Thanks for the update. Will check

Mgt were conservative earlier even though 100% of loans are secured and LTV is low as loan book is full of new to credit borrowers.

As the book goes throught seasons, they are planning to get aggressive in using leverage to boost their ROE profile.

Rohit, Its a great coverage and thesis. Well articulated. Am new to value investing and learning. I have a question on the valuation. Given company’s 35% growth projection, how to determine current (under/overvalued) and projected target price. My rough calc, at a conservative 30% yoy, considering industry PE 30, it should reach close to 1700. Is that right way to project a NBFC!!!

That’s a good question & to be honest your guess is as good as mine in terms of what is the exact NPV of Five-Star business finance. That is as far as valuation goes.

As far as pricing goes - I think this goes back to the age old debate of should financials be “priced” at P/B or P/E. There are some who argue that P/B if there will be constant equity dilution, and P/E only if no plans to dilute (like Gruh back in the day) It could be argued Five-Star falls in the latter (Gruh finance) category.

Five- Star has stated in the October earnings call (if i am not mistaken), that they ideally should not need to raise capital (maybe ever, if not at least for the next 5 years) If you look at their CAR it is greater than 50% and they have high return ratios RoA (8%+ now should come down to 6.5% steady state in the next few years). So they should be able to finance growth for at least the next 5-6 years (may be more) through internal accruals while maintaining a max leverage ratio of 4x (current leverage little above 2x)

So if we assume P/E is the right metric and just crudely straight line their earnings at 35% (which is their stated guidance) 3 years out. They should conservatively be around 2,000 cr PAT. (They are currently close to 900-1,000 cr PAT annualizing last quarter’s number) Assign whatever P/E multiple you choose (based on growth expectation then & RoE at 4x leverage) & you will get your target market cap 3 years out. (current market cap 22,500 cr)

It must be said that the above calculation is extremely crude and i am sure flawed in many ways ![]() but it’s made just to illustrate a larger point.

but it’s made just to illustrate a larger point.

2 Likes

Very good pointers. Thank you!!

I always had this question for rapidly growing Banks/NBFCs: why use P/B at all? It is more of a “present” metric rather than something that takes into account the future.

And instead of PE, use it growth in AUM + sales (something similar like PEG) to get a better sense of the value that they would generate for us shareholders.

Disclosure : Invested

3 Likes

For your first question, based on my understanding, Book Value gives an understanding of how much capital does the entity have. In cases of financial institutions, it gives an idea of how much they can lend (I think RBI gives the definition of how much leverage one can do based on the book value).

So as book value increases the entity can get more leverage and accordingly lend more. This brings in more volume lead yield.

In some sense, AUM growth is also linked to the book value as well as the equity. Since equity is part of what is being lent.

So, if we know the rate at which the AUM grows or book value (ROA) is growing, we can understand how much more leverage is possible in future. So you’ll see expected P/B forcast being done.

An eg: If current P/B is 2 but historically the entity traded at P/B of 3 we can say (after more analysis on P/E, ROA, etc) that the firm maybe undervalued.

Hope I clarified your doubt. Also, please correct me if I’m wrong. I’ve just started learning the finance sector.

Cheers

1 Like

Compared to peers Fivestar has a very low debt to eq ratio of just 1.22

Larger peers have significantly higher debt to eq ratio at… Bajfin(3.8), Chola(6.8), Shriram(3.9), Hdfcb(7.4), Sbi(13.5), BoBaroda(12.1).

From a risk perspective is this a good thing ?

1 Like

Have started preliminary research on Five Star Business Finance.

A question I had is that how are they able to capture such high NIM’S at roughly 17%, which are almost twice of what peers like Fedfina and SBFC are able to get and in fact higher than most microfinance companies.

Any major differentiator in the business model per se?

Thanks.

1 Like

secured lending (loan against properties), where as, most micro-finance is unsecured which leads to higher cost of funds due to higher risks for the company.

1 Like

FedFina is primarily a gold loan company and the LAP that they do is of a much higher ATS than Five Star. Their target is much different that Five Star. These companies are not comparable at all.

1 Like

The NIMs are elevated due to lower leverage.

They give fixed loans at~21-24%, but since interest expense is very less, it seems like High NIMs.

3 Likes

A few points here.

SBFC Finance does 98% secured lending, yet their NIM’s are ~10%. Fedfina does 85% secured lending with NIM’s at 8%. Cost of funds for microfinance companies are in the range of 11-12%, whereas for Five-star Finance, it is 9.7%, so the disproportionately higher NIM’s are not due to lower cost of funds.

1 Like

Fedfina has a Mortgage AUM of roughly 6200 crores, ticket size of INR 22 lakh and yields of ~14%.

Five-star has an AUM of 9600 crores and almost 90% of the loans are sub INR 5 lakh with yields of 24%.

I presume the huge difference in yields is largely due to the nature of loans, wherein Five-star gives loans to small business owners.

However, my thought was that given the secured nature of the loans, their yields should have been much lower. At 24% yields, they are on par with microfinance companies, whose book is completely unsecured.

2 Likes

Some part due to lower cost of funds, some part due to lower leverage and some part due to high yields (~24%). They have been saying they will pass on recent lower cost of funds advantages to customers once predictability with (rising) interest rates increases.

Their incremental and overall cost of funds decreased even during rising interest rate environment.

And, from here on they will try to increase leverage as well, again statements made in concall. Spreads as well as NIMs should decrease going forward. Guiding for no further equity dilution for next 3-5 years.

And, I have not studied fedfina and sbfc. My takeaways for micro finance are from bandhan, asirvad micro finance, etc

Not invested.

The relatively higher yields could be due to:

- Individual loans vs group loans where there is collective accountability and scale leading to larger disbursement hence rates are lower.

- Longer duration of the loan and keeping EMIs to smaller amounts.

- Focus on Tier-4 and below markets.

1 Like

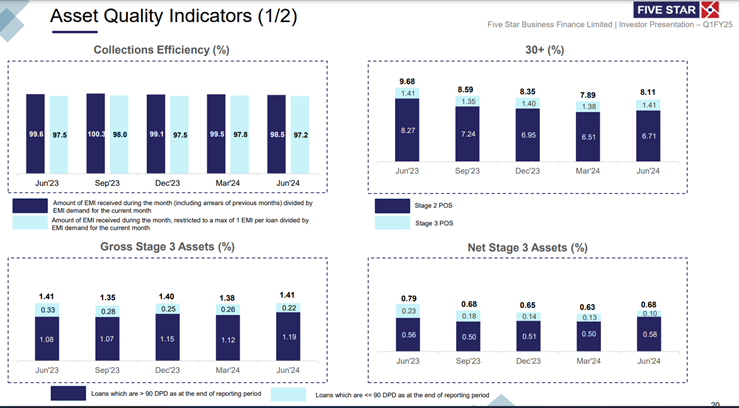

Good set of results from Five Star. Consistent growth stable asset quality.

Only worry is a large % of the book is unseasoned.

Lag asset quality numbers are encouraging though (when looked at wrt yields)

Investor-Presentation-for-the-quarter-ended-June-2024.pdf (1.7 MB)

1 Like

Do you think this company will be re-rated at P/B of 5-6x considering the high growth, pristine asset quality & RoE touching 20%?

Disc - Invested

1 Like

Promoters infusing ~32 Cr at a price of Rs. 770 at a time when everyone is doing so at a 25% discount. Good signal from the management.

3 Likes

Great set of numbers for the quarter gone by.

Investment thesis in 1 line - MFI spreads with Housing finance type risk/security & NPAs.

The damper is the forward guidance for the next 2 quarters. Not sure why the market reacted so negatively. There is at least so far very little stress on Five Star’s book. And exercising Temporary caution at a time of elevated consumer leverage is just being responsible. I don’t see how the terminal value of the company goes down by 13% because of it ![]()

Disclosure - Invested.

3 Likes