The oddest part is how all the companies are in kolkatta.Every single one of the top ten non promoter entity is in kolkatta.

These companies will have too much control over the share price.

The oddest part is how all the companies are in kolkatta.Every single one of the top ten non promoter entity is in kolkatta.

These companies will have too much control over the share price.

The prices howers around a price for a long time.

Whats your take on Gallant Ispat results? seems OK at first glance

Results seem reasonable to me, nothing great. If I remember correctly raw material cost is higher this quarter & write-back of subsidy.

But I believe full benefit of expanded capacity will come into play this year.

Thanks

Been tracking this company for a year or so now.

i) Management is very good on Capital allocation. Their previous capex cycle, paying off already. The top line & bottom line growth in past 4 years have been highly impressive.

Dec 17 to Dec 18 Quarter- Sales up by 146% and Profit up by 46%

ii) As per Feb filings are now going for a 970 crore capex, (awaiting EC) with work to begin Sep 2019.

iii) Have sizable market share in UP

iv) They have the subsidy case in Supreme court pending : The SC isn’t disputing the lower court rulings that UP govt has to pay up the subsidy to Gallantt Ispat (30 crore already dispersed. 320 crore + another 300+ crores in no interest loan pending to be sent). Thing in question is on mode of disbursement ie the no interest loan part. Gallantt Ispat filed a motion to fasten up the process. Matter has been heard & the final order has been pending since Dec 2018.

v) Gallantt Ispat debt is 250 crore mainly on back of past expansion which has been completed.

vi) They also have been doing backward integration. Signed a PPA deal with UP Govt to supply 50MW power from Nov 2018

So, if I put things together.

600crores + to come from subsidy. Current Market Cap is 840 crores & fixed assets are 450crore+. 250 crore in debt. As per management in CNBCTV18 a while back, subsidy when it comes in will be used to pay off debt and rest used in upcoming capex.

To me, looking at the recent growth in topline, bottomline and the valuation of assets, subsidy money to come in, capex on horizon, it presents a astute management with a steel company in very good shape with good growth for next few years.

Question though is on the shareholder pattern. No institutional investments till now. Elara were in it but moved out few years back. SEBI had them in possible shell company list in 2017 but were subsequently audited and cleared completely. The questions others have asked here is valid on why so many non-promoters group all registered in Kolkata and infact few of them in same address ‘Crooked Lane…, Kolkata’

Company has been based of Kolkata as well. But In the EGM that happened 3 weeks back, they have shifted the registered office from Kolkata to NCT, Delhi (is this a sign of good changes happening ?)

Disc : (no SEBI registered) I have invested a small % in portfolio.

Business wise, everything looks rosy including clear evidence of a very efficient management. But at same time,I don’t want to take the big leap (yet) considering concerns over shareholding pattern. I am a novice in Value Investing.

So, question to experienced folks : Considering above points , what would be your take on this company ? (not asking for a investment advise)

I have been tracking this and invested too. As per my view, this is one of the top class capital utilisation. Getting the Capex done through internal accruals majorly is always a good sign for a company. There is huge land bank too which they are monetising gradually (you can refer real estate income in annual report). Company and business wise there is no issue. But the only issue here is lack of liquidity and to an extent I feel that its operator driven. I too was apprehensive regarding absence of institutional shareholders. But considering the supreme court judgement on subsidy disbursement and the given expansion plans, future looks rosy.

Amalgamation of Gallantt ISPAT with Gallantt Metal completed and the combined entity is renamed as Gallantt ISPAT.

There are some additional restructuring happened

Some subsidiaries are sold to promoters

Proposed cement plant is carried out by sold out subsidiary and land taken for Metro project still not completed

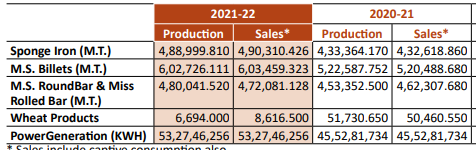

Wheat production for FY22 is 1/10th of the FY21, seems these mills are also getting sold

Major capex are done with palletisation plant alone is pending. Current available capacity is almost twice of the production in FY22. This could help company to grow its revenue for sometime

Gallantt Ispat.pdf (3.2 MB)

This has some minor details about the difference in both the plants operations

12 posts were merged into an existing topic: Gallantt Metal Ltd

what’s really behind the huge surge in stock price over the last few weeks?