The latest in the list of large corporate frauds is Luckin Coffee (thanks for sharing it @Mantri).

A detailed read (link)

The latest in the list of large corporate frauds is Luckin Coffee (thanks for sharing it @Mantri).

A detailed read (link)

@varadharajanr

Thankyou sir for starting this great thread.

I have one question

I have seen many interviews of top investors. Some of the investors claim to find fault in depreciation/amortization rates to check for faults.

Can you explain to novice investors like us that how depreciation rates are important and how can we check accounting fraud with that

Thanks in advance

The first thing to check while looking into the amount of depreciation of company is to read the depreciation policy of the company(specifically to check which method is used by them, straight line or written down value method) and then check the same thing for its competitor, if both the companies use a different method of depreciation, the same can be checked with the management of the company on why they are using a different method.

The second step should be to go through past annual reports of a company and check if they have a history of changing the method of depreciation frequently which might show a wrong picture of their earnings.

Also after certain changes in companies act, it has become difficult to match the exact figures of depreciation, however, we can get some sense on if the company is recording it correctly.

This can be done with the help of peer group analysis, for this, we need to find other companies which are in the same sector, the same line of business along with the same scale of operations.

In such companies as the scale and line of business is same, in most cases, assets of peers will be similar(in terms of size and type) to the company which we might be looking into.

Once we find a peer for the company which we are analysing, we should compare the depreciation expense as % of the total revenue for both the companies, and if the difference is substantial (> 3%), there might be something wrong in either of the company.

Also, one other thing to look for is to compare the depreciation with the type of asset which the company has – suppose XYZ company has total fixed assets of Rs. 1000 and its breakup is building worth Rs.400, Plant and machinery worth Rs. 600. So in a way building forms 40% of total fixed assets while the rest 60% is plant and machinery.

Usually, plant and machinery have higher depreciation rates as compared to a building. So suppose depreciation rate on building(Depreciation expense/gross block) is 11% and for Plant is 15% so the weighted average depreciation comes to be around 14%.

Now suppose after 2-3 years, the total fixed assets of the company grow to Rs. 2000 and the breakup is like buildings worth Rs. 600 and plant and machinery worth Rs. 1400(30:70) and the depreciation rates remain unchanged or if it reduces even when the asset having a higher rate of depreciation growing, then it might be a red flag.

We can also look into the year on year change in depreciation expense of the company and compare the same with its peers, any significant difference might be a red flag.

Hope this answers your doubt.

Thanks.

Most books on Accounting & Finance are American books. So I had a few questions about difference between the American System & Indian one.

In the US, one is allowed to use different methods of depreciation in the Accounting statement as compared to the tax returns. Let’s say a company buys a capital asset, in the Accounting Statement, it may use straight line depreciation, while in it’s Tax returns, it may depreciate the same asset using Accelerated Depreciation. Is such a practice allowed in India also?

In the US, Goodwill can neither be amortized in the accounting statement nor in the Tax returns. What is the case in India?

Like, intangibles of both types (in house created intangibles & acquired intangibles) - can these be amortized in the Accounting statement and/or Tax returns in India?

Answer to your to point no 1is yes.

Good reply by Deep, but allow me to add a couple of more points on this topic @preetkaran:

The Cash Flow Statement has Fixed Assets Purchased, which comprises of maintenance capex and expansion capex. Maintenance capex is linear, rising steadily over the years. Expansion capex is lumpy, with large outflows once in a few years, and nothing at other times. Using this, as well as information available elsewhere such as annual reports, management calls etc., estimate the level of maintenance capex for the company. Now compare maintenance capex with book depreciation. If maintenance capex is significantly higher than depreciation, profits & EPS are overstated to that extent. Factor this into your valuation (though accounting wise company has done nothing wrong).

Usually due to sheer inflation and cost escalation over long periods of time, replacement cost of assets trend higher over a period of time. But book value of fixed assets (Net Fixed Assets) trend lower as depreciation is deducted from Gross Block every year. All Fixed Asset based ratios (e.g. Asset Turnover Ratio) therefore should be taken with a pinch of salt. An old rusty plant that is almost to the end of its life and due for replacement will appear more productive than a brand new factory, though it is the latter which will provide more free cash flows in future years. Or comparing ATRs of two companies give a misleading picture if the age of their plants is different.

@Chandragupta @Deep2104

Thank you for such comprehensive answer

Hi ,

Can you please start a separate thread for this?

ONCE A DARLING, NOW AN EVIL

I am going to start this new series with all your love and wishes. Series “Once a darling, now an evil” is based on the companies which were once upon a time darling of the market and now, it has wiped out the majority of all those gains. I am trying to put some of the number-crunching facts by which we have identified ongoing issues in the companies and have saved our wealth.

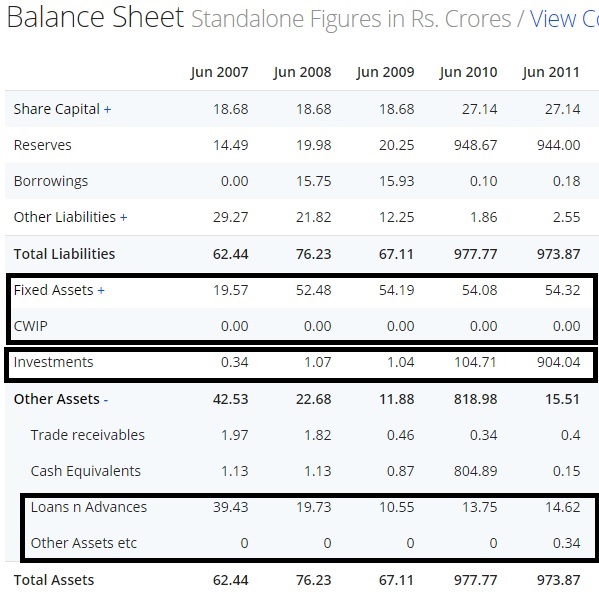

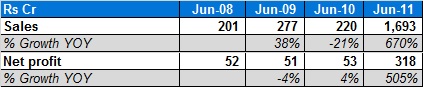

I am starting this part with one of the company which is engaged in providing Services Incidental to Onshore Oil Extraction which has an all-time high price of ~Rs.347 in 2008, ~Rs.308 in 2011 and now last traded price at Rs.0.42.

the company having huge sales and profit growth. Might be having something like a turnaround case or some Capex has started giving result.

But as usual, I get suspected on everything so as per habit I go deeper.

Wow…. What a wonderful company!!!

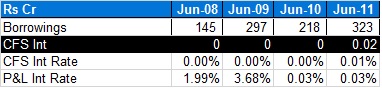

Company has taken a borrowing but does not have to pay any interest on it. I like it, I also get such a loan then can achieve many things with it. ![]()

Another point is, the company also need not pay any taxes. Wow… no interest and no tax.

Huge diversion between CFO and PAT but yes, positive and when looking at the FCF then its huge negative.

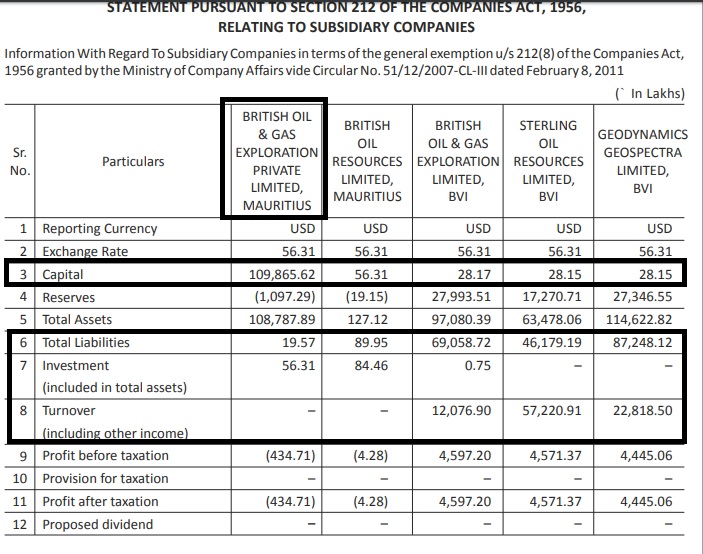

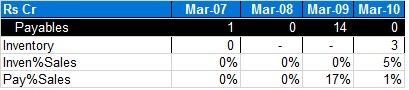

Now, more feather to add into it… need to compare consolidated and standalone balance sheet.

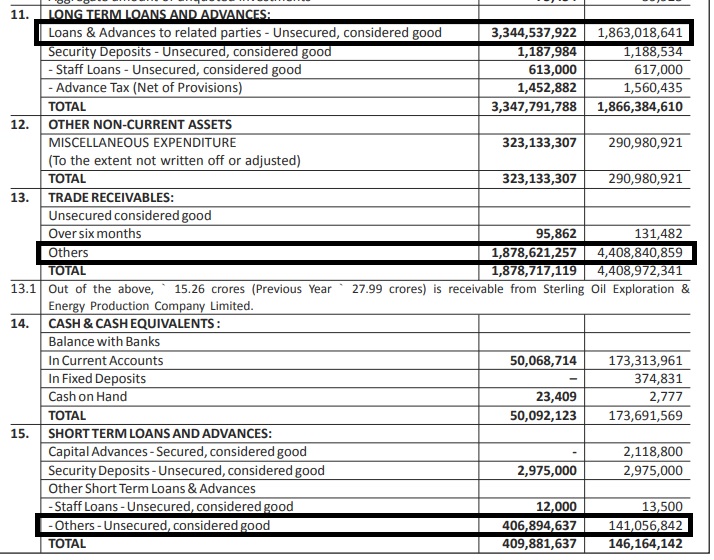

Here, when we see that company get ~Rs.800+ cr of cash in FY10 but that cash has gone out in FY11. So, where these much of cash gone? When we check the standalone balance sheet then that cash has gone as an investment.

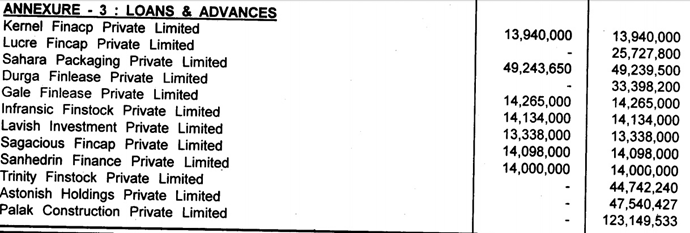

If we look at the few of the items of the balance sheet then we realize that the company has given a huge loan and advances to the related parties. Also, huge other receivable, what meant by others?

Disclosure – Companies mentioned in the article are just for an example & educational purpose. It is not a buy/sell/ hold recommendation.

please tell the name of the company also, so that i can go and take these data and learn.

This is very good analysis. Thank you for posting it

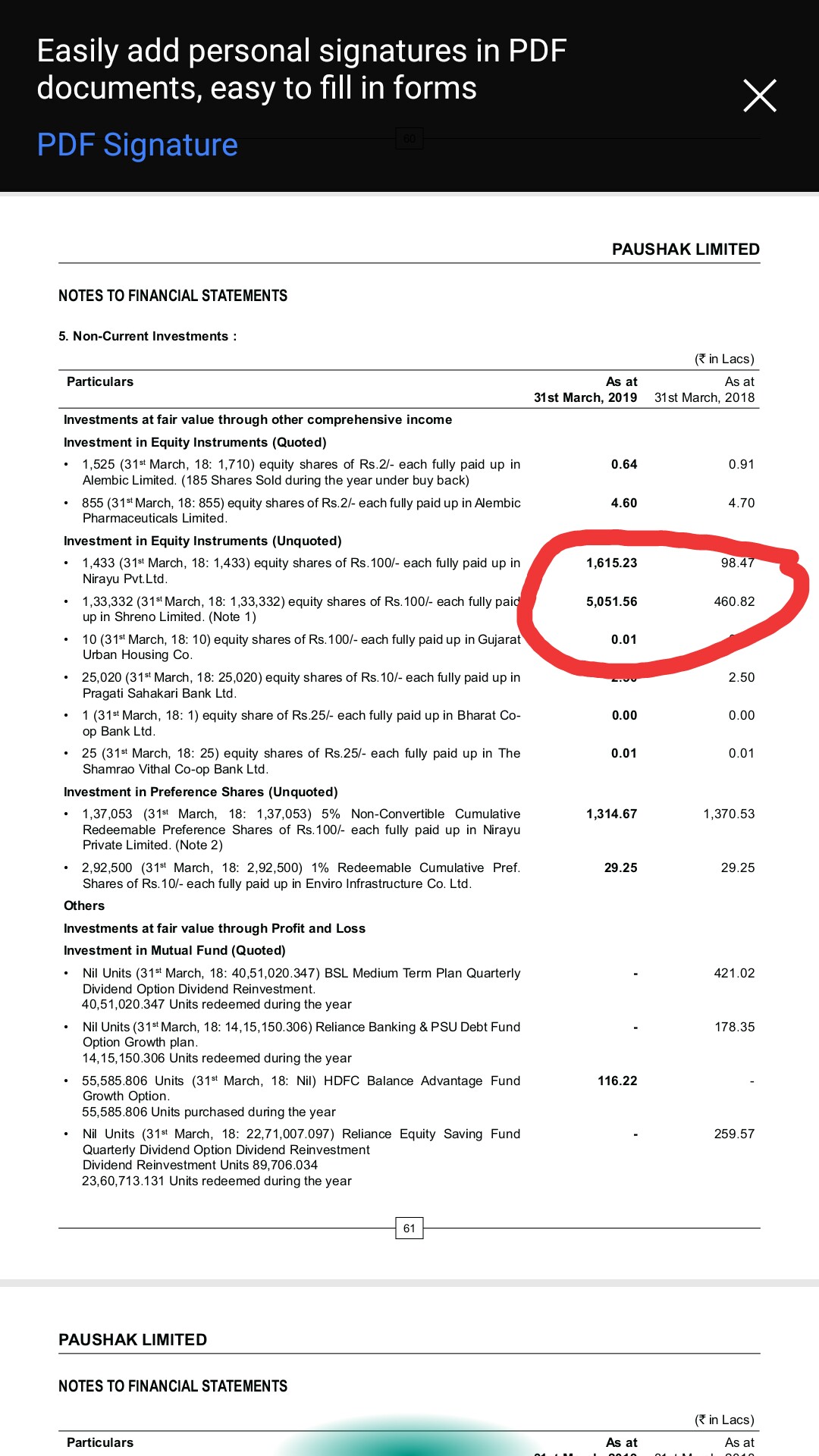

I have few querries about balance sheet of Paushak limited.

It is from Alembic group company.

1…Investment in their own group of company

Its ok that they (paushak)had invested in promoter’s group company but how their invested amount grows year on year on balance sheet

A—value of nirayu increases from 98.47 lkhs (2018) to 1615.23lkhs(2019)

B—Value of Shreno ltd increases from 460.82 lkhs(2018) to 5052.56lkhs(2019)

2……Why paushak’s cummulative cfo (10 years)is not matching with cummulative pat(10 years)

Cummulative pat=126 cr

Cummulative cfo=90cr

3……Receivable% is incresing in last few years

(In 2019 annual report

During the year, the Company has made changes in its Policy for receivables, payables and working

capital which resulted in lower Receivable days and higher current ratio.)

I am missing something or there is any red flag??

Seniors kindly give your opinion

Thanks

I am starting this part with one of the agro commodity trading company which has an all-time high price of Rs.5500 and now last traded price at Rs.1.60. and high of Rs.506 and 364 in the year 2008 and 2010.

What a wonderful company!!! Look at the fixed assets turnover…

But some interesting data…

Another interesting data….

Without a payable and without keeping an inventory, company has achieved huge turnover. But only receivables are there….

(Data of FY07-08) This looks something susceptible…. ~10%+ advances of sales… and that reach to ~71% in FY10. Majority of the companies were investment and finance companies.

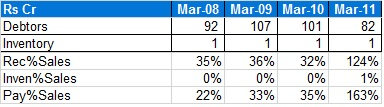

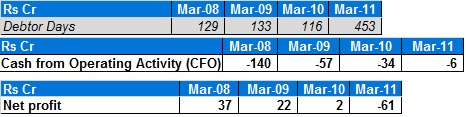

One other company which involve into the construction activities, which has an all-time high price of Rs.540 and now last traded price at Rs.0.30.

We can see that company is into the construction business but company does not have to keep any of the inventories.

Also, debtor days are growing and CFO is negative though company has reported net profit. Working capital is responsible for the negative CFO.

Advances recoverable is ~45% of balance sheet size in FY2010 and ~43% in FY2009. Also, company has contingent liability of ~Rs.725 cr which is ~96% of entire balance sheet size, 2.27x of sales and 319x of net profit in FY10.

Disclosure – Companies mentioned in the article are just for an example & educational purpose. It is not a buy/sell/ hold recommendation.

I was wondering if anyone has a view on this, specially any of the seniors. Looks like the company gave very good performance in 2019FY. Do we have any idea about any red-flags in this company (Apart from some promoters hiding as public shareholders)?

Recently a famous person running PMS services and well renowned for unearthing various corporate governance issues of many corporate, came with his views on recent run in pharma specially small / mid cap pharma, which has seen good run after going through dull period of 4-5 years.

He has used a name as well in his views. The name used has almost 2 decade old known issues and many other allegations / speculations by various section of investors / financial investigators.

Now we have a situation where retail investors must trust the person, as he has good track record in related field or evaluate the situation based on facts and take their investment decision

I wish to put certain facts to the audience and draw their feedback against each of them

The company had negative FCF during capex phase and recently started generating positive FCF. They have planned upcoming capex requirements wit their internal accruals

The company had rumours of promoter stake sale but promoters didn’t use legally approved money offloading their stake & used part of buyback to ensure they don’t reduce their stake unnecessarily. They brought next gen promoters in recent concall & everyone was impressed with knowledge / information possessed by young promoter.

The company used to pay dividend even when they had huge debt & investor community understood it as a way chosen by promoter to handle the pledged shares. Now pledge is almost nil, company still pays the same dividend

The company used to pay huge sum as remuneration to its promoters. Although that was always under legal limits but considering negative FCF / lower PAT etc, investors didn’t like it. Now with increased turnover / PAT, its getting addressed.

The company has US subsidiary, whose accounts are not audited. It contributed around 11% in recent quarter. Investor community feels that there could be a possibility of double accounting

If we have more points related to the issue, let us put together & scan through to get the facts for safe & secure investment.

Hi

I have been going thru the thread.

at times, name are not being highlighted, it becomes difficult for someone like me to understand the complete matter & do a due diligence my self as well.

Please mention name of company,if permissible

Amit Mantri talking about Granules

That is normal isn’t it?

The point made has two statements. Both aren’t related to each other. The second part has no relevance in corporate governance issue. As for the first part - if the company used buyback then how can the promoters be reducing stake - unless they’re offloading it in buyback. The bigger question is - if the company is so debt laden, how can it do buyback?

I don’t get how paying dividends is related to handling pledged shares. Dividend are a way to generate less taxing income (for the promoters or big investors) - why would it related to pledged shares?

I do not get why all those analyst make such hue and cry about huge promoter remuneration. Better they are paid legally rather than them taking it under the table. If anyone tries to set up any business in India, it’s like moving a mountain. Making random (less) promoter remuneration guidelines makes no sense.

Without knowing the name of the company, and seeing the accounts, can’t say anything about it.

news share as The nine accounts ED sought to freeze were: J K Tyre & Industries; Hamilton Housewares Pvt Ltd; K P Shangvi and sons; Nancy Krafts Pvt Ltd; Eastman Industries Ltd; Orbit Exports Ltd; Bharat Fashions and Apparels; Sheenuj & Co and RSWM Limited

complete News :