Incorporated in 1984 by Mr VK Ranganathan, Five Star Business Finance in its previous avatar was mostly a “me too” local low ticket auto/secured lending financier around Chennai. In 2002 his son in law, Mr LakshmiPathy Deenadayalan (Pathy) took over the reins of the company and transformed it into the business finance company it is today. In 2002, Five star finance’s portfolio mainly comprised of 2/3 wheeler & consumer goods financing with high NPA’s and no significant advantage over the more established players in the region. Pathy realized that this was not sustainable and spent the next 8-10 years trying, testing & perfecting a new business model moving away from conventional auto (2/3 Wheel ) finance to a business finance company. Five star business Finance (FSBF) currently is a non-deposit taking NBFC (used to be a deposit taking NBFC, surrendered the license) providing secured business loans to micro-entrepreneurs and self-employed individuals, each of whom are largely excluded by traditional financing institutions. Over 95% of the loan portfolio comprises loans with ticket sizes varying between ₹0.1 million to ₹1.0 million, with the median ticket size being between 3-5 lakhs and an average tenure of 5-7 years.

In simple words, FSBF offers business loans to micro/small entrepreneurs (think small shop keepers, mechanic shops, hardware traders, welding job / work units etc.) in tier 3 – tier 7 cities. These businesses are largely unbanked and are excluded from most formal sources of financing. The only option these Micro entrepreneurs have is the local money lender (FSBF’s main competitor apart from a few small firms CSL etc.), and therefore these customers to a large extent are not very price sensitive (Read high yields 22-24% and therefore wide spreads 12-13%)

This is different from a microfinance institution in 2 important ways. Firstly the lending is asset backed & secondly loans are made to individuals instead of SHG (self-help groups) etc. The main collateral for these loans is a self-occupied (Pakka) house, with an RCC foundation.

Additionally, a rising interest rate environment does not have a significant impact on FSBF’s business, firstly because of the wide spreads (low customer price sensitivity), and secondly as they grow & season their asset book and establish more credibility in their business model, the higher their credit rating gets and therefore the lower their cost of funds in the commercial debt markets, as evidenced by their declining overall cost of funds in the past 2 years despite a rising interest rate cycle.

In 2014, FSBF stepped on the growth pedal after perfecting its lending model, by raising private equity capital, professionalizing the management structure & investing in strong IT systems so that the company could grow at a faster clip & orchestrate their operations at scale.

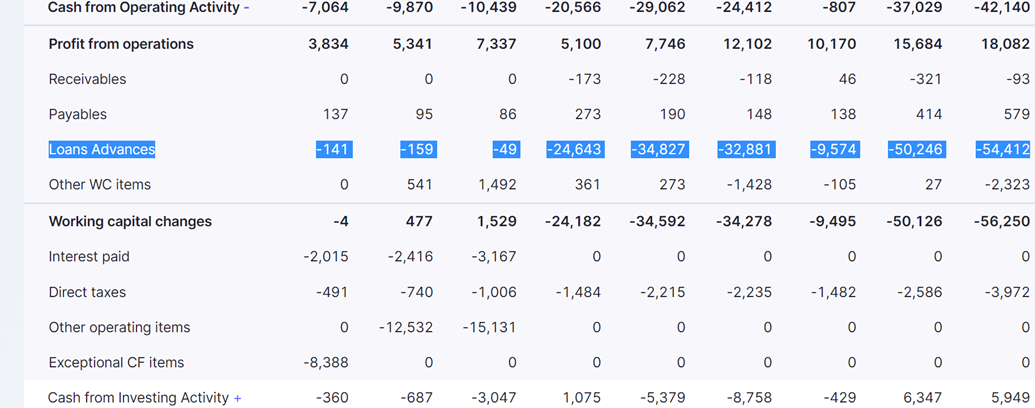

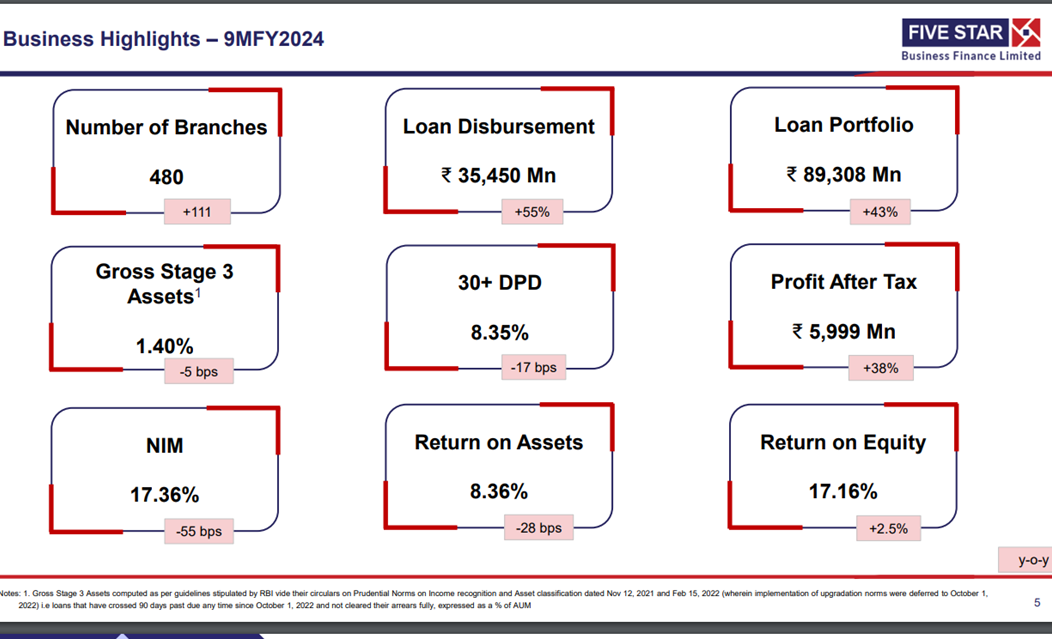

Growth – Since 2017 the company has grown its top line 15x, Grown its book 12x and PAT 23x. All this while maintaining a reasonable asset quality with an average GNPA 1.5% and NNPA 1% (excluding temporary shocks such as Demon, Covid, GST implementation etc.)

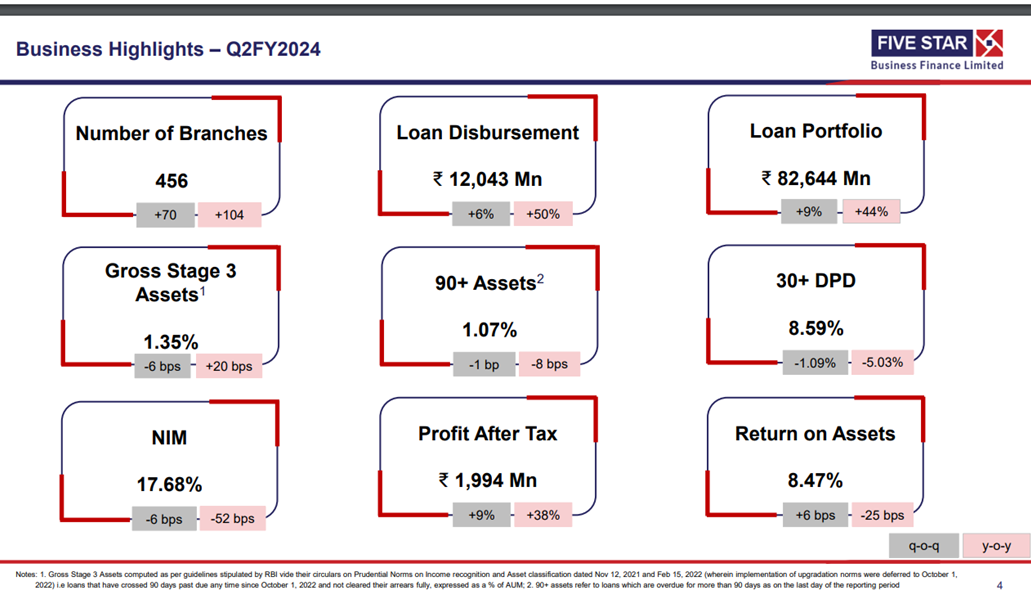

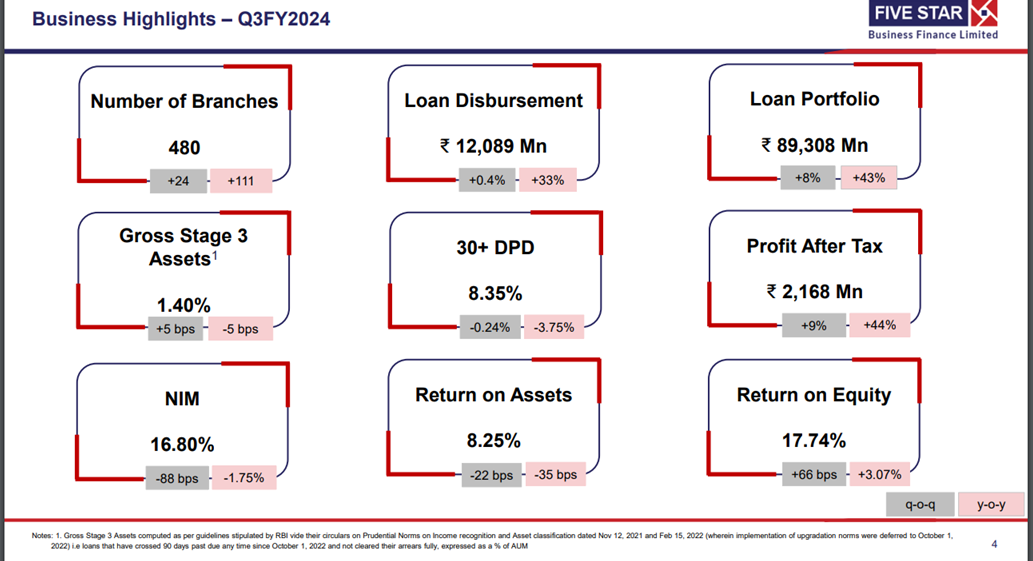

There is a lot more one can write about their personnel strategy, their cluster-based growth strategy etc. The mechanics of how they keep their asset quality the way it is etc. But in the interest of keeping this short (and not a 70-page report ![]() ) so as to introduce this company to the VP community, I have chosen not to get too deep in the weeds in this first post. The important data points have been captured in the table above. Additionally, I have curated a set of informative videos (7+ hours of video) below, for those interested in gaining a significantly deeper understanding of the business.

) so as to introduce this company to the VP community, I have chosen not to get too deep in the weeds in this first post. The important data points have been captured in the table above. Additionally, I have curated a set of informative videos (7+ hours of video) below, for those interested in gaining a significantly deeper understanding of the business.

Key Risks -

-

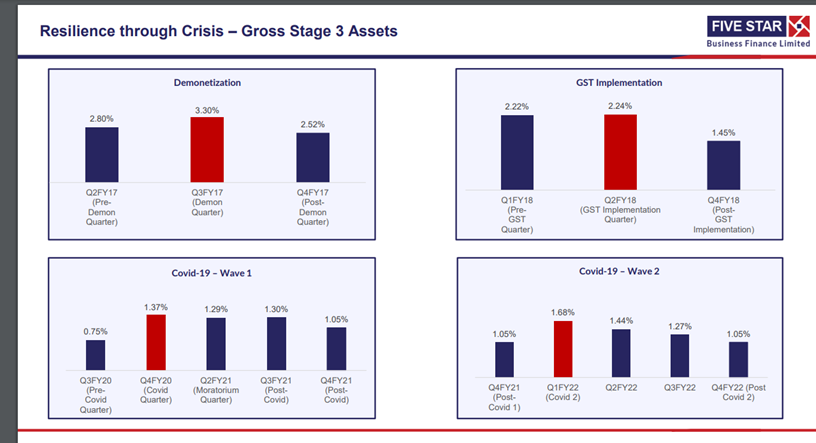

Five star’s business model is heavily labor dependent. Unlike other NBFC’s which employ large data sets, AI & ML etc. to arrive at a loan decision almost instantly, Five star can not do that because of the company’s customer profile. Five star’s customer rarely has any documented cash flows or sources of income. A five star employee therefore has to physically verify the customer’s cash flows & the nature (character) of the customer by spending a few days at the customer’s business, talking to neighbors, visiting the customers home etc. to make qualitative assessments such as, do they own a refrigerator at home, what’s the size of their TV, does the wife wear jewelry etc. to arrive at an evaluation of the living standards and thereby the income of a potential customer. This methodology is based on the principle that, if a person claims to have a certain income, then the 2 main areas that they will spend said income on is their own home and on their overall living standard. This high dependence on labor & their subjective opinion on a customers living standards and therefore the ability to repay is a big risk in their business model. Five star finance mitigates this risk in several ways. First - They do not silo the origination team and the collections team. By making the loan originator also responsible for collections ensures that there is minimal scope for corruption, further the employee’s variable compensation is tied to the repayment profile of the customers he/she brings in. Additionally they are trying to make this process of evaluating subjective living standards as objective as possible. For ex- if a customer claims to be earning 3 lakhs per year for 7-10 years, they should own assets / goods worth at least 3-4 lakhs, and these items have to be documented (This excludes all items obtained through inheritance, mainly the house). Lastly the ultimate risk mitigator is the collateral. Having the customer’s own, occupied home as collateral and getting reregistration done of the property helps minimize default risk, as evidenced by the low NPA numbers over the past 7 years despite a stupendous growth in their loan book & several macro and micro shocks.

-

Geographic concentration risk - Nearly 80% of Five Star’s business currently comes from the states of Tamil Nadu, Karnataka & erstwhile Andhra Pradesh. In order to mitigate this, they are trying to diversify the portfolio by entering the central Indian market but this will take time. Learning the local laws, customs, borrower profile, land record rules etc. and institutionalizing it takes 24 months (per management). So at least for the next 2-3 years a large portion of the book would be concentrated in the south.

In conclusion, Five Star business finance is basically a sub-prime LAP lender & is trying to disrupt the “money lender” / Loan Shark market in India. They have been able to execute extremely well thus far. They have grown their book by 50x in less than 7 years, have weathered the most serious shocks in the lending business (Covid / Demon) successfully and are on the cusp of a major geographic expansion. The company does not have any major “organized” competitor (There are several companies doing low ticket 8-12 lakh housing finance but none in the 3-5 Lakh business finance segment). In my opinion the company should do well in the coming positive macro cycle & does therefore deserve a closer look.

Significant Shareholders – Matrix Partners, TPG Capital, KKR (recently sold in the IPO) & Several others.

Disclosure: Invested. May increase/decrease allocation in the future, biased. Do your own due diligence before investing.

Reference Videos: