Detailed Analysis of Geekay Wires Ltd Market Cap: 316 Cr. 5-year Sales CAGR: 26% 5-year Profit CAGR: 100% ROE: 42% ROCE: 27% PE: 10x

Let’s deep dive into it![![]() ]

]

Business Overview:

-Geekay Wires Limited is an ISO 9001:2008 certified company, located in Hyderabad

-The Company was taken over by the Kandoi Family in 2012

-Geekay Wires has been in the biz of manufacturing high-quality galvanized steel wires & other different wire products

Geekay manufacturers niche quality of

- Galvanized Steel Wires

- Collated Nails

- Bulk Nails

- Stainless Steel Fasteners

- HTGS Earth Wire

- Stay Wire

- Binding Wire

- Cable Armour Wire

- Spring Steel Wire & other types of wires

Catering to vast Industries like:

-Industrial, Power Transmission,

-Cable and conductor,

-Commercial Construction,

-Automotive industries,

-Marine & mine Industries,

-Wind & solar Power Energy &

-agriculture applications

In short, the Proxy to Capex cycle & an FMEG Player

Production Process of Wires:

-Main RM is Wire Rod (High Carbon steel)

-Zinc is used for galvanizing the steel wire

-Acid Pickling removes impurities

-Wire drawing provides shape & density

-Galvanizing to make it rust-proof

-Stranding to make the product perfect

-Final testing

Production Process of Nails:

-Drawn Steel Wire Rod main RM

-Nail-making machines give shape as per requirement

-Nail polishing unit gives finishing to the nail

-Then, Plastic or Wire Nails and Thread Rolled Nails can be made from that polished nail

Raw materials used:

-For steel wires & nails it’s wire rod

-For GI steel wire it’s Wire rod + Zinc

RM is procured from both international & domestic markets

Also, entered into an agreement with Hindustan Zinc Limited & Rashtriya Ispat Nigam Limited for the supply of raw material

Manufacturing units:

Unit 1 at Isnapur Village, Medak District, Telangana

Unit 2 at Shankarampet Village, Medak, Telangana

Geekay has an installed capacity of 30,000 MTS PA of GI Steel Wires in various grades & sizes and 30,000 MTS PA of Nails & 10,000 MTS PA of SS Nuts & Bolts

Cliente Profile:

Preferred vendors of PGCIL(Power Grid Corporation of India Ltd) in most of the State Transmission & Distributions companies across India. Geekay also exports products to various countries including USA, Canada, UK, Australia, Saudi Arabia & Germany

Industry Growth/Driver:

-India’s domestic steel demand is estimated to grow annually by 5-7% in Next 3-4 years

-The construction industry in India is expected to expand by 5% in real terms in 2023

-In the Budget 2023-24 the PM & FM have announced Rs. 10 lakh crore capex plan

Key Competitive Advantage of Geekay Wires:

- ISO Certified Products & Quality products

- Qualified & Experienced team

- Preferred clients of many government & private sector + Recognised & established Client base

- Wide SKUs/Product range

- Order Book Fully Booked

Key Variant Perception playing out:

- Industry Cycle: Capex Phase going in India

- Deleveraging: Debt is reducing

- Capex led growth: Doubled the Capacity of Nails

- Operating Leverage: Scale will increase Profits more than Sales (Currently going on)

- Margin Expansion: Introduction of Quality & Premium Products

- Cost Reduction: Can play in future, if Geekay introduces automation in manufacturing

Sources of Future Earnings:

- Geographical Expansion: Entering new states in India & Expanding further in Export market

- Increasing Distribution Network

- Increase in Manufacturing Capacity

- Introduction of more VAP Products

- Capex cycle in India & PLI Schemes

- Increase in foreign demand

- Fully booked orders

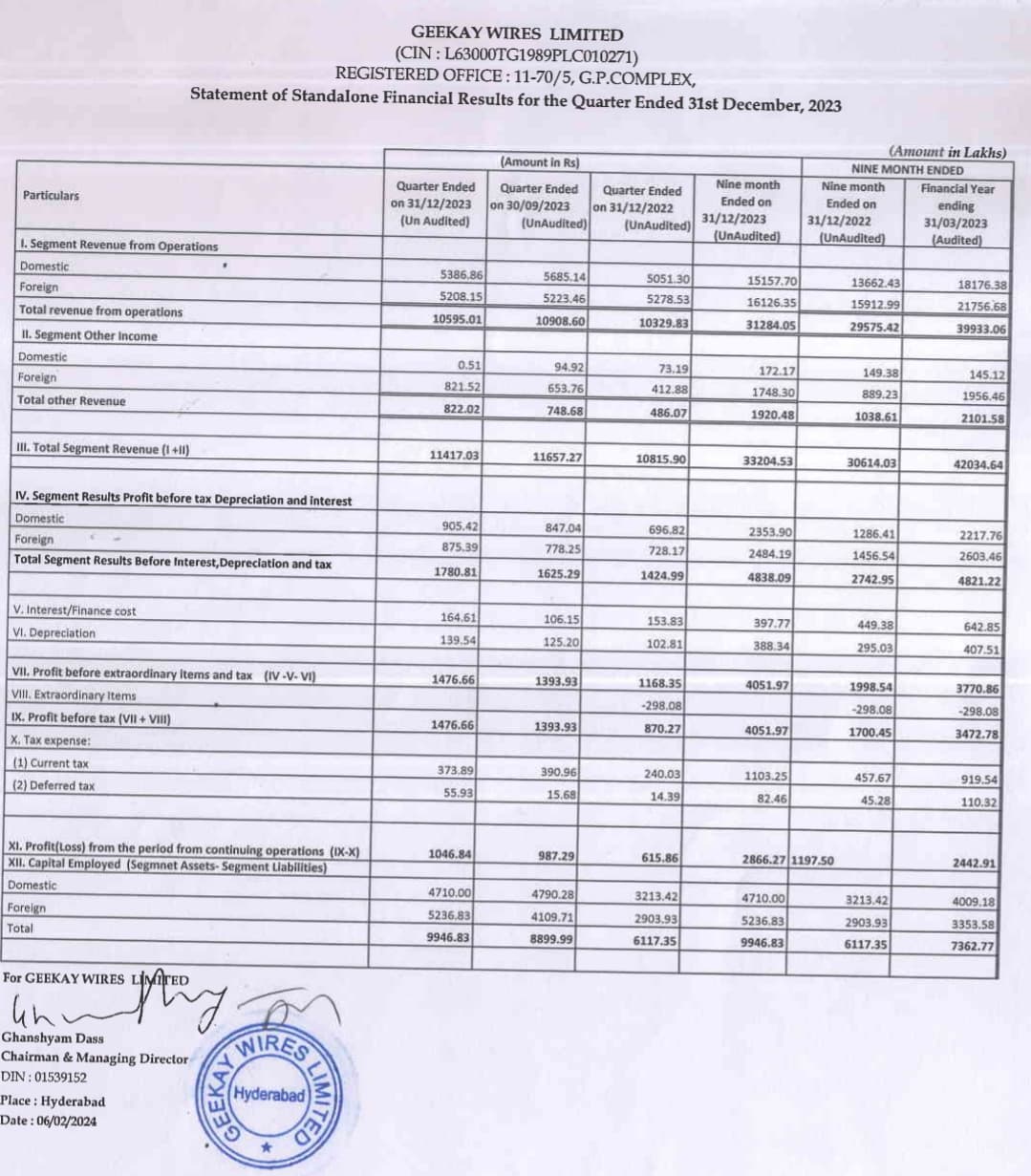

Financial Analysis:

Will Put it Crisp, One can check the screener for a detailed one

-GP Margin has expanded to 21% from 16%

-PAT Margin has expanded from 3% to 6%

Mainly margin is expanded through improvement in GP Margin & Operating Leverage

-Employee intensive production

Segment Analysis:

-Sales growth of Export Vertical is more than Domestic Vertical in last 3 years

-Last FY Director remuneration increased by 91%, but still in a limit when compared to % of PAT

Ratio Analysis:

-D/E reduced from 2 to 1.3 times

-Interest Coverage improves from 2 to 6 times

-ROE expanded to more than 30% led by PAT margin & Operating Leverage

-Asset turnover also improved & now around 2 times

Efficiency Analysis:

-Receivables turnover ratio improves

-Inventory Turnover improves

-WC Days reduces

-Good CFO conversion in FY23

Valuations:

-P/E around 10 times, median PE is 10.6 times

-EV/EBITDA around 6.6 times, median is 7.4 times

-Industry PE is around 20 times

-Available at a discount to median & Industry level valuations with good sales growth, WC improving & good CFO conversion

Peer Comparison:

It’s closest competitor is DP Wires and other competitors in some products are Usha Martin & Bharat Wire Ropes

DP Wires:

-Sales growth is more than Geekay in 5 years (42%) but Profit has been lower (just 33%)

-GP Margin reduce drastically

-ROCE & ROE constant & above 20%

-WC cycle improved & Asset turnover led ROE Growth

-Available at 21x double the valuation of Geekay

Why does Geekay trade at the lower multiple?

Reason

-Continues inclusion in AGM & ESM List (Caps liquidity & trading)

-High Debt can also be the reason

-Might be still market is accession the stability of operations (Margins & Growth)

Anti-thesis:

- Labour intensive Industry

- High Logistics cost (Need to be pan India to have good growth, but Geekay is mainly in South)

- High Inflation impacting input cost (Steel)

- Competitive Industry with highest share of unorganised/Local players

- High Debt (D/E of more than 1)

- WC intensive operations

- High Volume & Low margin type Biz

- Depend upon Government (Can have B2G risk) & CFO conversion risk

Hope you will like it!!

Strictly, No Recommendation

Open for discussion!!

Note: Can’t able to post images because of new member restriction. one can check proper one on twitter

Also, more active on Twitter… if anyone want to connect

https://twitter.com/BansalSwapan