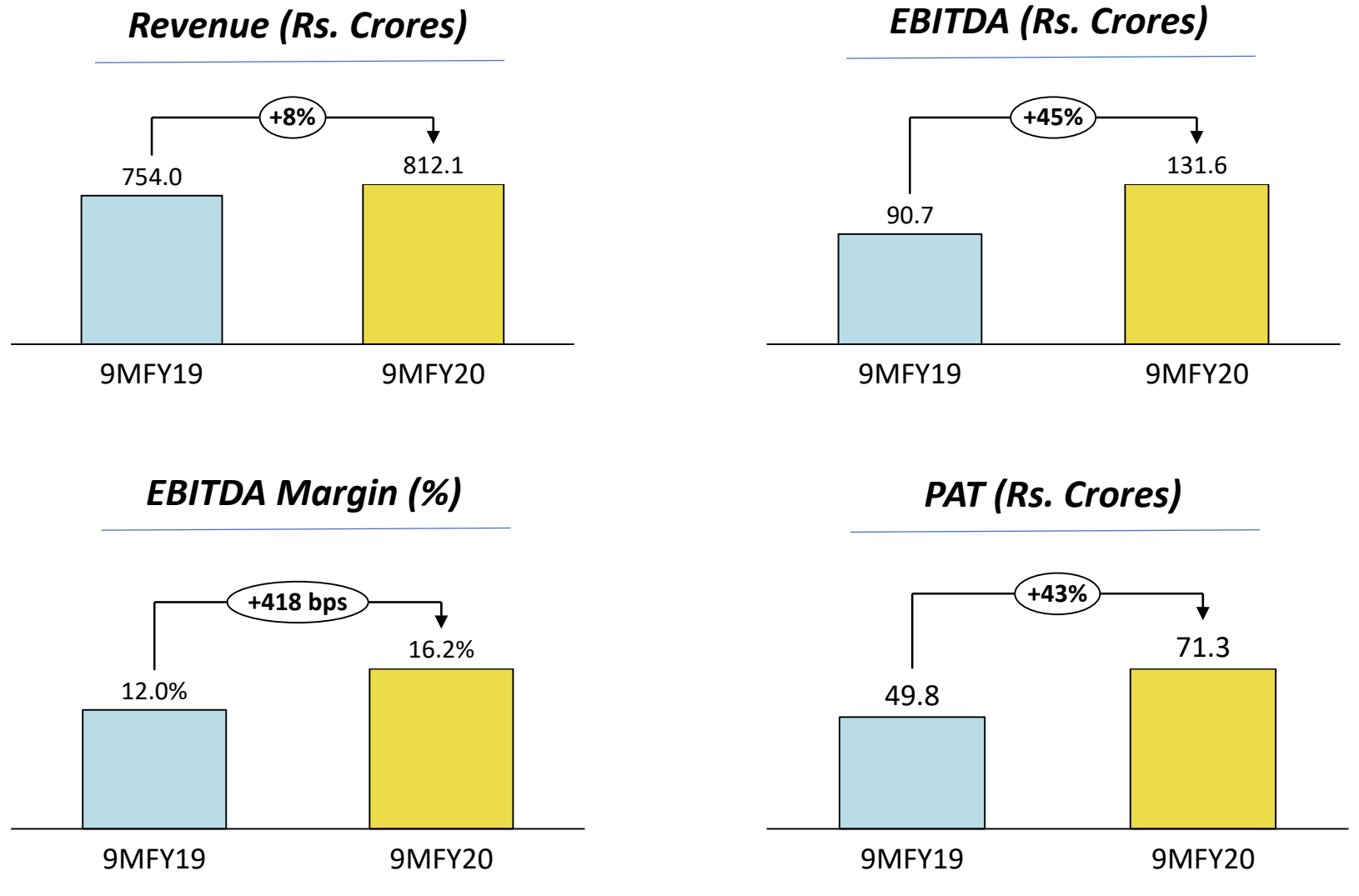

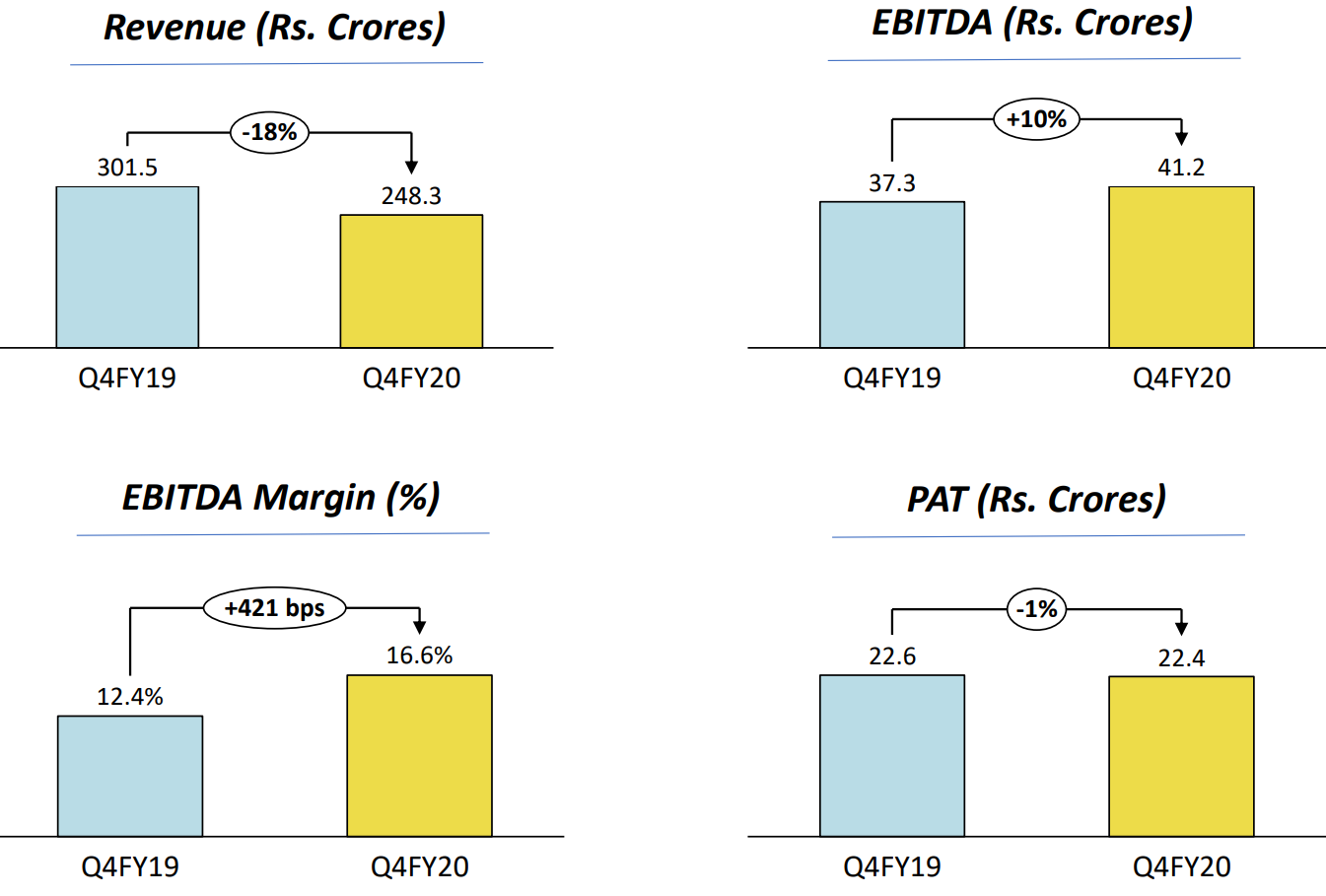

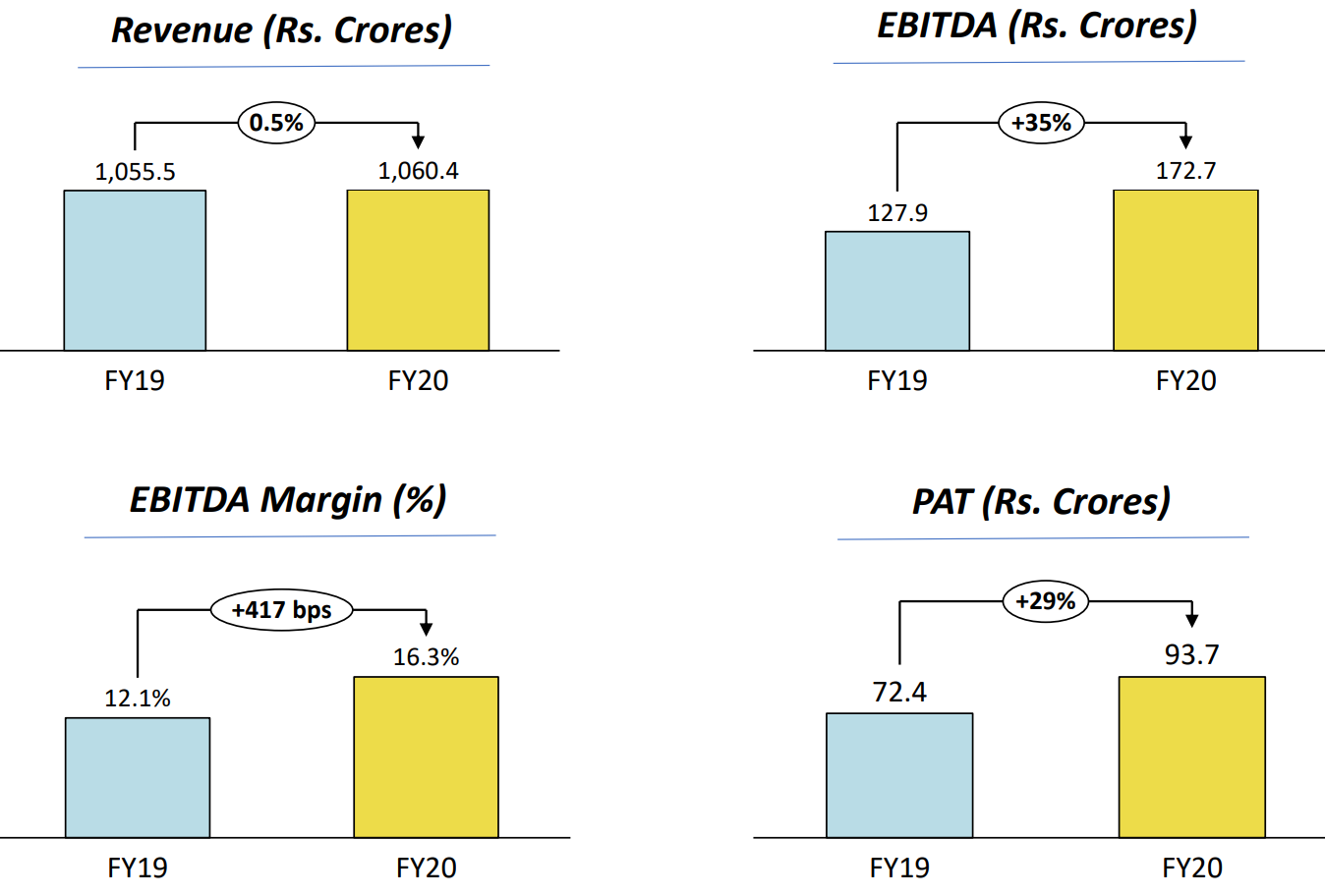

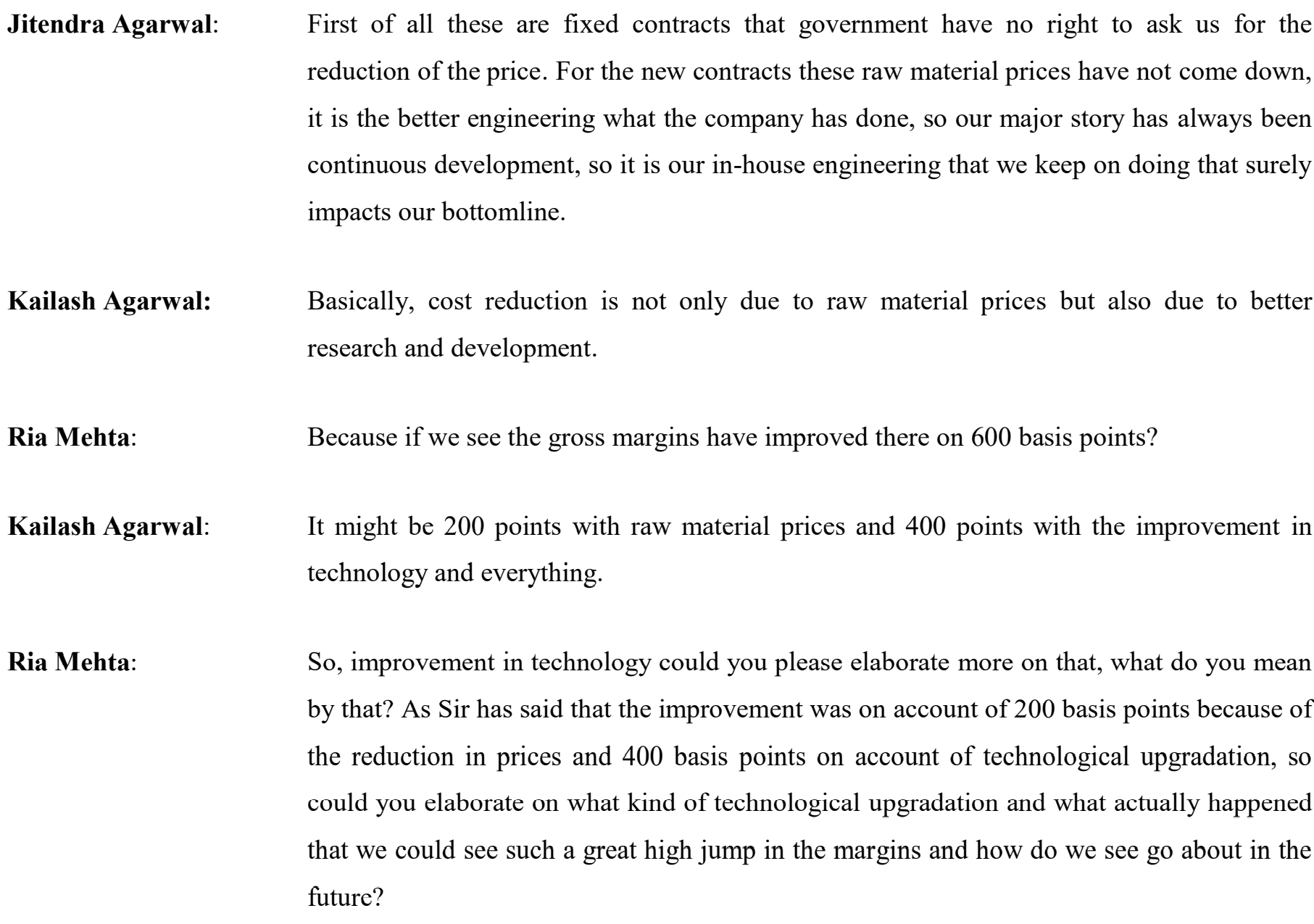

Margins and Pricing: Being fixed price contracts, pricing is important during the bidding process. Raw material availability and cost form a big portion of the costs. The OPM and NPM has been steady (as shown above) at 12% and 6% respectively. The last two quarters has seen a sudden jump in these two to 15% and 8.5%. The conference call has some pointers on this improvement

Receivables: The receivable days is high for obvious reasons. It’s consistently around 6 months. CCC too is similarly high

| 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 |

|---|---|---|---|---|---|---|---|---|---|

| 197.56 | 190.32 | 206.75 | 217.05 | 164.15 | 146.94 | 170.95 | 208.32 | 182.99 | 186.99 |

| 159.48 | 155.40 | 180.53 | 198.79 | 154.34 | 144.98 | 167.46 | 201.19 | 165.10 | 158.01 |

Debt Levels: Debt to Equity has been reducing consistently over the years

| 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 |

|---|---|---|---|---|---|---|---|---|---|

| 0.84 | 0.82 | 0.73 | 0.58 | 0.72 | 0.74 | 0.36 | 0.31 | 0.32 | 0.34 |

Related Party Transactions: The company had a Joint Venture in Brazil Genus SA, Brazil. This was divested in FY 2016. There was another subsidiary Genus Paper and Boards which was transferred to Genus Shareholders Trust. However there two associate companies and a few companies where Key Management Personnel are in position of influence. The concerning issue is that Genus Power has extended unsecured loans and guarantees to these unlisted companies. There are also transactions with these companies and KMP

Calling out some of the items from the AR (all values in lakhs)

| 2016 | 2017 | 2018 | 2019 | |

|---|---|---|---|---|

| MKJ Manufacturing - Loan Balance | 373 | 44 | 133 | 96 |

| Greentech Mega Food Park - Investments | 132 | 215 | 304 | 174 |

| Yajur Commodities - Balance Receivables | 2284 | 2490 | 2753 | 0 |

| Yajur Commodities - Guarantee Given | 16388 | 12205 | 7868 | 6855 |

| Genus Consortium - Advances | 9.85 | 10.4 | 1.7 | 3.4 |

| Genus Innovation - Balance Receivables | 1384 | 3525 | 3302 | 3591 |

Pledge

Another concern is that the promoters have pledged shares starting Dec 2017. The pledge is creeping up steadily

| Dec 17 | Mar 18 | Jun 18 | Sep 18 | Dec 18 | Mar 19 | Jun 19 | Sep 19 |

|---|---|---|---|---|---|---|---|

| 3.08% | 3.31% | 4.43% | 4.43% | 5.27% | 5.27% | 5.27% | 6.51% |

Valuations

Historical valuation

| 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | |

|---|---|---|---|---|---|---|---|---|---|---|

| Price | 15.3 | 16.93 | 9.91 | 10.41 | 11 | 24.35 | 52.8 | 40.5 | 51 | 28.8 |

| EPS | 1.78 | 4.02 | 4.16 | 2.80 | 2.36 | 2.07 | 3.12 | 2.25 | 2.00 | 2.81 |

| Price to earning | 8.58 | 4.21 | 2.38 | 3.71 | 4.67 | 11.77 | 16.93 | 17.99 | 25.45 | 10.24 |

| Book Value | 19.86 | 24.15 | 28.04 | 30.71 | 16.90 | 18.98 | 25.51 | 27.38 | 29.09 | 31.48 |

Current valuation

Price: 23

P:E: 6.59

P:BV: 0.71

Thoughts

There is no doubt that the Smart Meter market is going to grow at a decent clip in the coming years. Department of Science and Technology’s report on Smart Grids clearly details the future direction. The section on Smart Metering mentions a CAGR of 8~10% in the next 4~5 years.

There is intense competition but Genus seems to be well placed to ride the Smart Meter wave over the next three years. It has the required R&D infra to handle the technological shifts. The management is confident of maintaining margins going forward. Looking at history, Genus seems to have managed the Receivables and CCC well.

The related party transactions and pledged shares is one of the major concerns. The market seems to have factored this into the 5-year low PE of 6.59. With two good quarters and improving margins, if the company can build on the momentum, we should see some improvement in market valuation.

Refer:

Disc: Started tracking a couple of months back. Invested less than 5% of PF as a tracking amount.