It’s just a matter of time before company starts to pay dividend…With Stolt having 10% …The company management will have to reward them with cash payouts (dividend) …Still came onboard in Nov 20…May be a divided will be announced after a year or in Dec 21 or March 22…That’s my view…If dividend is announced earlier it ll be better… Also company should start making disclosures to the exchange.

1 Like

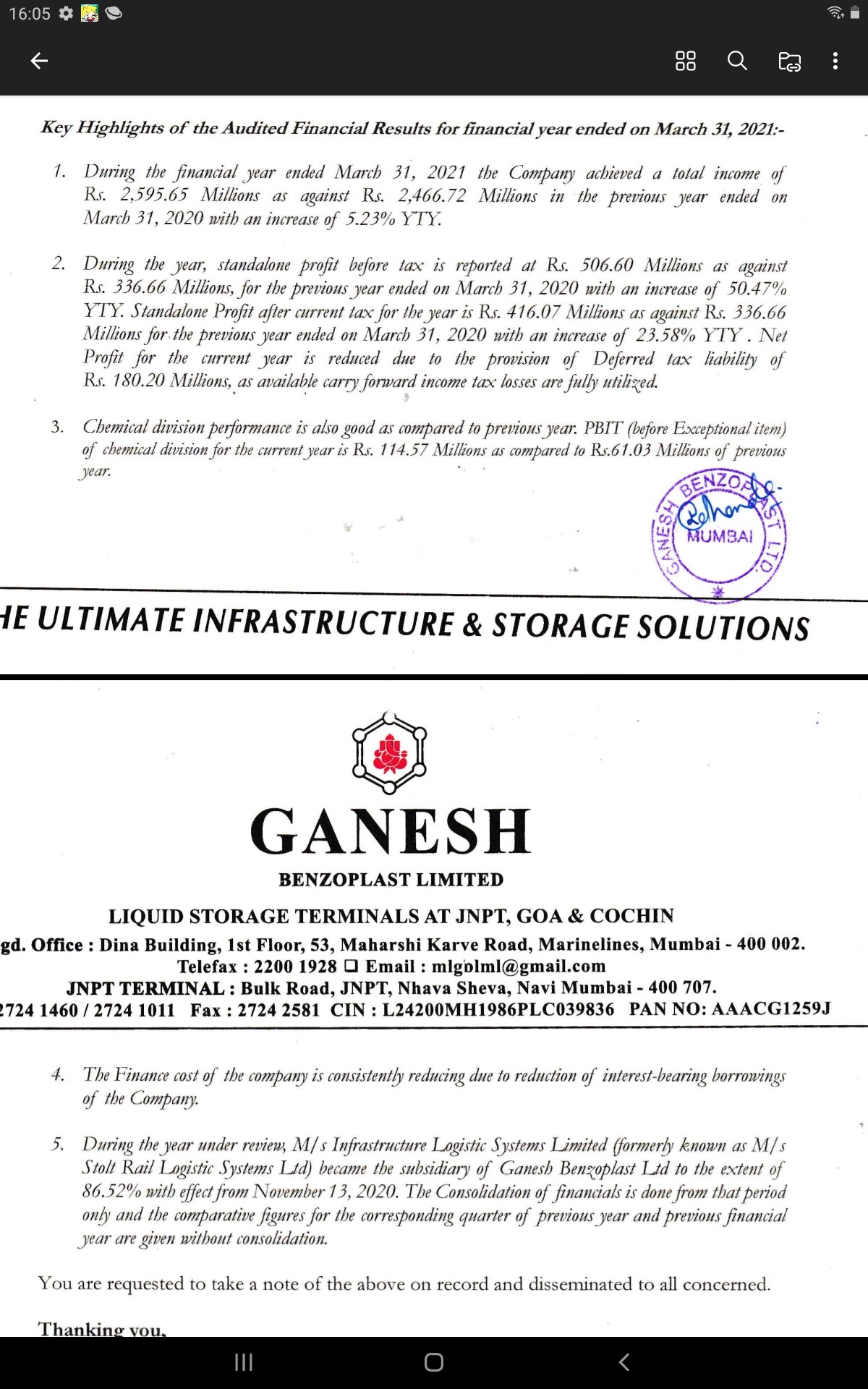

Results-

Seems bad results. But if remove one tym loss of 224 million then at par.

Highlights

Optically down but seems good performance

- CFO has increased by 2.5X YoY at consolidated level

( 26 cr to 61 cr) - PBT from 41 cr to 59 cr for

- Revenue from 246 cr to 270 cr

- LST division revenue from 122 cr to 160 cr, PBT from 44 cr to 53 cr - can see that bottomline has been majorly contributed by LST

- at normal tax rates of 25% , PAT would have been close to 50 cr range and with increased equity base of (6.2), EPS would be 8

Overall Good year, LST stands out, Chemical is drag in last two Qtrs and Okay type annually.

Demerger is big trigger.

1 Like

But they haven’t talked about demerger this time too. Still not sure how much time they will take.

Thesis/Stories is still intact . Two big trigger points for decrease in PAT

- Creation of Deferred tax liability of Rs.22.40 cr which is a good sign as management is bullish for future profits.

- Margins of Fabrication work which has lead to decrease in profits slightly but it should bounce back in coming quarters

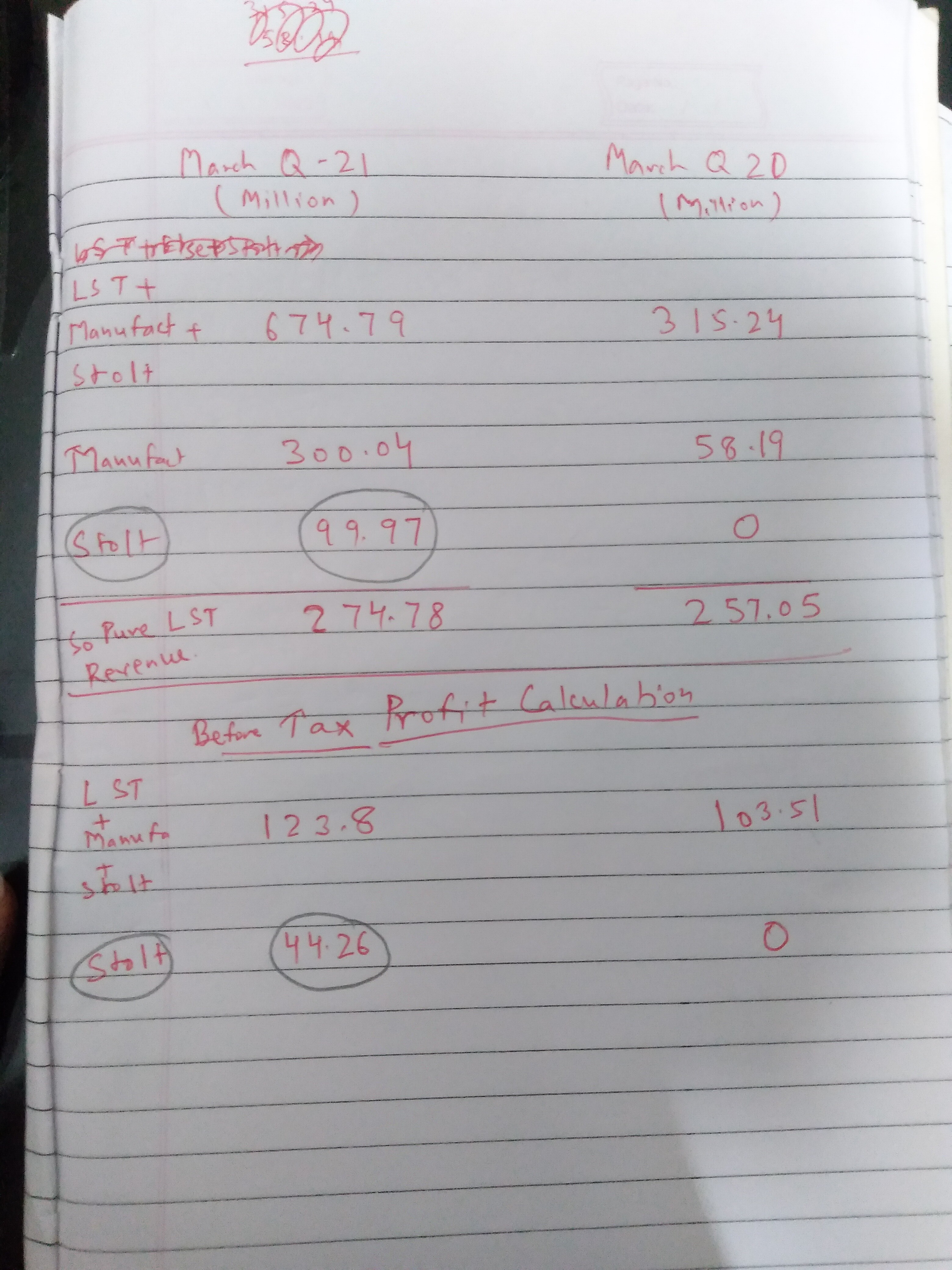

March 2021 LST Result Comparison

| LST | Mar-20 | Jun-20 | Sep-20 | Dec-20 | Mar-21 | Increase | Percentage |

|---|---|---|---|---|---|---|---|

| Tank Rentals | 25.71 | 24.00 | 23.55 | 29.07 | 29.86 | 0.79 | 3% |

| Fabrication | 5.82 | - | 2.60 | 10.20 | 30.00 | 19.80 | 194% |

| Stolt - LST | 3.23 | 7.62 | 4.39 | 136% | |||

| 31.52 | 24.00 | 26.15 | 42.50 | 67.48 | 24.98 | 59% | |

| Profit (inc Fabri) | 10.35 | 12.32 | 10.97 | 15.43 | 10.39 | (5.04) | -33% |

| Profit - Stolt | 0.96 | 1.95 | 0.99 | 103% | |||

| Total Profit | 10.35 | 12.32 | 10.97 | 16.39 | 12.34 | -4.05 | -25% |

| Profit %(inc Fabri) | 33% | 51% | 42% | 39% | 17% | ||

| Profit % Tank Rent | 40% | 51% | 47% | 56% | 41% |

Reason for decrease in LST Segment profit could be due to various reasons:

a. Tank Rental Profits is getting knocked off against Fabrication work losses as there are very minimal chances that tank rental margins can decrease. Is fabrication business a loss making venture ?

b. June 20 qtr rentals were exceptional as rental prices were high due to Covid 2019.

c. In Dec 20, Fabrication work has generated profits as LST division has margins of 40% to 45 %.

d. There is a possibility that Fabrication work revenue/profit are derived basis on percentage of completion method so previous quarter profits have been reversed in current quarter which has lead to sudden decrease in margins.

e. Depreciation has increased in current quarter by Rs.1.18 cr due to capitalization of Storage tank in previous quarter and acquisition of stolt business.

4 Likes

Would u please explain me more about Deferred Tax liability as how to calculate? Is it a type of advance tax? Can they pay advance tax in March quarter?

Deferred tax liability is just a provision .It is an expectation that there will be future tax liability in coming years and it will be reversed and actual tax will be paid.

Ganesh has done it first time in March 21 qtr which lead to such huge amt ,it is normally assessed on every qtly balance sheet.

2 Likes

Just trying to start more discussion on results. When i looked at first time it looked average but after some serious look i found many interesting things and those findings i would like to highlight here. Replies to this post will further clear my understanding if i got it wrong.

I would like to put in points

- Standalone Deferred tax is 18 crore, consolidated is 22.4 crore (means stolt paid 4.4 crore tax) and net loss for Stolt is 2.5 crore (i.e profit after tax) it means PBT is 2 crore.

- If we just extrapolate quarterly number for Stolt then Revenue comes around 40 crore yearly and 8 crore PBT.

- Company able to got it’s Other Financials Assets from 19 crore to 9 crore this year end These were due last year also

- Net cash flow is 62 crore impressive because if we go by the Trading and Manufacturing nature of biz which is 50% of total turnover this quarter is capital heavy and can easily block capital equal to turnover.

- lnvestments in Bank Deposit/Mutual Funds/Equity Shares have gone up to 19 crore from 0 last year.

- Current account balance 10 crore up from 3 crore.

So overall results are robust my only concern remained is the Trading and Manufacturing biz. How much they want to scale it up and how much ROCE it could give?

To dig more about profitability of Manufacturing/ Trading we need to compare YOY results of past years.

As per my knowledge Stolt is having Cargill and Punjab Alkalies & Chemicals as its client and talk to acquire 3rd client is in progress. Company have assets in terms of Warehouse and Wagon at Pune, Daund ( Maharashtra) and Nagpur.

5 Likes

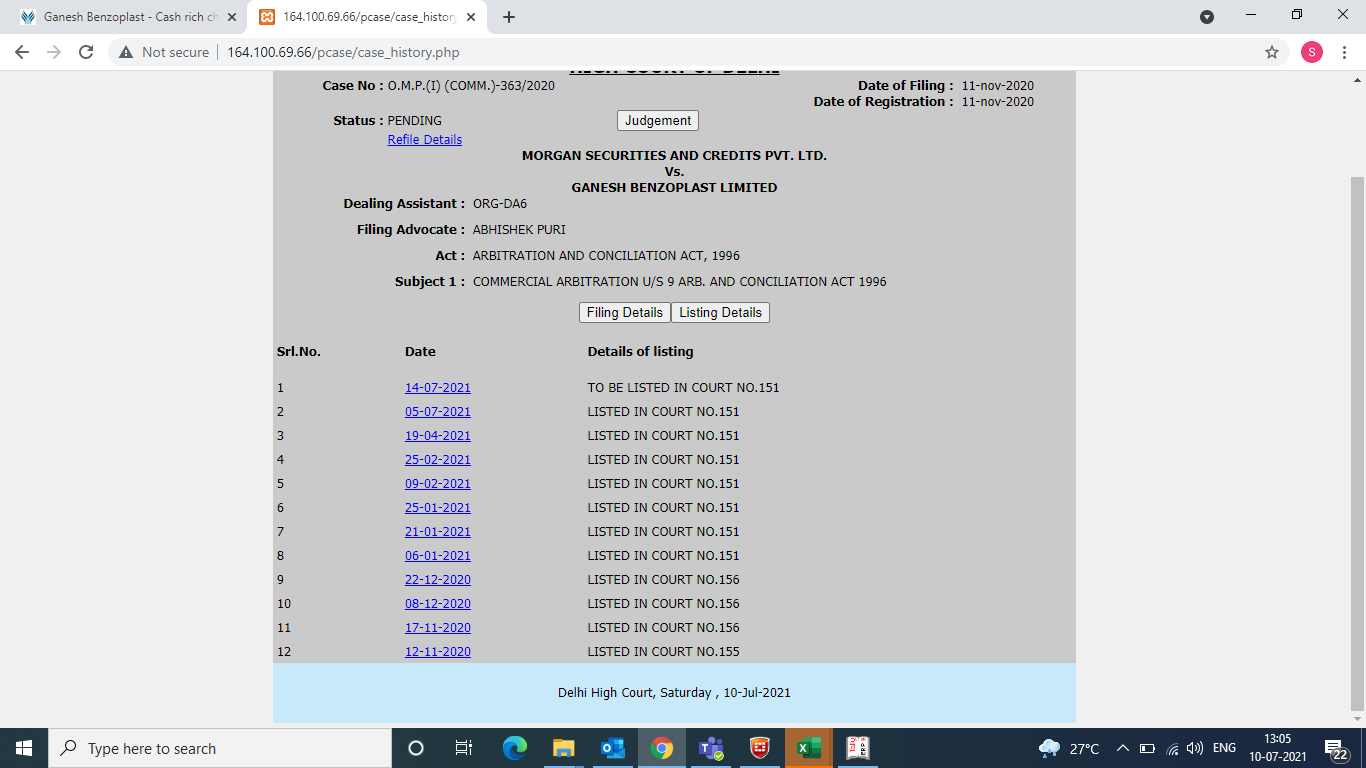

@RajeevJ What are your views on Ganesh Benzo’s recent results sir?

How do u see this company gets going after settlement and demerger?

Also would like to hear u about Shareholding pattern emerging in recent quarters. Shareholding below 2lakh is decreasing at faster pace and in June update FPI holding came up and HNI holding is also increasing.

Market knows that Liquid storage biz is going to grow in single digit only till any new land is acquired. Chemical biz wont grow or make profit as it is a simple and has no specialty or pricing power. How new ventures Stolt Logistic and Manufacturing& Trading performs on return ratio metrics? How stable cash flow from LST will be used, reinvestment at same ROCE or distributed? If cash is not utilized for same ROCE then market is not in hurry to give it decent valuation.

1 Like

10 % up on 14 july. There must be some uphoria about the hearing and there might be good news too. Respected boarders please enlighten us if you have any confirmed news

The liquid storage & logistics business is all set to undergo a transformation in the country with the recent JV announced by Aegis Logistics with Royal Vopak of the Netherlands, World’s leading Tank storage Co. The JV signifies that the next few years will see an influx of many foreign players into the country to set up plants requiring tankage storage.

https://www.vopak.com/tank-storage

What the Aegis Vopak JV will do is establish valuation benchmarks for the liquid storage industry. Stolt Neilson already holds 10% stake in Ganesh Benzoplast & Vopak’s entry into the India will certainly hasten the process of Stolt consolidating its position in Ganesh by upping its stake. The business itself will expand with both these multi nationals looking for increased market share.

Another interesting discussion emerged in the investor concall of Aegis Logistics. The Aegis promoter clearly stated that going forward the business was not going to be limited to the ports, but would grow into inward logistics offering better value to the customer. Ganesh Benzoplast has only recently acquired the rail logistics Co., that was earlier being run as a JV partnership between its promoters in their individual capacity with Stolt. This internal logistics business is set to grow rapidly over the coming years.

14 Likes

Continuing the discussion from Ganesh Benzoplast - Cash rich chemical storage/tank king:

Very Detailed PDF by HDFC securities on GB’s Operations.

2 Likes

Sir, the link seems to be broken. Could you kindly share the pdf

Good Results

Profits before tax has increased to 12.30 cr from 10.06 cr in March 2021 qtr which is mainly due to increase in LST profits which is offset by loss in chemical division.

Fabrication business is adding to the bottom line which should make us cherish till the time litigation with Stolt (Demerger) and adjacent plots start generating rentals.

Comparison of LST division with previous qtrs

Assumed Tank rentals same as march 21 qtr as bifurcation not given by the management.

| LST | Mar-20 | Jun-20 | Sep-20 | Dec-20 | Mar-21 | Jun-21 | Increase | Percentage |

|---|---|---|---|---|---|---|---|---|

| Tank Rentals | 25.71 | 24.00 | 23.55 | 29.07 | 29.86 | 29.86 | - | 0% |

| Fabrication | 5.82 | - | 2.60 | 10.20 | 30.00 | 9.35 | (20.65) | -69% |

| Stolt - LST | 3.23 | 7.62 | 4.74 | (2.88) | -38% | |||

| 31.52 | 24.00 | 26.15 | 42.50 | 67.48 | 43.95 | 24.98 | 37% | |

| Profit (inc Fabri) | 10.35 | 12.32 | 10.97 | 15.43 | 10.39 | 15.85 | 5.46 | 53% |

| Profit - Stolt | 0.96 | 1.95 | 0.40 | (1.55) | -79% | |||

| Total Profit | 10.35 | 12.32 | 10.97 | 16.39 | 12.34 | 16.25 | 3.91 | 32% |

| Profit %(inc Fabri) | 33% | 51% | 42% | 39% | 17% | 40% | ||

| Profit % Tank Rent | 40% | 51% | 47% | 56% | 41% | 54% |

Chemical division has generated a loss of Rs.3.26 cr against sales of Rs.34.40 cr for which management has given below explanation

“Lower than expected performance in chemical division was on account of lockdown impact in first quarter resulting in substantial increase in prices of raw material without corresponding increase in prices of finished goods as well as stoppage of production for a few days in one of the manufacturing plant at Tarapur on account of notices issued by MPCB to the common effluent plant of 'Tarapur, MIDC.”

It was an temporary phase and will recover at the earliest as done in previous quarters.

Good point to note is that there is no exceptional item in this quarter after a long time.

4 Likes

Yes, its heartening to see no exceptional items. Chemical biz will remain a drag to company’s growth. LST as a pure biz segment has also peaked out and wont be growing till that plot is acquired. Court case is a big drag on demerger or sale of chemical biz. I hope that Rishi must have had some learnings from his Father’s Diworsification endeavor. Company is not sharing its planning properly.

1 Like

GBL has incorporated new WOS as GBL Infra Engineering services private limited w.e.f. August 9,2021

The main business of the Company will be to provide complete design and engineering services and solutions for EPC projects including procurement and supply of all materials, installation and commissioning of projects for bulk storage tanks for chemicals, Liquids, petroleum-based products, edible oils etc. internal pipeline & structural works, cross country pipeline etc.

Going forward, fabrication work should be done under this umbrella as work is similar to it.

Further GBL has incorporated new WOS as GBL Clean energy private limited w.e.f. August 11,2021

The main business of the Company will be to deal in clean energy fuels viz. ethanol, ethyl alcohol, bioethanol, butanol, bioalcohol, methanol and Isopropyl alcohol and other cleanener$/ and biodiesel fuels, bio-oils and other agro based products etc. including wind, solar, hydro, Bio-mass and other non-fossilised and non-polluting energy sources.

Chemical business will be diversified through this venture mostly and will became profitable.

3 Likes

Their experience in storage tanks will be a plus in gaining customers for GBL Infra Engineering services private limited. We need to see how they will execute it going forward. If this clicks, it will be another storage tanks kind of stable income. It all depends on how focused the management will be in executing these.