Product

Sponge Iron

Steel melting Shop

Rolling Mill

Captive Power

Wheat products - Atta, Suji, bran sold in UP, Bihar & West Bengal

Capacity

Sponge Iron - 2.97 Lac Ton per annum

Steel Melting Shop - 3.3L Ton per annum

Rolling Mill - 3.3L Ton per annum

Captive power - 53 MW

Floor Mill - 1 Lac Ton per annum

The above capacities are recently expanded at the cost of 235 crores. Commercial production of expanded capacities started on 01-Dec-17.

Please find companies letter dated 15-Jan-18 in this regard here. (256.8 KB)

Expansion

As per the company disclosure dated 24-Jan-18 company wants to expand capacities further as follows

Sponge Iron - 4.45 Lac ton per annum

Steel Melting Shop - 4.95 Lac ton per annum

Rolling Mill - 4.95 Lac ton per annum

Captive power - 73.5 MW

Pellets - 6 Lac ton per annum

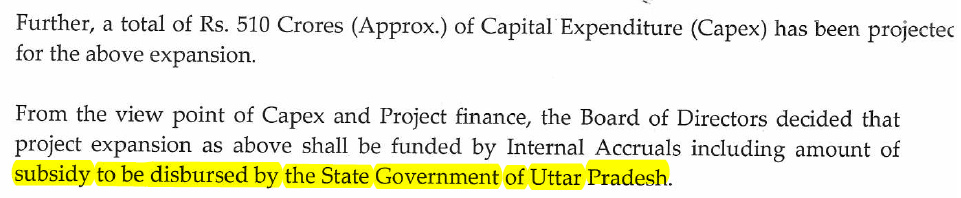

The cost of this expansion is pegged at 510 crore.

Other details like

When will the expansion start? When it will be completed etc. are not know at this point?

Location

Company’s registered office is in Kolkatta and plant is located in Gorakpur Industrial Development Authority (GIDC), Gorakpur U.P

Raw Material

Iron Ore

Coal

Process

Company uses Direct Reduced Iron method for steel production. It is similar to how Tata Sponge produced Steel.

Holding Company

Gallantt Metal is holding company with plants located in Gujarat in similar line of business.

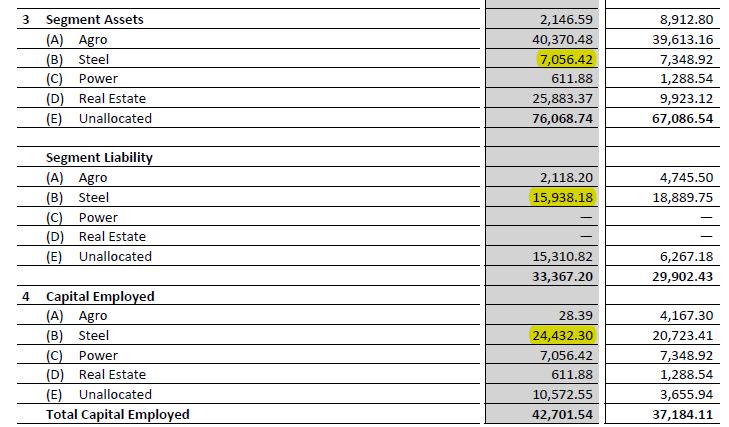

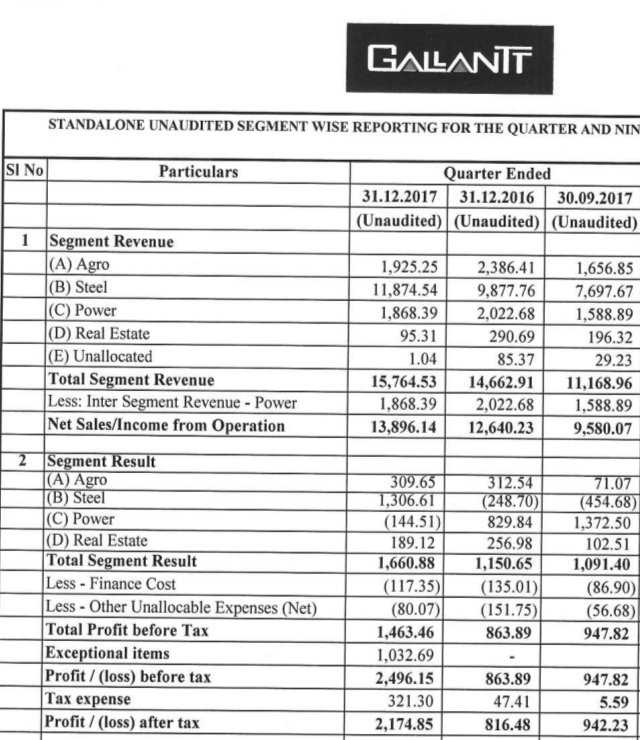

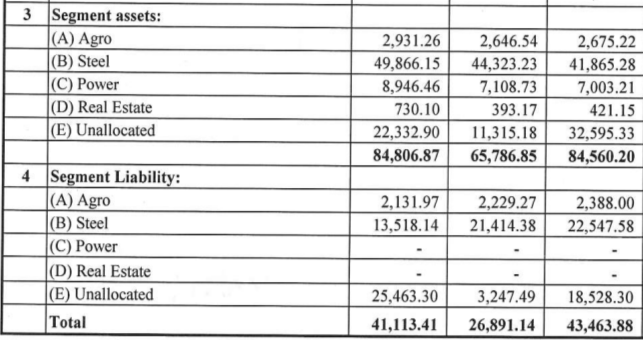

Financials

As always Screener.in is our destination for financial of the company.

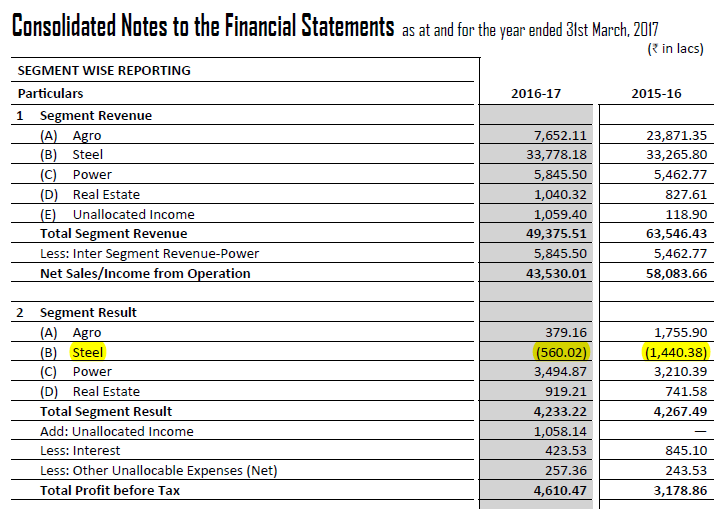

- Consolidated Cash flow from operation is more than Consolidated Net Profit.

- Debt to equity is less than one.

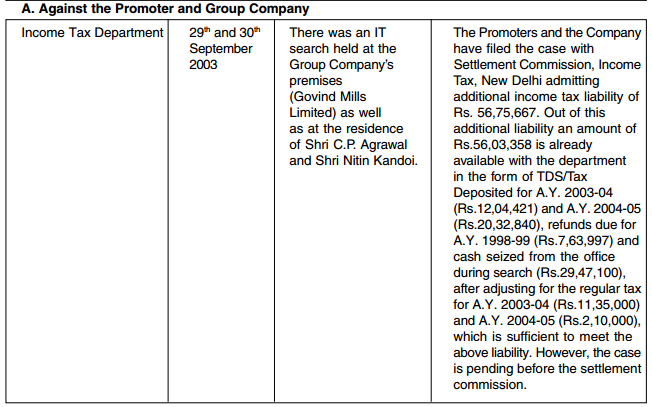

Controvery

- Land takeover for Gorakhpur Metro - There was some news that company land will be takeover by Government for Gorakpur Metro. Management clarified that they have some land bank in Gorkhpur city a portion of which will be taken over for Metro Rail

- Company designated as Shell Company by SEBI - According to this disclosure, shell company status has been removed.

Risks

-

Excessive leverage - Having completed a recent expansion, company has planned for another expansion at the cost of 510 crore. Such rapid expansions are marred with multiple risks.

-

Increase in price and non-availability of raw material - Company does not have captive mine of iron ore or coal. Rapid increase in price of any raw material can derail the company.

Triggers

Iron & steel companies are coming out with wonderful results. Tata Sponge has done very well. Multiple source say India is having very good demand for Steel. Expansion of capacity will lead to increase in topline & bottomline of company.

Invested. Views may be biased.