Thank you for sharing the note of HDFC Sec Inst. Research. I went through it, and with NHAI FY 18 Annual Report (FY 19 not yet available).

What I gathered from the HDFC Sec note is that:

(a) NHAI will have to continue to raise debt to payback interest till about FY 25, when debt will peak out and then there will be no subsequent material investments. This was the key theme raised by Prof Bakshi.

(b) Toll in various forms will start kicking in from FY 20, including securitization of toll (I guess so, not clear), which will increase and till such time it increases to repay debt on its own, external funding is assumed

( c) Based on HDFC Sec assumptions (which it says is built with a margin of safety), the entire debt payback under those assumptions will be by FY 43

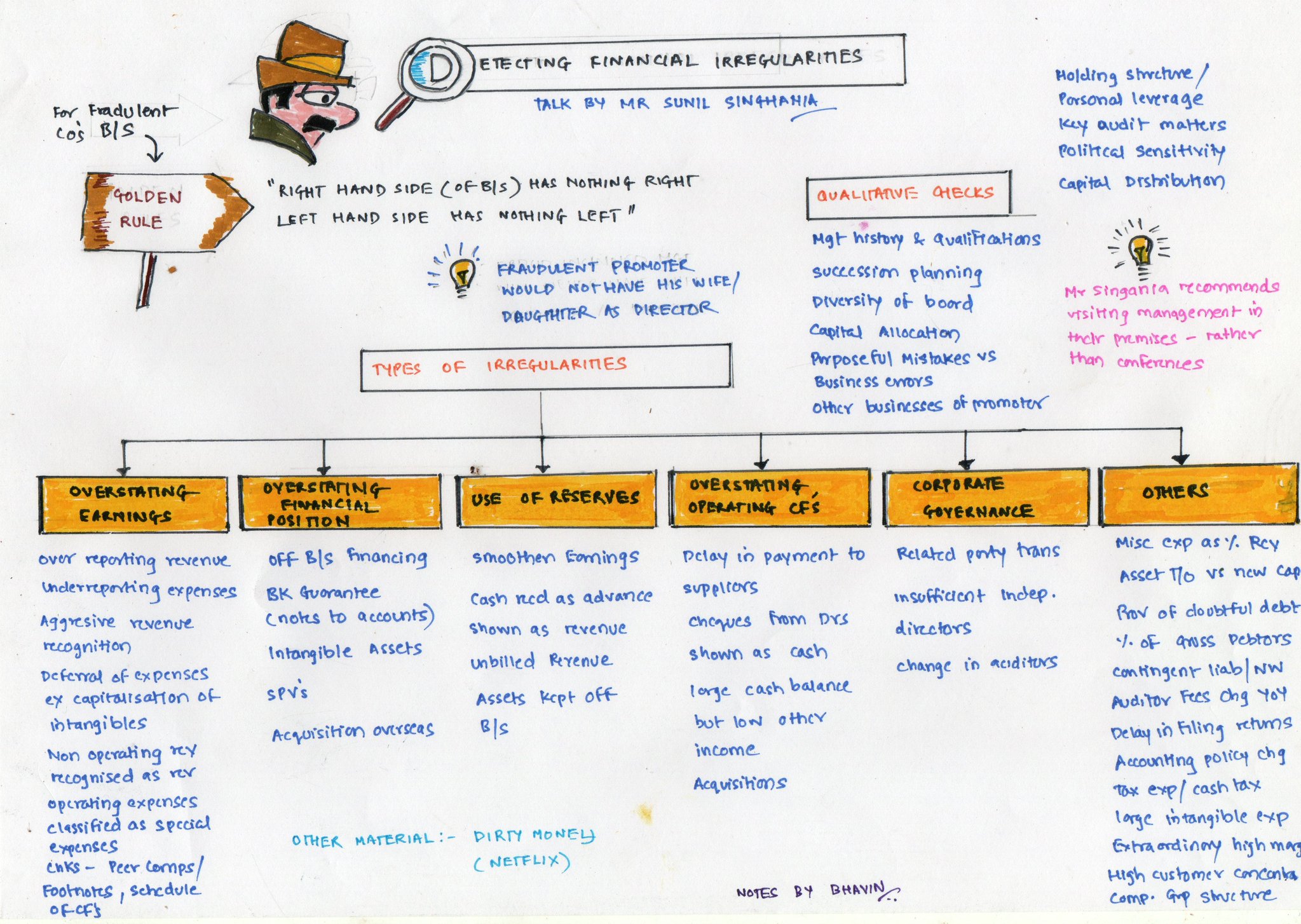

the fall of the Talwalkars, India’s largest fitness group, is not about a business gone bad due to the economic slowdown. Like DS Kulkarni, and Punjab and Maharashtra Cooperative Bank (PMC Bank), this appears to be a case of brazen fudging of turnover and membership numbers and cooking up profits

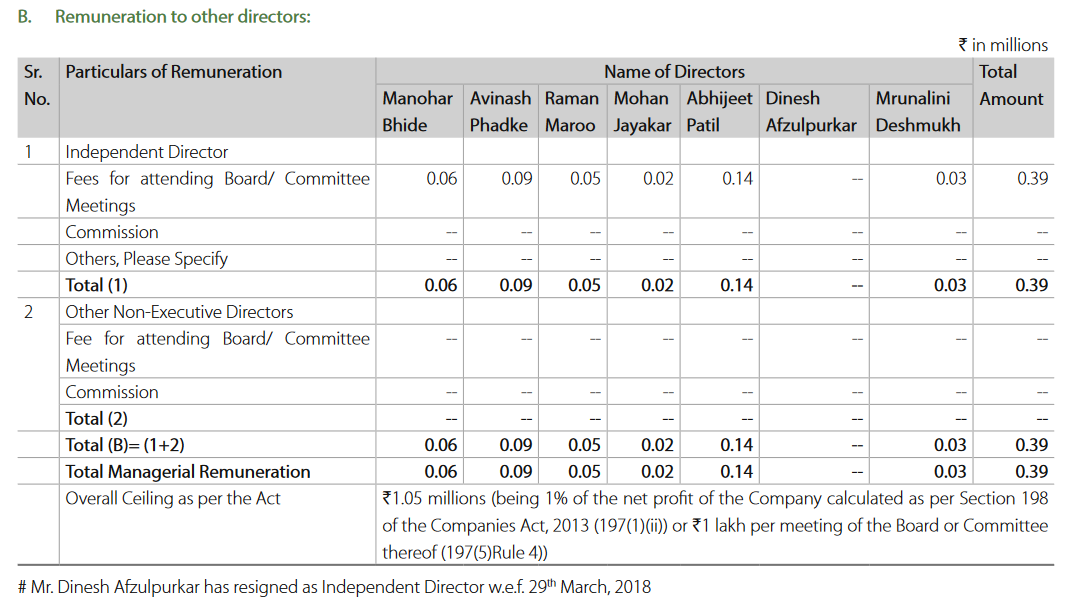

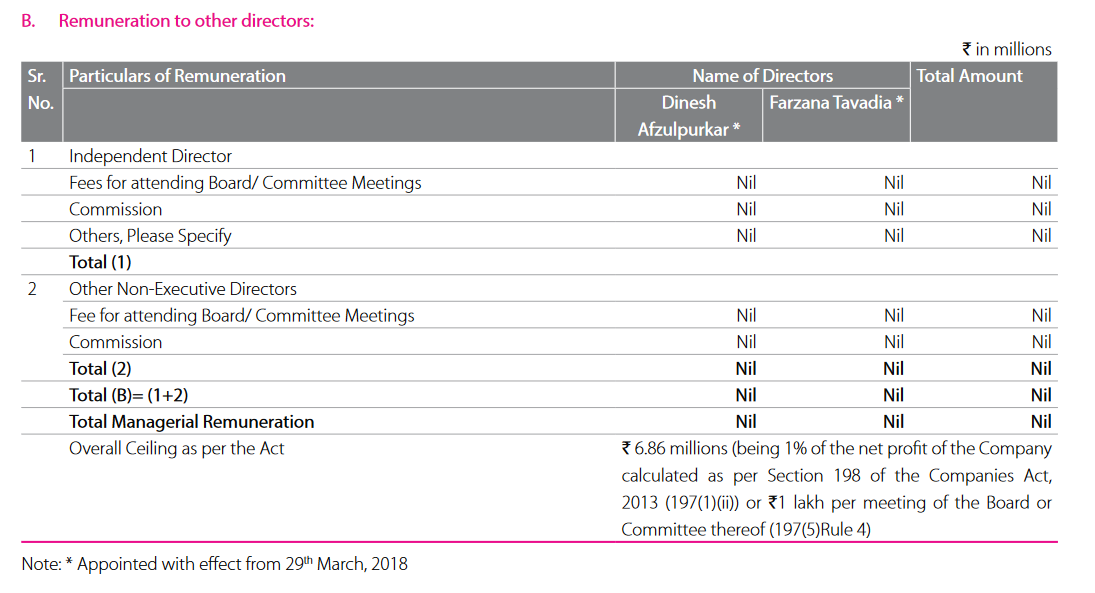

Additionally from the latest annual reports, we can see that the directors’ remuneration was very low.

Some common traits of fraud/suspect management are to come on TV to explain displeasure about falling stock price, Gaming investor with Demerger Merger pr to unlock value idea, Dividend & Buyback etc to show owners are shareholder friendly( Now days even leveraged company want to do buybacks).

I recently wrote to SEBI asking for forensic audit details. I received a response stating that this is privileged information(!) and excluded from disclosure. The query is below and the response is attached Please provide a list of companies where forensic audit has been ordered since 1 Apr 2016 and the soft copies of audit report wherever final report is submitted. This information is requested for learning as an individual investor how to avoid mine traps ReplyDocument SEBI (1).pdf (66.5 KB)

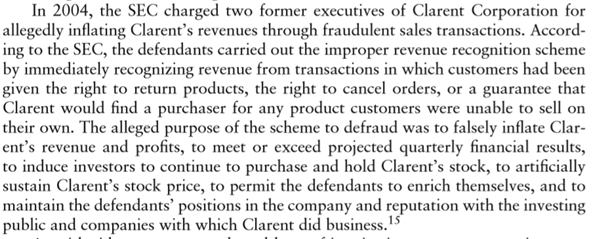

Most common wilful fraud is overstating the revenue in the quarterly or annual returns I am sharing some cases of wilful inflated sales

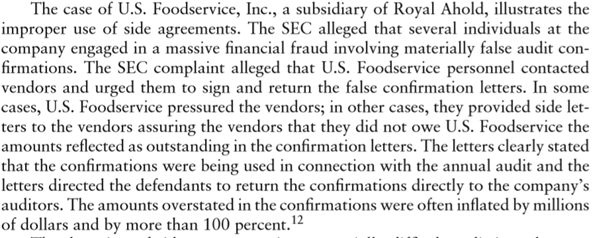

Side agreements

LAX sales agreements can lead to inflated sales

Channel stuffing

I have personally checked in the local market that most of the MNC which work in FMCG I am not deliberately mentioning the name but products are of following categories soap, noodles, baby products , Toffees, chocolate , biscuits , They offer fast moving along with slow moving stuff This also leads to frustration among the dealers / whole sellers which will hamper the company in long horizons

Bill and hold transactions

What is this ? In this buyer under pressure of seller made commitment to send the Purchase order but not paid the amount which will be paid in due course the shipments are forwarded to a third part warehouse and these are booked in the sales but the amount is not realised an examples of it is

Disc : The above examples are from Book : A guide to Forensic accounting Investigation by THOMAS W. GOLDEN STEVEN L. SKALAK MONA M. CLAYTON JESSICA S. PILL which are under copyright ( Copyright C 2011 by PricewaterhouseCoopers ) These are shared for education purpose and if Administrators think it should be removed please be advised to remove the content . Book is Published by John Wiley & Sons

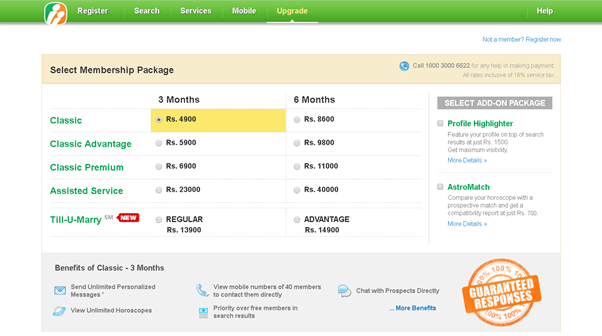

I was recently looking at matrimony.com, the listed matchmaking portal and came across an interesting observation on company’s revenues.

The company primarily earns from subscription services purchased by members looking to benefit from the additional features that are available on the portal, not available to free account users, that can help them find a life partner. Below is some data highlighting the revenue, and customer details –

Particulars

2015

2016

2017

2018

2019

Paid subscribers

647,000

678,000

702,000

745,000

731,000

Portal Billings(in crores)

237

260

285

327

343

Avg. fee / subscriber(INR)

3,657

3,830

4,066

4,386

4,688

Gross Up Service Tax

4,316

4,520

4,798

5,175

5,532

increase by

5%

6%

8%

7%

While Average fee per subscriber has been as per accounts, I have grossed it up with Service Tax so that it can be compared with the rate card.

Company offers various packages to the users starting from ‘Classic ‘ to ‘Advantage’, with rates charged as follows (as of Dec 2019) –

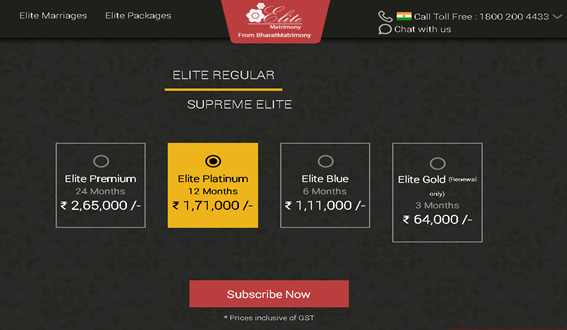

As can be seen from above, revenue per subscriber hovers closes to the most basic package ‘Classic’ for 3 months. This is questionable since company has a range of packages that ought to have paying subscribers too and average revenue per subscriber should not be at the lowest level. This is considering that the company also has platforms like ‘Elite Matrimony’ which charge as follows –

There could be 3 possible reasons for the above –

A very large number of subscribers are simply opting for the cheapest package and are not renewing.

Company is engaging in giving large discounts to customers the customers on the mentioned rates. I had called an agent on the portal to bargain, but got no discounts.

Matrimony.com is overstating the number of its paid subscribers.

With all the 3 reasons negatives for a business, and even a possibility of the third point existing, I abandoned the idea. I have written to the company seeking a clarification, but have got no response yet.

yes, heavy discounting could be most probable. however, its discomforting to see the numbers of subscribers and average fee move this steadily without variance despite such competitive intensity.

also, had seen something similar in numbers for this company called infibeam too.

i could be completely wrong and maybe looking too much at this data point.