The Mgt at the AGM had confirmed that the Land allotment had as good as come through, with some minor technical issues to be sorted out. With Stolt as a important stakeholder in the Co., it is very likely that it would play a major role in the Co.'s future growth plans. With Stolts technical superiority, it is unlikely that the Co. would go in for the regular tanks for petro / chemicals storage for which it is more than capable of going ahead on its own. The Co. is likely to go in for storage of some kind of hazardous liquids that command much higher rentals. Even LPG could be a possibility, given Stolts expertise in it. That could be a huge positive as the throughput for LPG is about 10X. It would be interesting to see what route Stolt takes to increase its presence in the Co. Stolt is a world renowned name, about 100 times the size of Ganesh & desperate to have a meaningful presence in India.

I understand that the loss in rail logistic business is more of a one time issue & going forward things should get back to normal as the business is doing quite well. The exceptional item of Rs. 0.53 cr pertains to the final instalment paid to Avron Chemicals under a mutual settlement entered into a few years back.

We are aware that the Co. has legacy issues, that are gradually getting addressed. However, what is clear is that both the business as well as the financials have never been in better shape. The chemical business too is seeing traction & it could all come together in the next few qtrs.

Promoter buying from market of 370000 shares, typically a good sign, lot of triggers and possibilities for value unlocking overdue, has tested patience in bull market, goodprice volume action today, looking good on charts , near ATH of 102 in 2017 - taking that out can give significant upside , fundamentals and balance sheet much stronger currently , TTM available at 1.5X sales and 9X EBDITA ( suppressed currently and has delivered 30% on longer term range).

Meeting of the Board of Directors of the Company will be held on Tuesday, 1’t February, 2022, inter alia, to consider the following businesses:

Raising of funds by way of fresh issue of Warrants Convertible into Equity Shares to Non-Promoters on Preferential Allotment basis in accordance with applicable provisions of the Companies Act,2013 (including any statutory modification or reenactment thereof for time being in force) and the Securities & Exchange Board of India (Issue of Capital & Disclosure Requirements) Regulations,201.8 and subsequent amendments thereto. Ganesh Private Placement Feb 2022.pdf (772.1 KB)

QoQ looks good and bit consistent, if this is new base , i.e. Q3 101 cr revenue and 10.5 cr profit at consol ( op margins Def has been much higher in past and should go up at median 25%+ from current), at current run rate it is annualized 1.5X sales and 15X PAT, most small cap chem are 15-20X EBDITA- significant room for rerating

Promoter has bought sizable qty around current prices - should provide a good base for next leg of journey , warrants issue lined up as well

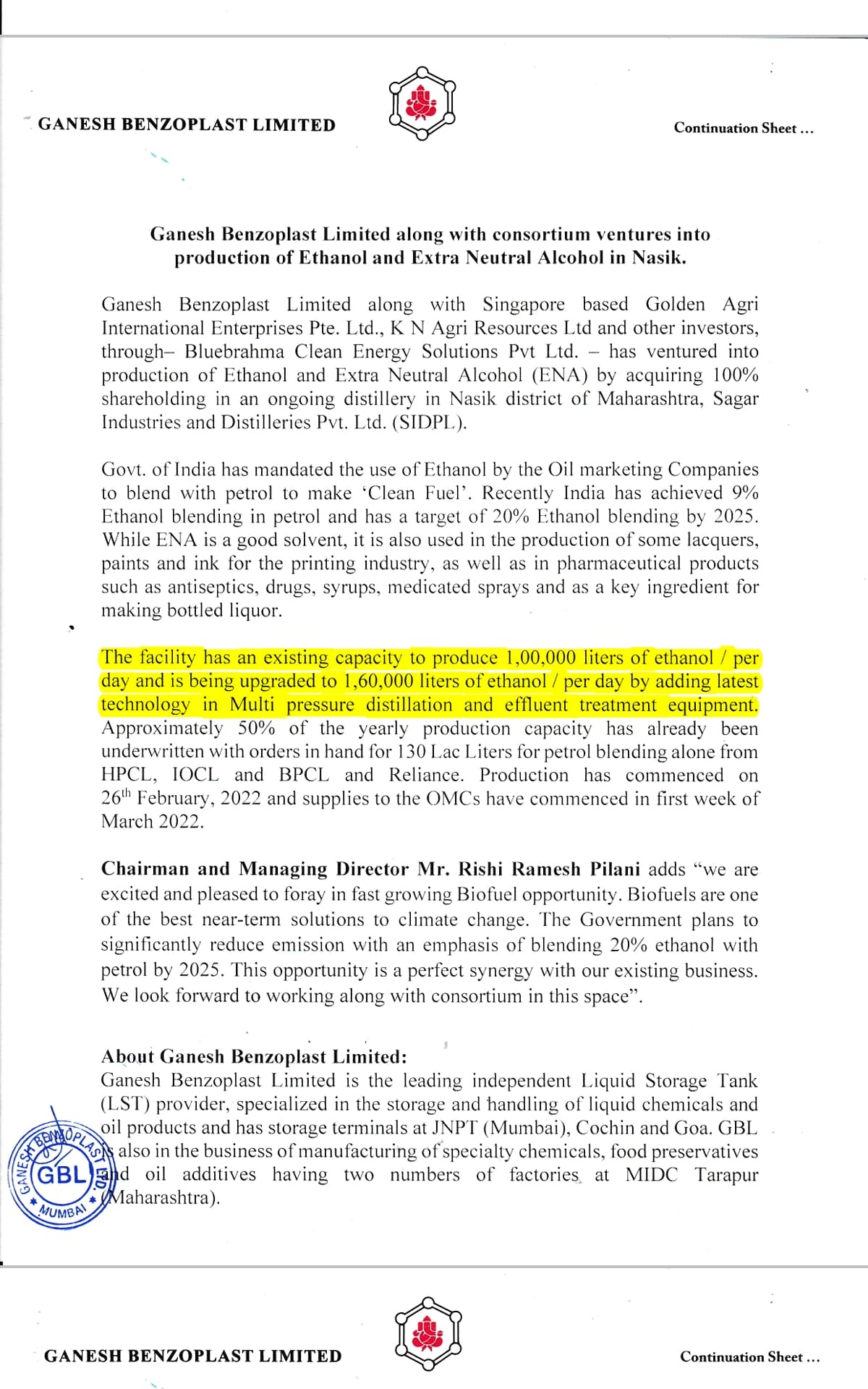

Variance in Standalone and Consol Chemical Segment Revenue is Rs.4 cr and Profit is Rs.35 Lakhs which should be majorly GBL Clean energy Limited i.e Ethanol and so on. Expecting sales and margins to improve in clean energy fuels which has a tremendous demand outlook.

Variance in Standalone and Consol LST Segment Revenue is Rs.6.87 cr and Profit is Rs.2.43 cr (margins is 35%). It should be majorly due to Stolt Rail Logistics Limited business.

LST division segment assets is increasing on continuous basis from March 2021 of Rs.269 cr to 328 cr in December 2021. It had already added 60 to 65 cr in 9 months which should further increase post preferential allotment of convertible warrants of Rs.61.8 cr

This is in partnership with two other entities, one local and other global player ( listed in Singapore- Golden Agri)

Investment value and share is not detailed out in release

A quick way to understand Investment per some other players is - 60 Lac per klpd - per Ganesh press release the capacities will be at 160 KLPD, I.e. Approx 100 cr asset. Shared by all parties.

Ethanol per ltr price here( 45 to 60 depending on type)

REVENUE POTENTIAL- 160000 Lt per day at 50 INR to be 80L per day, 25 cr per month, 300 cr per year for a 100 cr asset at peak utilization - HIGH RoCE - If equal share then 100 cr for Ganesh/ yr - ofcourse it’s at theoretical peak capacity and 33% share.

Ganesh did 100 cr+ in Q3, given Ethanol supplies started in March, some addition in Q4 nos, full impact in Q1 23 onwards for 25 Cr+ per qtr( if equal share at 1/3, high if more share).

There seems to be very high quality biz with Ganesh

Storage vertical - always near full utilization, high margins

Transportation ( Via Stolt)

Bio fuel ( Ethanol) - likely to run at high utilization, good margins

In addition to above is EPC, Chemical biz - these do not have similar characteristics as above three.

Current mkt cap is 600 cr+, There is no reason as to why FY 23 should be less than 500 Cr -600 revenue( Q3 was 102 cr run rate, add Ethanol biz and scaling of core biz) , last few years margins have been 25-30% type, if they get back there , should do EBDITA of 140-150 cr.Thats 1X sales and 4X EBDITA. Not to forget Promoter has bought stake near 100 in Dec, Jan from market.

They need to simplify org structure and communicate better with market, a significant re rating is possible. Margins a key monitorable as well.

60,00,000 Walrants convertible into equal number of equity shares of Re 1/- each of the company at issue price of Rs 1-3/- per warrent on preferential basis to promoteors and non-promotors

This will be worth INR 15,45,00,002

I recently exited Ganesh Benzoplast. As I have been regularly writing about the developments, usually positive, for about three years now, I felt the need to let fellow valuepickrs know.

The Co. diluting equity by issuing shares to a whole host of retail investors were a concern. Dilution, if it meant issuing shares to Stolt was different, in that Stolt was a strategic investor who added value to the Co. On one hand the Co. has been making profits for the last several years & still not giving dividend, apparently due to anticipated objections from Morgan, & on the other going ahead & further diluting equity.

The 26% stake that the Co. has taken in Bluebrahma Clean Energy doesn’t move the needle much. A listed Co. like Ganesh with adequate resources needs to have a meaningful stake of at least 51% in any venture to justify investing. Liquidity can be a double edged sword & mgts. sometimes misallocate in their quest for scale. One can only assume that the equity dilution was to enable investment in taking a 26% stake in Bluebrahma.

The formal announcement for land allotment for additional land at JNPT is still to come. It’s now close to a couple of years of waiting.

Another reason was that with volumes going up, one was able to exit even a biggish position with sizable gains!

Core biz - LST related expansion, quite bullish statements in press release, need to see which path mgmt takes for funding capex. Last qtr or so has seen sizable qty mkt purchase from promoters, last year has been eventful as well.

Finally they got something to cheer about. After so many broken promises some good is happening now to this company. But intention of management alone may not be the reason that they could not do what they mentioned in AR or at other forum. Like demerger of chemical biz is not happening due to case pending in court, Installation of Liquid Gas terminal at Goa could not be done due to opposition by Public and some unfortunate incidents at Goa site. Management remained silent in terms of future plan but doing small small addition to its Biz like Manufacturing of Steel Vessels and pipeline, addition of Stolt Logistics assets and investment in Ethanol plant. Falling ROCE due to these low ROCE biz to LST dented its valuation but missing of future growth in its main LST biz was a major reason for low valuation even in bull market.

This recent development has just given its new life and i think it was all known to stolt or other preferential allottees thats why they are interested in it. And we can say we too were anticipating it to happen but it tested our patience. I have also pared my position to 1/4 of my original holding. Though investment equal to 80% of it’s Current Gross block and small payback period is to be taken as pinch of salt. Market like paka pakaya khana and wont give value to its announcement till it is there on the land and operating.

My take would be to wait and if the valuation comes close to 400cr Mcap i will be very much interested in it but till then lets see how fast they could setup new capacity and do something meaningful with Logistic biz.I am not interested in manufacturing segment as it is very WC intensive and low ROCE. Management should be more communicative at least in there results.

I attended their Q2 concall and am sharing my notes below.

FY23Q2

19’000 kl JNPT expansion: Should be commercialized by March 2023. Building 19 tanks and all have already been contracted. This expansion is custom made for customers with potential revenue of 15-18 cr. and 70-75% EBITDA margins. This is higher realization vs existing capacity

Advanced talks with customers for LPG storage containers (80’000 – 1 lakh kl capacity; full capacity will be built in 2 years), will have plans ready by Jan 2023.

LPG throughput at other ports is 8-9x/month translating into 96-108 times static capacity.

All evacuation mechanisms exist at JNPT (road, railway, pipeline). The evacuation mechanism used by Ganesh will depend on what customers want

In chemicals division, net capital employed is negative because of depreciated assets and loss tax assets

Disclosure: Not invested (no transactions in last-30 days)

Who bears the risk of the goods stored in the tanks of GB?

If GB bears it, does it insure the risk and what % of Revenue is the insurance cost?

The tanks may sometimes be empty, sometimes filled with customer’s goods. Does the insurance cost vary, accordingly?

Appreciate if anyone can provide answers.