The reaction started due to management commentary. Moreover lending rates were reduced by 2 percent from Nov. So obviously profit will be affected adversely. Market was already jittery regarding MFI stocks and management commentary was trigger to hammer it. Present market mood is very severe for any negatives due to panick.

1 Like

The asset quality trends are not so promising either. There is lot of stress across the board on retail assets as most customers are over leveraged. A cautious stance here might not be unwarranted.

By asset quality trends, are you referring to Five Star or sectors as whole?

Regards,

Ashutosh

Disclosure : Invested

Both, expect some more deterioration before things stabilize here. The forced slow down and moderation of interest rates might help them out. The company has exhibited strong disciplined execution so far and hope the same continues.

1 Like

Two back to back resignation by Key management personnel that were leading Compliance & Audit deptt respectively. Whats brewing here?

4 Likes

@imran_ahmad one of the attachments above is that of CMS.

Five Star Business finance -

Q4 and FY 25 results and concall highlights -

FY 25 outcomes -

No of branches @ 748 as on 31 Mar 25 vs 520 as on 31 Mar 24

AUM @ 11.87 k cr, up 23 pc

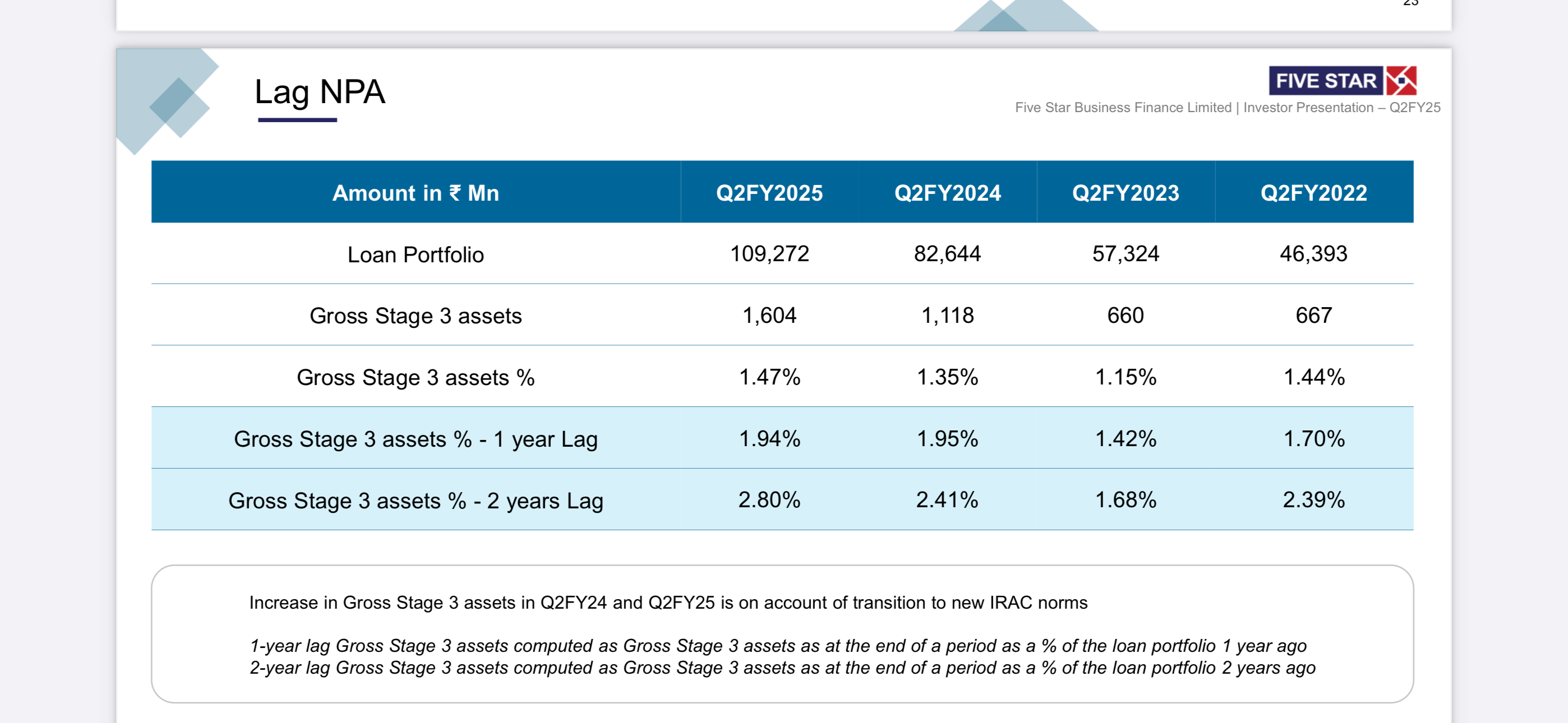

Gross NPAs @ 1.79 vs 1.38 pc

Net NPAs @ 0.88 vs 0.63 pc

PCR @ 51.31 vs 54.27 pc

Capital Adequacy @ 50.10 pc !!!

30 DPD + @ 9.65 vs 7.9 pc YoY ( includes 90 DPD + @ 1.79 pc )

PAT - 1072 cr, up 28 pc

NIMs @ 16.75 pc

RoA @ 8.18 pc

RoE @ 18.9 vs 17.8 pc YoY

Company is present across 11 states and UTs

100 pc of company’s loan book is secured. 95 pc is against self owned residential property

Avg ticket size @ 3.9 lakh. LTV @ 40 pc - indicating conservative lending practices

Restructured book @ 0.30 pc. Holding 45 pc provisions on restructured book

Active loans as on 31 Mar 25 @ 46 vs 39 lakh YoY

Company added 19 branches in Q4

Total employee count @ 11934 vs 9327 as on 31 Mar 24

**FY 25’s cost of borrowing @ 9.64 vs 9.71 pc **

**Portfolio yeild @ 24.03 vs 24.27 pc **

Spreads @ 14.39 pc

Geography wise breakup of AUM -

TN - 29 pc

AP - 38 pc

Telangana - 19 pc

Karnataka - 6 pc

MP - 7 pc

Others - 2 pc

Tier wise breakup of AUM -

Tier - 1 and 2 - 1 pc

Tier - 3 - 8 pc

Tier - 4 - 14 pc

Tier - 5 - 32 pc

Tier - 6 - 45 pc

AUM breakup by ticket size -

< 3 Lakh - 32 pc

3-5 Lakh - 53 pc

5-10 Lakh - 13 pc

10-15 Lakh - 1 pc

AUM breakup by vintage -

Less than 1 yr - 39 pc

1-3 yr - 48 pc

3-5 yr - 8 pc

More than 5 yr - 5 pc

Trend of 30 DPD + over last 5 Qtrs -

Mar 24 @ 7.89 pc

Jun 24 @ 8.11 pc

Sep 24 @ 8.44 pc

Dec 24 @ 9.16 pc

Mar 25 @ 9.65 pc

Trend of 30 DPD + over last 5 yrs -

Mar 20 - 11.82 pc

Mar 21 - 12.36 pc

Mar 22 - 16.78 pc

Mar 23 - 10.5 pc

Mar 24 - 7.89 pc

Mar 25 - 9.65 pc

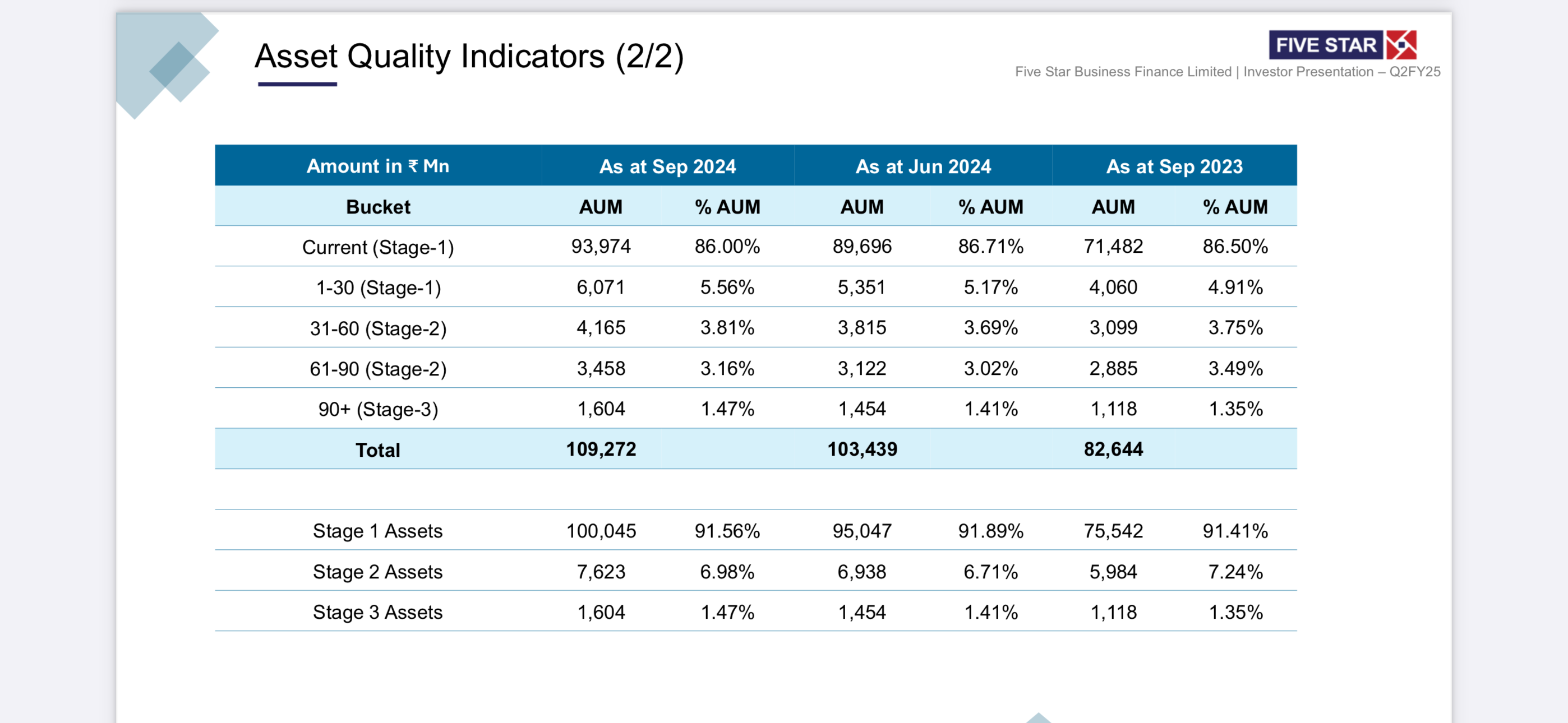

Stage wise breakup of current AUM -

Current ( stage 1 ) - 10009 cr @ 84.92 pc of AUM

1-30 DPD ( stage 1 ) - 720 cr @ 6.07 pc of AUM

Total stage 1 @ 10730 cr

31 - 60 DPD ( stage 2 ) - 487 cr @ 4.1 pc of AUM

61 - 90 DPD ( stage 2 ) - 446 cr @ 3.76 pc of AUM

Total stage 2 @ 934 cr @ 7.87 pc of AUM

90 DPD + ( stage 3 ) - 212 cr @ 1.79 pc of AUM

Total provisions @ 194 cr ( out of which 85 cr are against stage 1 + 2 assets, 109 cr are against stage 3 loans )

Q4 P&L statement -

Interest Income - 734 vs 599 cr, up 23 pc

Fee and Other inc - 25 vs 19 cr

Interest expenses - 175 vs 138 cr, up 27 pc

NII - 584 vs 481 cr, up 21 pc

Operating expenses - 188 vs 149 cr, up 26 pc

Provisions + loan losses - 25 vs 19 cr

PAT - 277 vs 236 cr, up 18 pc

FY 25 P&L statement -

Interest Income - 2766 vs 2116 cr, up 31 pc

Fee and Other income - 100 vs 79 cr

Interest expenses - 668 vs 468 cr, up 43 pc

NII - 2198 vs 1726 cr, up 27 pc

Operating expenses - 678 vs 555 cr, up 22 pc

( yearly operating expenses @ 5.74 pc of AUM )

Provisions + loan losses - 89 vs 56 cr

PAT - 1069 vs 834 cr, up 28 pc

Comments from Q4 concall -

If the disruption in Karnataka had not happened in Q4, company would have grown its AUM by 25 pc ( instead of reported growth of 23 pc ). The bump up in gross NPAs to 1.79 is also partially attributable to the new Bill passed in Karnataka assembly. Things have now started to improve

Distributed a dividend of Rs 2 / share for FY 25

Massive branch addition in FY 25 is mainly due to split up of bigger branches into smaller branches to improve coverage and efficiencies with minimal additional expenses

Cost of incremental borrowings has fallen further to 9.3 pc

As the interest rates keep falling, credit demand should pick up further

The over leveraging by retail customers ( specially lower income groups - which are company’s customers ) - also played a role in worsening of credit quality through FY 25. The same is now getting reversed. Should take another 2 Qtrs for situation to normalise completely

Still the company is much better off vs MFIs as their nature of lending is 100 pc secured. Customer behaviour is completely different while dealing with Five Star finance vs MFIs as the company holds their residential property as collateral

Should be able to grow their AUM by another 25 pc in FY 26

Similar bill has now been passed in TN. But the disruption levels in TN are far lower and the situation is completely under control

Should see a sizeable drop in cost of funds ( 20-40 bps ) both on the existing borrowings and on incremental borrowings as the RBI has started cutting rates and the banks have also stared passing on the cuts

Company believes that a PCR of 1.65 pc of AUM ( 194 cr of provisions on a loan book of 11.8 k cr ) is more than adequate for a 100 pc secured loan book

Company is deliberately trying to lend more in 3-5 and 5-10 lakh ticket size bracket. They believe, the stress in this segment of customers is far lesser vs the customers with loan size < 3 lakh. Also as the cost of borrowing is falling and the company is also willing to lending at lower rates, the profile of customers that the company is getting ( incrementally ) is also improving. These ( supposedly ) better customers generally have ticket sizes > 3 lakh

Out of 228 branches added in FY 25, 150 branches were added because of split up of bigger branches. Any branch servicing > 1500 customers, company is happy to split it. Most of branch splitting is behind. As and when reaches > 1500 customers, company shall keep splitting them. New branches + Splitting combined - should be able to add 75-100 / yr going forward

Aim to bring the < 3 lakh ticket size loans down to 20 pc of AUM from 32 pc currently. There shall be a corresponding 12 pc gain in the 3-5 lakh + 5-10 lakh ticket size books ( combined ). Primary focus shall be on the 3-5 lakh bracket - that’s their sweet spot

Because of stress in the system wrt retail lending to low income customers, the MFIs have sharply pulled back their lending over last 2 Qtrs. The over indebtedness at retail level is now getting abating on a QoQ basis - this augurs well for the Industry. Also the cash flows in Rural India are showing descent signs of recovery

Looking to get into affordable housing segment - as it’s an adjacent product for the company. Should start rolling it out wef Q3/Q4 FY 26

Company aspires per employee AUM to be around 1.25 cr

In Q4, Avg new loan disbursements per employee per month was 2.6 loans / employee / month which corresponds to aprox 31 loans / employee / Yr

Company’s avg customer has a CIBIL score profile of 500-550 or is completely new to credit vs bigger NBFC’s / Banks which lend to customers with CIBIL score > 700

For the incremental loans, company is lending @ rates between 21.5 - 23 pc with an avg yeild of about 22.5 pc - which is aprox 150 - 200 bps lower than their previous lending rates ( basically they are now passing on the reduced rates to the customers ). This drop is yeild is also attracting better customers for the company

Expansion in employee count should moderate going forward as company intends to now ramp up AUM per employee

Expecting growth rates in TN and Karnataka to pick up wef Q1 FY 26 ( should be closer to 30 pc growth in these 2 states )

Intend to keep paying dividends every year from now on

State wise spread of branches -

TN - 208

Karnataka - 59

AP - 234

Telangana - 115

Maharashtra - 25

MP - 94

Gujarat - 1

Rajasthan - 5

UP - 6

Chattishgarh - 3

When company enters a new state, they open a small number of branches ( < 5-6 branches ) and study the mkt closely for 18-24 months. Only once they r confident, they then ramp up quickly

FY 26, earnings growth should be moderate at 12-15 pc despite 25 pc AUM growth because the company is now lending ( wef Nov 24 ) @ 200 BPS lower than their historical lending rates. RoA should be between 7.5 - 8 pc

End use of company’s loans include - Business loans ( 60 pc of loans ), construction related expenses ( 20 pc of loans ) , personal consumption like medial, educational etc ( 15 pc of loans )

Disc: hold a tracking position, studying, not a buy/sell recommendation, biased, not SEBI registered, posted for educational purposes

2 Likes

Five Star business finance -

Q1 FY 26 results and Concall highlights -

No of branches - 767, opened 19 new branches in Q1

Loan disbursement - 1290 cr, down 2 pc YoY

AUM - 12,457 cr, up 20 pc YoY

30 + DPD @ 11.31 ( up 3.2 pc YoY, 1.66 pc QoQ - indicating increased stress in the loan book )

Cost income stood @ 41.34 vs 34.34 pc YoY ( including credit cost ). Excluding credit cost, Cost / Income stood @ 33.45 vs 30.73 pc YoY

GNPAs ( 90 + DPD ) @ 2.46 pc vs 1.41 pc YoY

NNPAs @ 1.25 vs 0.68 pc YoY

Loan book is 100 pc secured - 95 pc of it is secured against self owned residential property. Avg portfolio LTV @ 39 pc ( indicating conservative lending practices )

Interest income @ 791 vs 669 cr, up 18 pc

Interest expenses @ 187 vs 158 cr, up 18 pc

Other expenses @ 201 vs 156 cr, up 29 pc

Credit cost @ 47 vs 18 cr, up 158 pc

PAT @ 266 vs 251 cr, up 6 pc YoY

Avg portfolio yeild @ 23.51

Avg cost of borrowing @ 9.54

Avg portfolio spreads @ 13.97

NIMs @ 16.43

RoA @ 7.24

RoE @ 16.57

AUM by geography -

TN - 28 pc

AP - 37 pc

Telangana - 19 pc

Karnataka - 6 pc

MP - 7 pc

Others - 2 pc

AUM by ticket size -

< 3 lakh @ 31 vs 35 pc YoY

3-5 lakh @ 53 vs 52 pc YoY

5 -10 lakh @ 15 vs 11 pc YoY

Above 10 lakh @ 1 vs NIL YoY

Management commentary -

Over-leveraging in the retail segment led by indiscriminate lending by MFIs, other NBFCs is the main cause of stress in the system

Management has deliberately slowed down lending in riskier segments, areas, colonies and in general for tick sizes < 3 lakh ( where the stress is more ). 3-5 lakh tick size bucket’s behaviour is much better. 5-10 lakh bucket is what the company is replacing the < 3 lakh bucket with

Closely monitoring customers debt profile before sanctioning loans. However, a lot of customers have over leveraged themselves post taking loans from Five Star - which is also another major reason for stress. To counter this, company is now focussing on financially literate / conservative customers who won’t over leverage themselves in times of easy liquidity

Seeing early signs of improvement as a lot of MFIs have taken the hits on their P&L accounts wrt bad loans. This should ease up the situation for lenders like Five Star ( since they hold customer’s residential properties as collateral )

Company’s July month’s collections have been much better than what was seen Apr, May, June - a key positive

Most of the pain should be over by end of Q2. Hence the company is not revising its full year AUM growth guidance of 20 pc + and 12-15 pc PAT growth

Credit cost guidance @ 1.2 - 1.25 pc for full FY

Because of secured nature of their loans, they should be the first to bounce back as the lending environment improves

New branch opening + splitting of branches continues as before

Disbursements and AUM growth moderated due to tough lending environment at present

No fresh over leverage is being created by the MFI players in the market ( as they too have turned cautious - for obvious reasons ) - a great thing to be happening for the sector

Q2 credit cost is not expected to be higher than Q1 ( most likely, should be marginally lower ). Credit cost should start tapering off wef Q3

Historically, 10-15 pc of loans flow down from 30+ DPD to 90+ DPD

Company has 100 advocates on its pay rolls - as a part of recovery team. LY, company recovered an avg of 12-14 cr / Qtr from NPA accounts ( written down ). This year, company hopes to recover an avg of aprox 18 cr / Qtr

Collections in Karnataka are bouncing back nicely. Once collections stabilise at higher levels, will the company start focusing on disbursements in Karnataka again

TN and Telangana are doing much better than the company avg wrt NPAs / slippages

Since the company began its operations ( over 2 decades ago ) they have hardly ever lost their principal ( because of secured nature of lending )

Disc: holding a tracking position, will add only when the stress starts to abate, not SEBI registered, not a buy/sell recommendation

4 Likes

I have started reading about the Five star business due to the recent fall after the Stress in the books and CEO resignation.

Can someone please clarify my points mentioned below:

-

The company is operating in Tier 5-6 areas therefore the operating cost to income is low as compared to the peers or just the fact that the efficiency in operation are high?

-

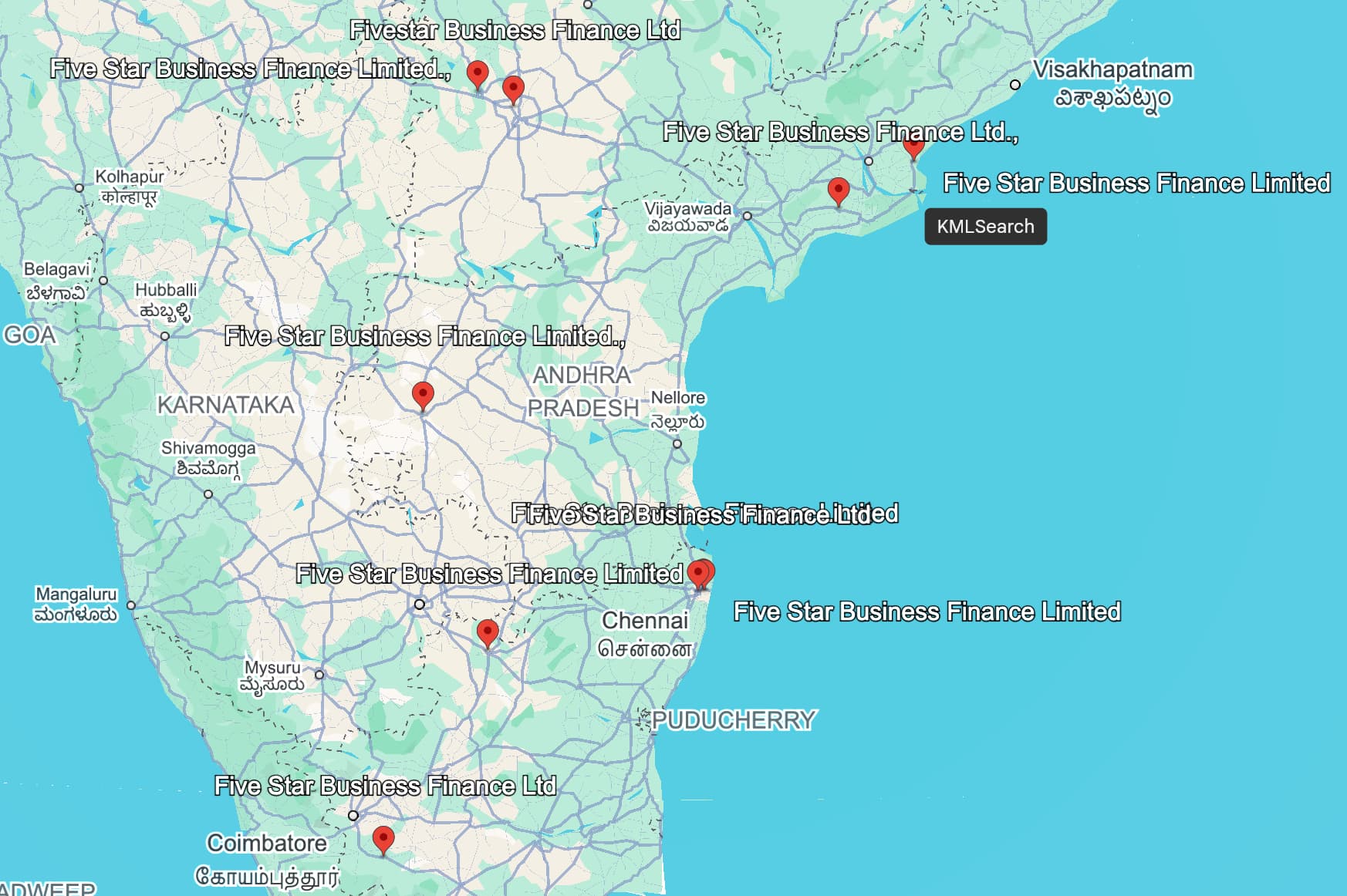

I have checked the Google earth for the Five star locations as they are expanding 50-60 branches per year but not even 10% of the Branches are under the Google Location marker although I understand that Locating the Branches in Rural area is easy so it might be the reason of not registering under Google location

-

I have also checked the reviews of the given Location but the average rating is as low as 3 stars.

When they say operating in low tier, that doesn’t main branches are in such a place. Branches will still be in some City or district headquarters, but they do source loan from the rural areas. Catchment area of branch sometimes even go 50-60 km from the branch. This is how all NBFCs work, none of them will actually have physical branch in a village

Google maps does not show all results at once, if you zoom further and search again, some more results will appear

Yeah aboslutely correct, they also have Business Correspondents (BCs) which pass on leads from lower tier areas to the regional branches.

Investor-Presentation-Q3-FY-2026.pdf (1.9 MB)

Five-Star put up a fairly dismal quarter, and I’m struggling to see why management felt comfortable reiterating 25% full-year growth guidance in the previous call. That optimism now looks… ambitious.

Asset quality isn’t helping the story either. With 30+ DPD creeping close to 13%, management has simultaneously lowered the provision coverage ratio from 45% to below 40%. If I normalize for this, both PBT and PAT would have actually declined ~6% YoY — which is not quite the growth narrative we were sold.

Five-Star was originally built on a deep, “doorstep” understanding of the sub-₹3 lakh customer — a niche no one else really cracked. But as the company moves up to the ₹3–10 lakh segment, where every bank and NBFC already plays, I find it hard to see what their unique edge is or why they should win here.

All that said, management insists this is the trough and that things turn around by the end of this fiscal year. For now, I’ll take them at their word — and keep my fingers crossed. Overall though, pretty disappointed.

2 Likes