Company has assets that is Tanks for storing liquid at Nagpur and Daund as per my info it also has something at Pune. Customer concentration is high as only two customer were there but now in discussion or may have added new customer.

Thanks buddy !! It is interesting to see the development of the subsidiaries. Also, it gives great confidence if management come out with details about the expected expenditure and by when they would start contributing to the revenue. Let’s track it closely.

@RajeevJ and @Pranshinv Please put some insights regarding current situation in Logistic and Terminaling biz… as the cost of Export and import are skyrocketing due to container shortage. My view is Chemical Segment may surprise us like it did last year when import were not happening due to COVID and it clocked highest profit and gave us some hope of trunaround. Also higher cost of Container shipping may have spilled to Rent to port based storage players.

Please share ur views thanks in advance

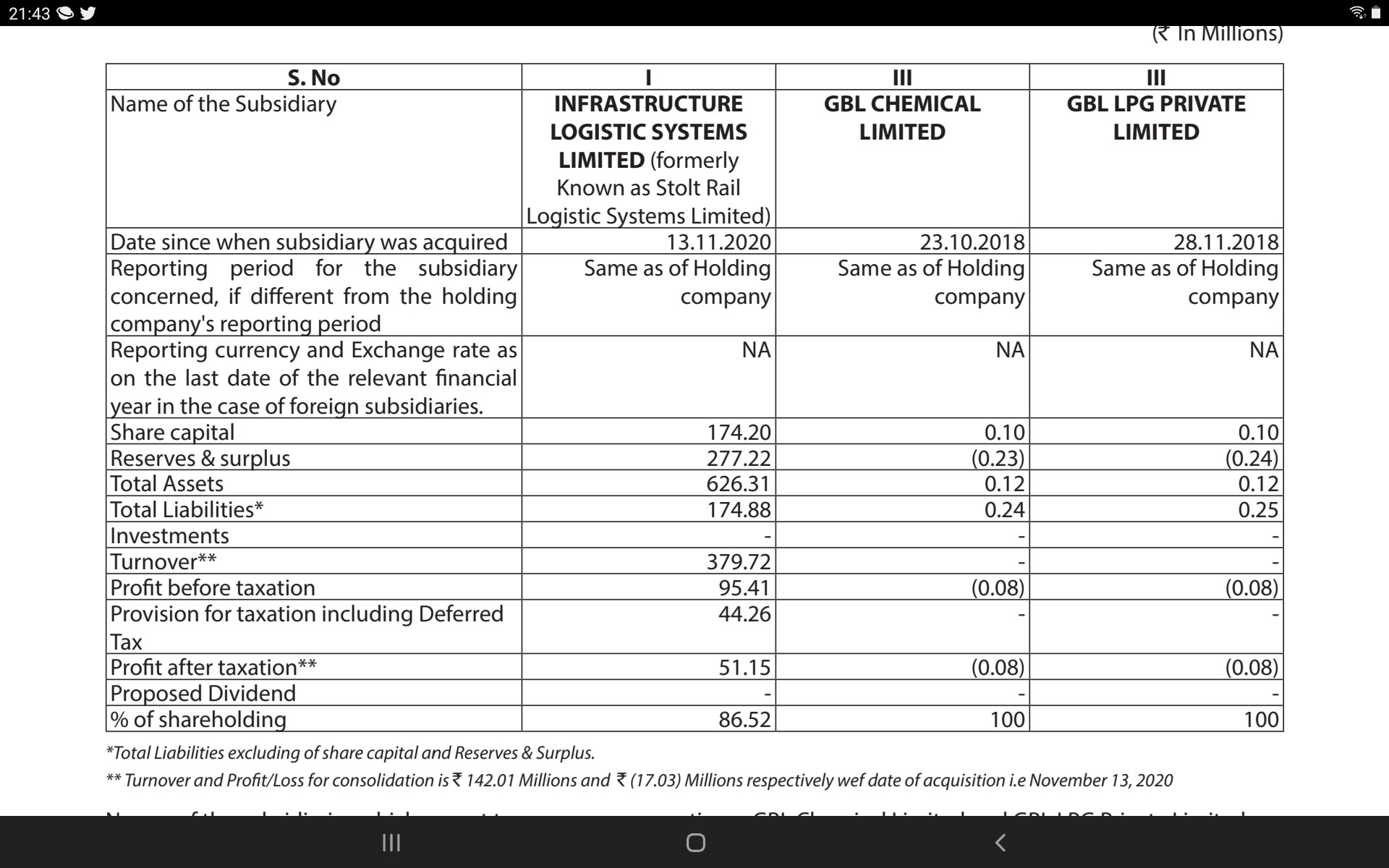

Management has transferred major Chemical business operations to WOS GBL Chemical Limited.

(It seems to be an Indirect demerger of business)

Considered and recommended for approval of the shareholders at the ensuing 34th Annual General Meeting (aCM) conducting the chemical business between the parent company - Ganesh Benzoplast Limited and its 100% subsidiary (Wholly Owned Subsidiary) GBL Chemical Limited, without transferring any immovable property owned by the company.

Under this arrangement, the purchase of raw material necessary for the manufacfure of the chemicals and the sale of finished chemical products will be handled by the WOS namely GBL Chemical Limited and the parent company (Gariesh Benzoplast Limited) will continue to carry on the manufacturing of chemicals on job work, exclusively for the WOS (GBLChemical Limited). BR.pdf (2.0 MB)

The mgt. intention behind transferring the Chemical business to the subsidiary is to bring clarity to the investors about the value of the stand alone logistics business. The Chemical business seems to be rather volatile in terms of its numbers. The division is impacted by a number of factors, some beyond the control of the mgt. Going forward, the stand alone numbers will be bereft of the chemicals division. This seems like a prelude to the eventual de-merger of the Chemical business.

Similarly, it is with the same intent that the Steel fabrication business will hence forth be carried out in a different subsidiary. This business is again lumpy in nature and was currently being clubbed with the logistics division. The overall margins of the fabrication business were much lower than the logistics business & depending on its volumes impacted the operating margins of the logistics division making quarterly comparison difficult. Also, as the fabrication business gains traction, it makes sense to hive it off into a separate division to enable it to grow that much faster.

Hope the Co. gets its due recognition on the bourses!

The Board of Directors of Ganesh Benzoplast Ltd, at their meeting held on September 01, 2021, has discussed the business operations and prospects of GBL Clean energy Private Limited, a newly incorporated 100% subsidiary which will deal in clean energy fuels viz. ethanol, ethyl alcohol, bioethanol, butanol, bio-alcohol, methanol and Isopropyl alcohol and other clean energy and biodiesel fuels, bio-oils and other agro-based products etc. Using ethanol and other alternative bio-fuels is highly promoted by the Government these days and various initiatives are taken by the Government for using environmentally friendly sources of fuel and by this industry, has a huge demand which can be capitalized by the company with the existing experience of the its parent company.

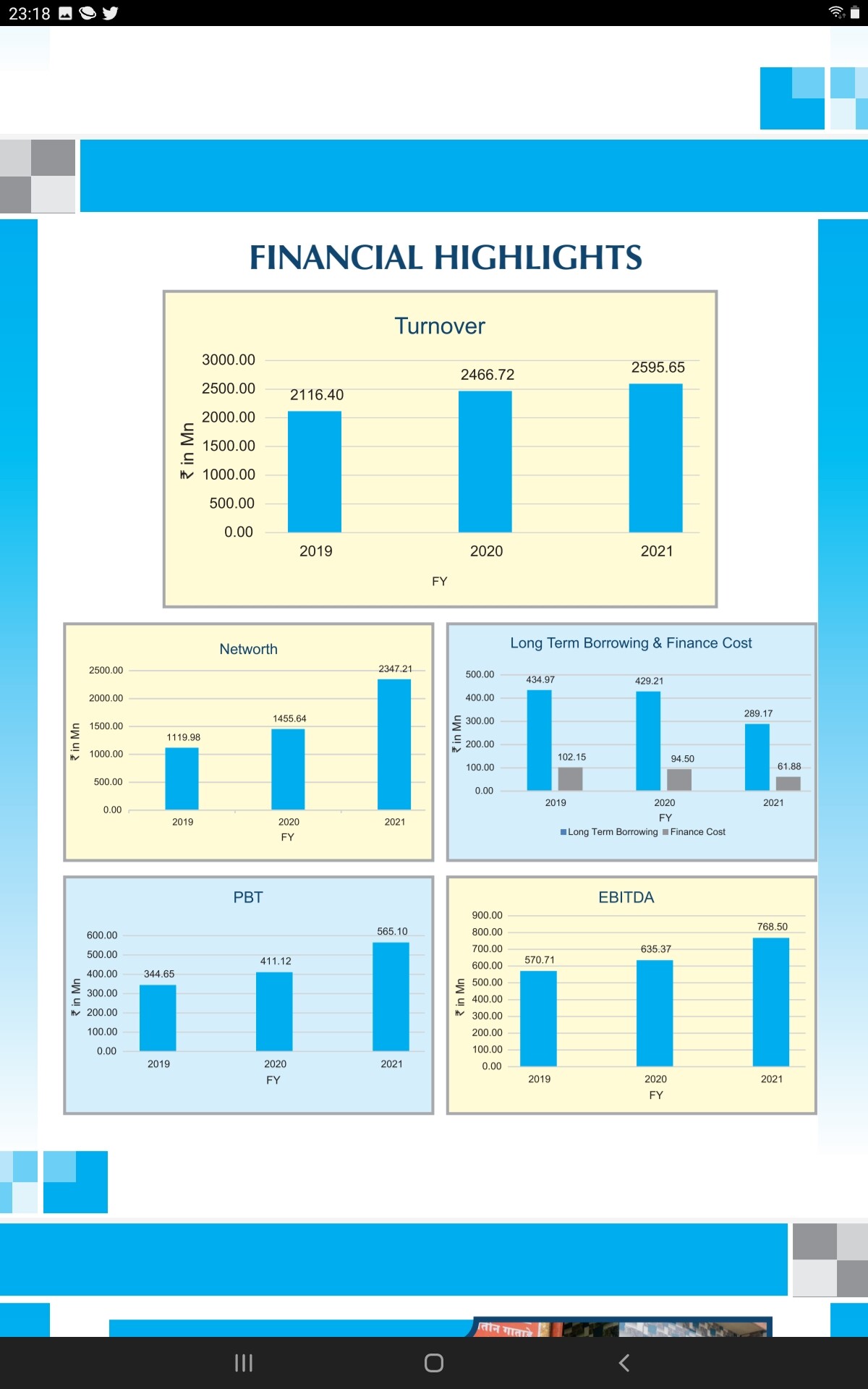

Stolt acquisition performance- 38 cr rev 10 cr PBIT, 5 Cr PAT - reported in consol 17 cr rev and 2cr losses in FY 21. For FY 22 this business is likely to straighaway add 8-10Cr in profits. BIG DEAL over current reported PAT in FY21

Deferred tax impact in FY 21 numbers , PBIT 51 cr and PAT 24 cr - PAT in normal scenario could have been 40 cr without Stolt

Normalized FY 22 they can do 350 to 400 cr top line and 45 - 55 cr PAT

( LST around 250+ - includes LST+ Stolt+ new EPC biz, rest from Chemicals), Profit for LST is higher at 40-45% PBIT, Chem is volatile but can deliver 15% type annual. Valuations

Available at 1-1.5X Sales, sub 10 PE for FY22.

Reduced debt , D/E 0.2, has good cash balance

Negative

Volatile in margins at consolidated levels

Overhang of Morgan case and pending demerger

Divisional performance Divergence - LST vs Chemicals

EPC biz - saturation in LST due to capacity constraints? Could be wrong interpretation

Hardly any returns in roaring bull market in last 1yr - range bound

Disc - was invested from Q2 21, exited in Q1 22 due to opportunity cost , have tracking position, v interesting biz on demerger

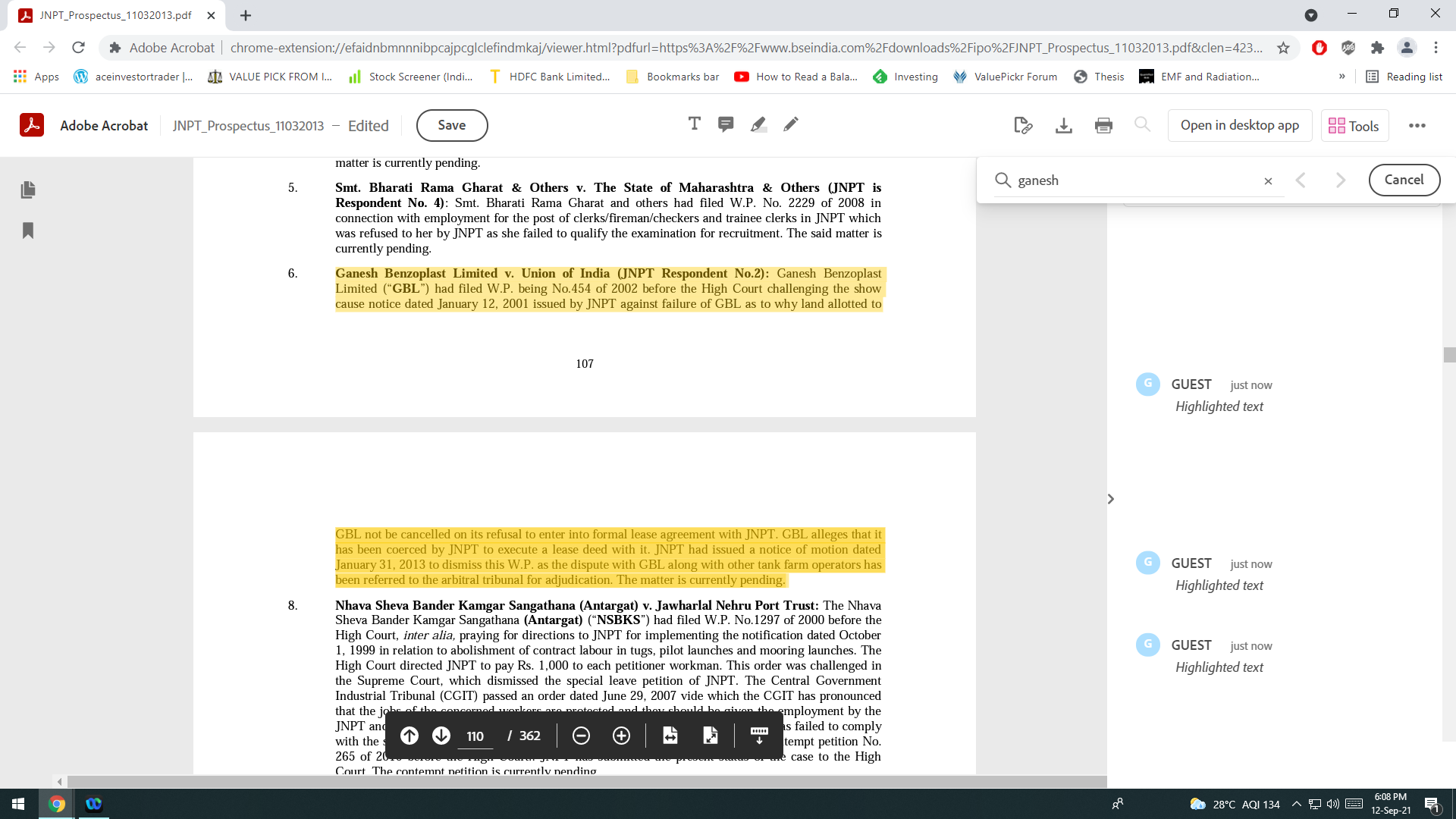

Now the case is at Supreme Court of India for further proceedings. There is high probability that the case will be in company favour looking at the grounds in which high court has passed the order.

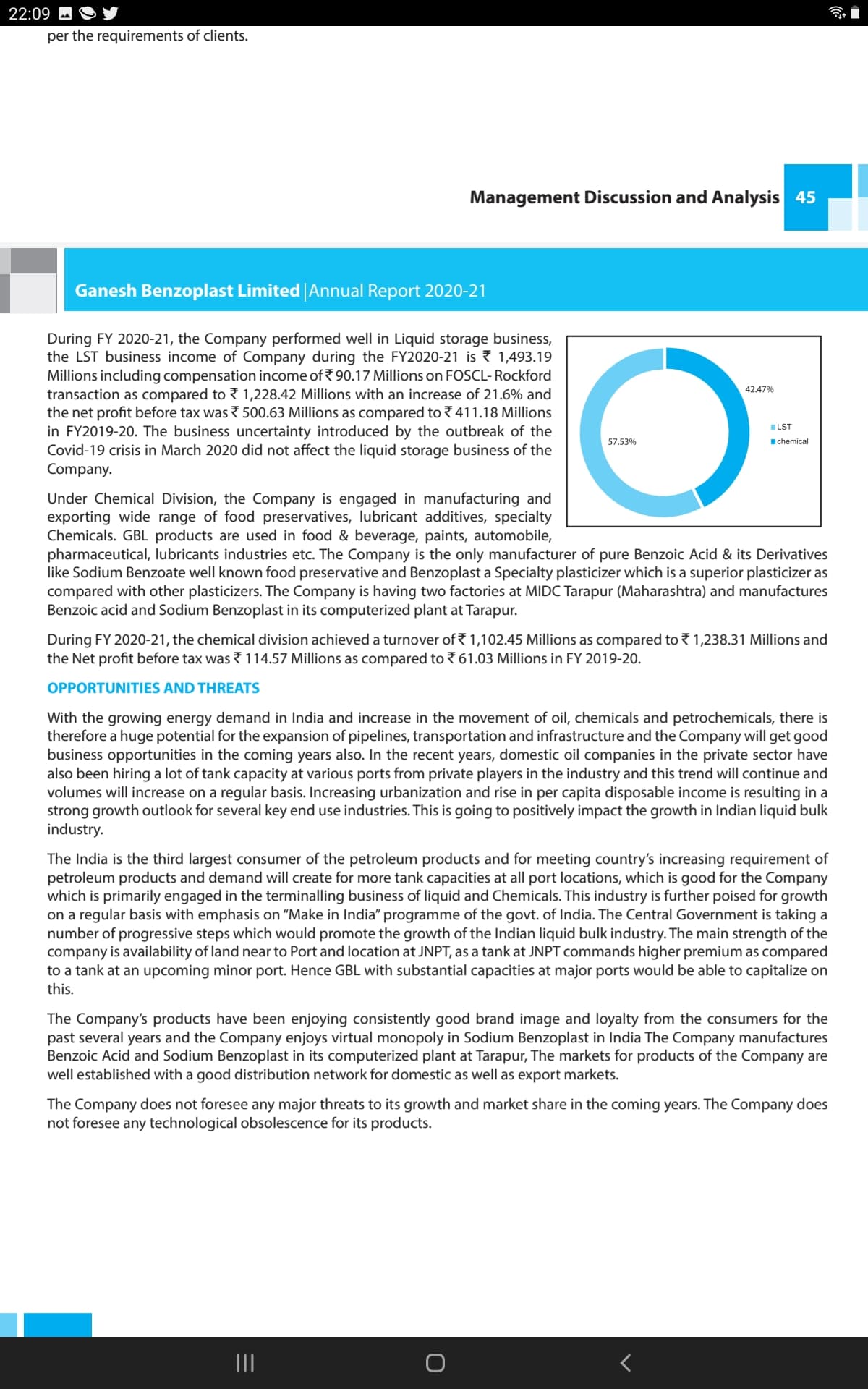

OPPORTUNITIES AND THREATS under MDA

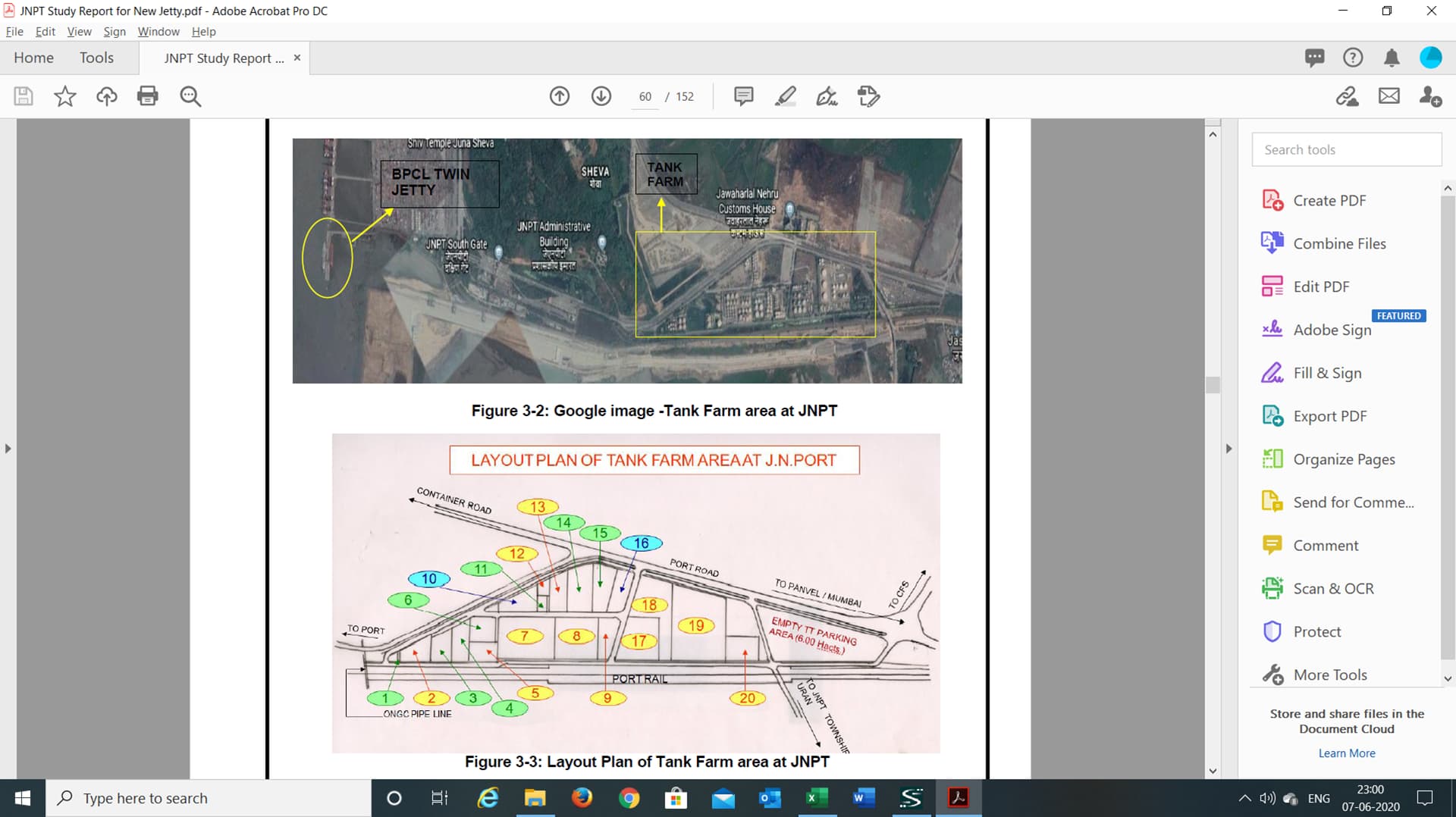

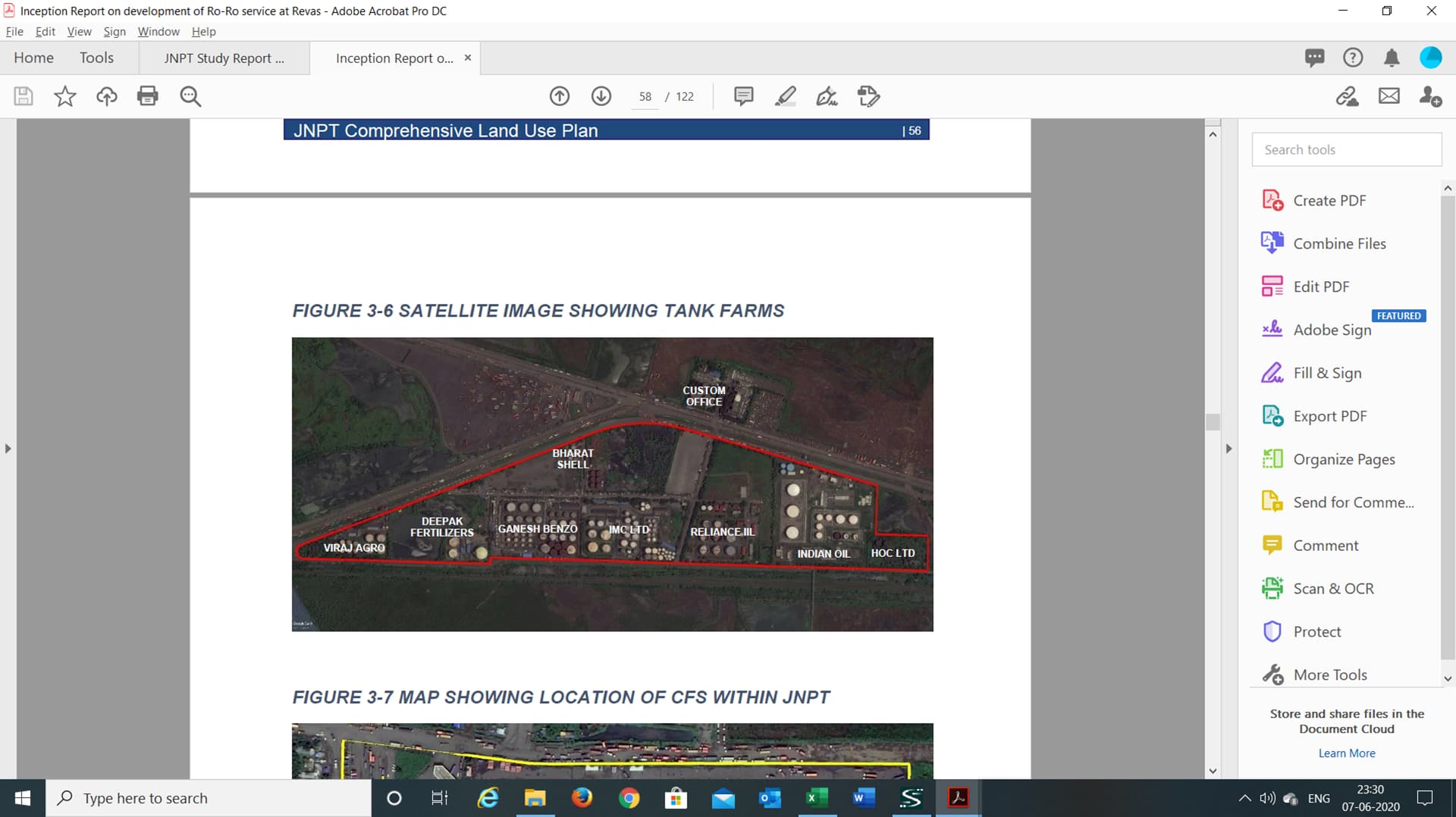

The main strength of the company is availability of land near to Port and location at JNPT, as a tank at JNPT commands higher premium as compared to a tank at an upcoming minor port. Hence GBL with substantial capacities at major ports would be able to capitalize on this.

Container Shortages can lead to higher rentals for LST division as well.

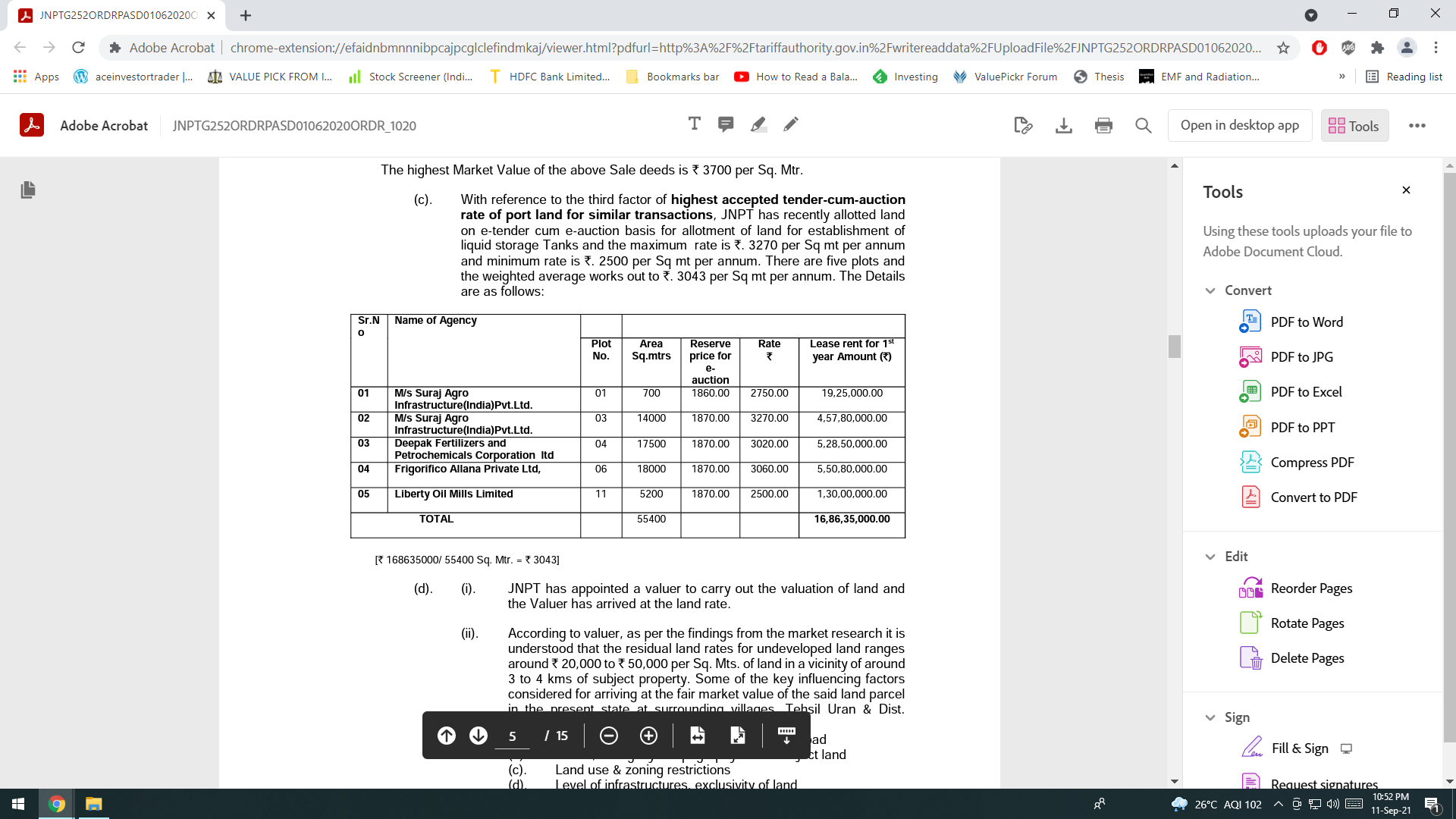

Found this on internet. It seems like plot were available for tender but none is issued to Ganesh Benzoplast. JNPTG252ORDRPASD01062020ORDR_1020.pdf (326.4 KB)

Will JNPT connect to Other Ports benefit to GBL as Storage tanks are going to be created in Coastal Berths ?

Result Update

Chemical Division

Sales grown from 34.4 cr in June 2021 to 41.72 cr in Sept 2021

PBIT grown from Loss (3.29) cr in June 2021 to Profit of Rs.75 Lakhs

LST Division

Fabrication (Job work ) and Infrastructure Logistics (Subsidiary) is adding to the toplines but not generating profits and eating up the Margin of LST Rentals

LST

Mar-20

Jun-20

Sep-20

Dec-20

Mar-21

Jun-21

Sep-21

Increase

YOY %

Tank Rentals

25.71

24.00

26.15

29.07

29.86

39.13

32.66

6.51

25%

Fabrication

5.82

-

-

10.20

30.00

-

0%

Stolt - LST

3.23

7.62

4.83

7.31

7.31

100%

31.52

24.00

26.15

42.50

67.48

43.95

39.97

13.82

53%

Profit (inc Fabri)

10.35

12.32

10.97

15.43

10.39

15.85

9.32

(1.65)

-15%

Profit - Stolt

-

0.96

1.95

0.16

(2.69)

(1.79)

-100%

Total Profit

10.35

12.32

10.97

16.39

12.34

16.01

6.63

(3.44)

-31%

Profit %(inc Fabri)

33%

51%

42%

39%

17%

41%

29%

Profit % Tank Rent

33%

51%

42%

39%

18%

36%

17%

No Explanation from Management for Exceptional item of Rs. 0.53 cr in the current quarter and decrease in depreciation cost by Rs.1.20 cr in QOQ

Company has Cash Reserves of Rs.44 cr as on 30th Sept 2021.