TTM Operating profit? Shouldn’t it be 80 cr considering 3 yr avg FCF

Valueable insights by community members on this company given the fact that company does not conduct conferrence call publicly which seems quite unusual from the company of this size. There have also been instances of promoters getting excess salary and company not contributing to providing credit reports inputs by Crisil.(Although very old some 2012 instance). Don’t know if this points to CG governance issue. Would request vpicker to enlighten on this.

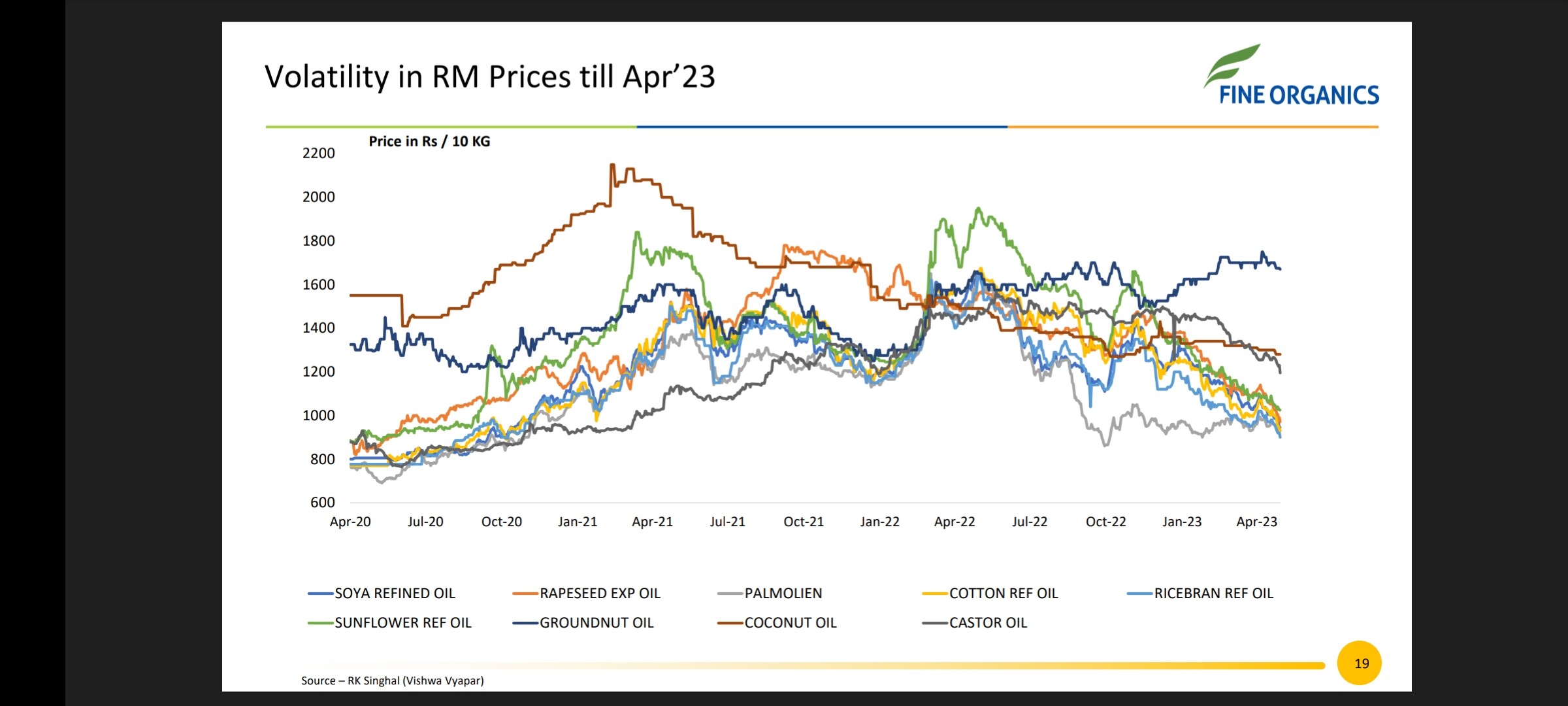

Now coming to the recent results posted by Co. It reports OPM of 34℅ which prima facie looked due to the high RM prices but except for groundnut Oil all the prices of key inputs are coming down. So there doesnt seem to be any correlation between key inputs prices and their OPM. I did not find any material information in this regard from Investor presentation report in terms of management commentary. IMO they should provide some sort of comments in the investor presentation atleast to gauge the company performance going forward.

Disc.- Views expressed are biased and could be wrong.

4 Likes

there is generally a lag between the RM price change and it reflecting in the P&L. Any reduction in prices will also mean that they may need to pass on the price benefits to end customers. So the OPM will have a lag effect and in my view the management will be able to manage the margins due to the product portfolio and companies standing with the customers in the market.

pertinent to note that for the Q4 FY23, their sales have dropped but profit has gone up and so have margins. My sense is that the change in RM prices would have happened some time back and whose effect would have seen in this qtr that beside the sales would have gone down due to Fine Organics passing on the benefits of lower prices to customers. So when RM prices go down, sale price also goes down. The management would have done a swell job in getting 30%+ margins since there was a lot of discussion on peak margins and whether they will be able to manage it. The stock prices came down from 7200 to 4000.

6 Likes

Hi,

I am not able to understand why has the PE gone down consistently since the last year - from 80x to 23x currently. The profit margin has improved. Is it because the quarterly Sales have been going down for last 2 quarters? Where do we see the prices going from here?

Because EPS has risen too fast due to higher margins. Could be market thinks these margins, are peak and not normalized for entire cycle and thus has not given Peak PE to Peak EPS/margins.

4 Likes

ok. But the results have been good overall, let us see the Q1 24 results. Where will the share price go from here? What are the thoughts here - will price increase?

The direct cause is FII has reduced the stake consistently. I dont find any other reason.The fall is very steep. Some long term observer should shed some light on this

1 Like

Price will keep moving up & down. Focus on the business. Follow historical PE, and PB ratios and be aware of not investing at historically high valuations. If PE is too volatile, use PB as it is usually more stable.

Have a reverse DCF model with ROE and reinvestment rate inputs which will give you the implied growth rate in the price today. Choose a conservative exit multiple, preferably below average and not a peak one. See if the implied growth rate is sustainable. If not, wait for the price, and valuations to come to your desired price.

3 Likes

Yes, it’s FII selling coupled with high margins last year and 1-2 exceptional quarters like Sep’22 which has led to PE come down to 23. Even 5Y median is around 42. Once margins normalize the PE should again shoot up.

2 Likes

- Patalganga is expected to achieve full capacity by Q4FY24.

- The Thailand Joint Venture (JV) was delayed and is now expected to start by Aug/Sep 23.

- These developments are expected to contribute significantly in the coming years.

- The company conducts no concalls, making it difficult to track and stay updated.

- Management has mentioned that the margins and topline of last year were one-off and cannot be sustained, indicating their integrity.

- Seeking updates on the following:

- Current status on Thailand JV

- Is Patalganga on track to achieve full capacity by Q4FY24?

- Land parcel from Gujarat for expansion - a long-pending point. They had also considered a plan B for procurement of land from MH.

- Price fluctuation is not a concern, but the lack of accessibility to information due to the absence of concalls is troublesome.

- Requesting any inputs to help with the situation.

- Disclosure: Invested.

11 Likes

@Mudit.Kushalvardhan wanted to know from where do you get the sector reports? is there any website to refer? Wanted to know what is the sector growth for Fine. Thank you.

2 Likes

5 Likes

How do the FIIs & DIIs get the required insights from the management if Fine Organic doesn’t do Concall? How are you gathering information? Is there any way to get the insights about the company? Plz reply

Companies often meet institutions even when they do not do concalls. Of course, some companies do not even meet management and only do AGMs, but increasingly that is becoming rare.

And meeting management is not the only way for investors to get the required information. Fine Organics regularly publishes their investor presentation which has a decent amount of details.

13 Likes

Hello, any insights on the falling revenue and profits for the past 2-3 quarters ?

I believe there has not been a concall recently.

Fine Organics — Q2 FY’24

Fine organics posted their results for Q2 FY’24. The market did not react well after which the stock slumped by about 12-15%. This post is my take on the results. I would love to hear all of your opinions on the same.

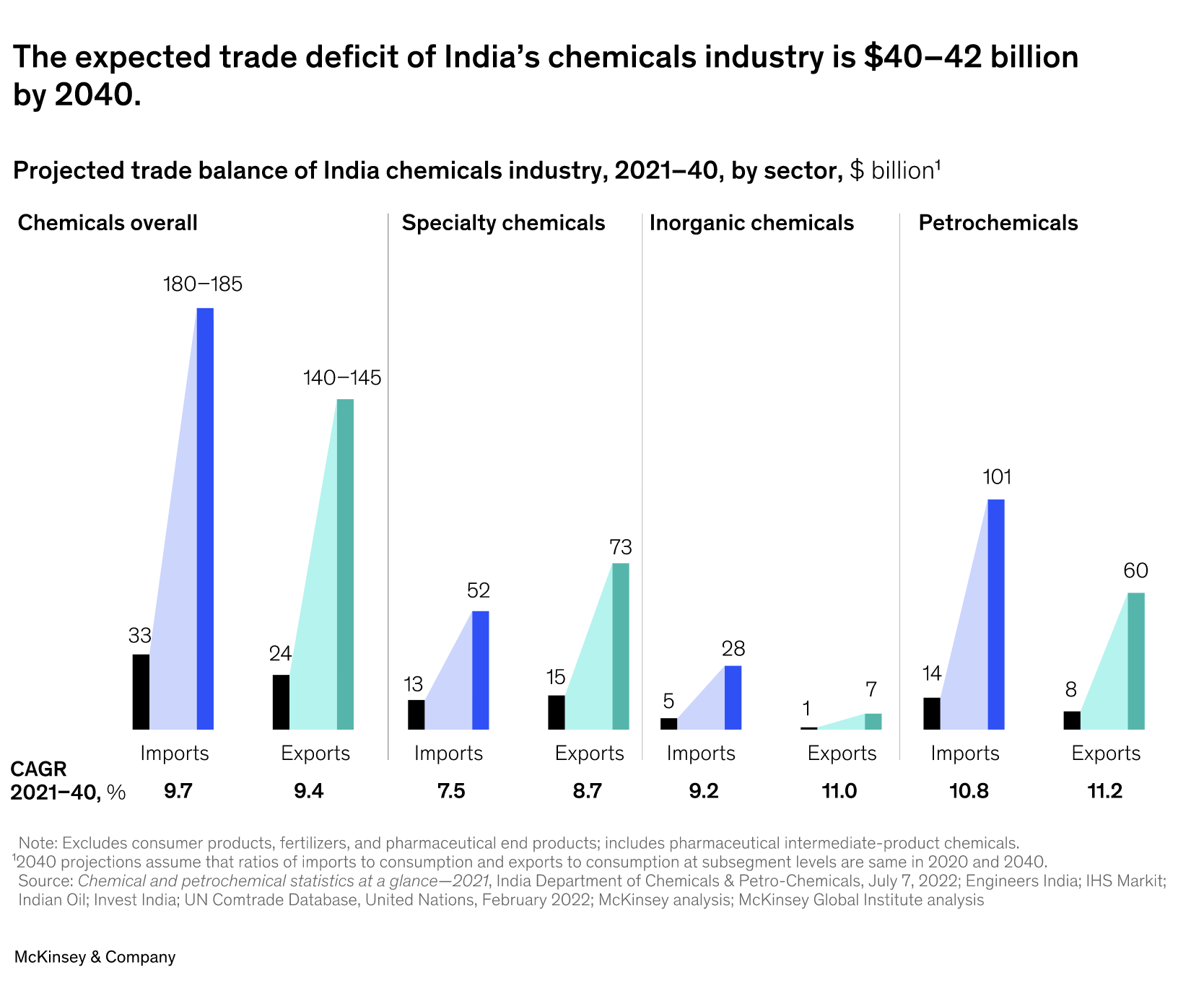

Chemical sector prospects (India):

- Exports: 13% CAGR growth (7% in China)

- Speciality chemicals: Expected to double by 2027 (12% expected CAGR)

- Here is an interesting snippet: Speciality chemicals is the only chemical sector which is expected to have a positive trade balance (exports > imports). Meaning net exporter of chemicals.

What about the Indian Oleochemicals market?

- Projected growth - 3.8% CAGR (through 2029) (Just to compare: IT - 4% CAGR, Retail - 2.5% CAGR)

- Key drivers - Growing demand for oleochemicals in Pharma, personal care, food & polymer industries

Current Market Size (2023) - $1.76B

Sectoral conclusion:

Fine organics is very well placed sector wise. Its long term growth and demand still looks to be in-tact. Export markets will be key. While this brings in more prospective business opportunities, it also adds more external factors to account for like trade barriers and policies.

Results - Q2 FY’42

Summary (standalone):

- Revenue: Rs 472Cr (-43% YoY)

- OPM: 22%

- Net Profit: Rs 79Cr (-51% YoY)

- No significant change in shareholding pattern

On the face of it, the results look disappointing.

Let’s dig slightly deeper:

- China dumping problems: Quoting the words of Jason Soans, Lead Research Analyst, IDBI Capital Markets:

Over the last few months, China has been dumping stock, especially chemicals. That has predominantly happened due to low demand in their home economy. And as is well known and is well covered, that there is a lot of slowdown in the Chinese economy. And they are trying to fight that in terms of exporting more and more, especially at rock bottom prices or predatory pricing, which basically has impacted a lot of commodity players. With the aftermath of Covid and companies looking to derisk and diversify, Indian companies look attractive. But again, here, we are more skewed towards specialty chemical players. These players are much higher up the value chain vis-à-vis a commodity play which is price led. We prefer players which are higher up the value chain. Now the demand has improved in China, and when this happens the intensity of predatory pricing or dumping will recede and we expect it to happen in the coming months.

-

Inventory destocking: A quick glance at the financial result will quickly tell you that the company has a positive change in inventory of Rs 26Cr. Compare this to Q2 FY’23, the company had a negative change in inventory of Rs 12Cr. Chemical companies often go through stocking and destocking cycles. Stocking occurs when companies increase their inventory levels (for example anticipated demand), while destocking occurs when companies decrease their inventory levels (for example to reduce costs, decrease in demand). It looks like the destocking cycle has slowly started to end and stocking cycle has begun to take presence across the sector. It’s not a sudden process but takes a few quarters to play out.

-

General demand slowdown: India’s doing comparatively well but due to a general slowdown in demand globally (especially in the larger economies), export oriented sectors like chemicals are experiencing a bad cycle.

-

Margin contraction:Over the past 7 quarters (standalone), OPM margins have clearly contracted. With a mean quarterly OPM of 25.4%, the current quarter Q2 OPM is sitting at its lowest in the last 7 quarters at 22%. Can the margins contract more? That is a high possibility, due to the fact that even with declining input/raw material cost the company will have to pass on the benefits to its customers. But as demand starts to return we could see a reversion to mean OPM and beyond. At-least it’s good to know that we are somewhere closer to the bottom of the cycle than the top.

-

Market expectations for the quarter: Beaten market expectations comfortably

-

Capex/expansion problems: the non-availability of land for further expansion as of now is a cause of concern in the short to medium term with plants running at optimum utilisation. Only Capex due to commission in Patalganga, as mentioned earlier in the thread was expected to reach full capacity by Q4’FY24 but I could not find if any updates on the timeline. Inorganic expansion opportunities are limited.

-

Delay in Thailand Joint Venture (JV): However once started and functional should contribute significantly to the top line numbers.

Valuation

-

PE: Currently trading at a PE of around 30. The valuation has worsened due to the bad numbers. 5 year median PE stands around 40-45, but it’s not far off. Another bad quarter and you’re headed your way there. So the company is definitely not undervalued as of now.

-

PEG: Currently at 0.63 which looks like the current PE is justified for now. However, the PEG has been increasing for the last few quarters definitely showing that growth is slowing down faster than the price is dropping. This could signify that the down-cycle was factored in fairly early.

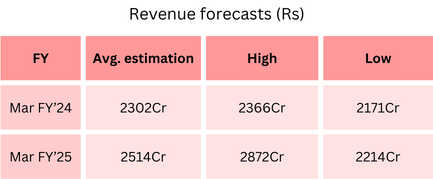

Market estimations for FY’24 and FY’25

Please take these estimates with a pinch of salt. The takeaway from this is that it does not look like there is going to be a fast uptick coming immediately. The coming quarters will be key in identifying bottoming out patterns both technically and financially. Keep an eye out on the margins and PE. Hopefully you found this helpful.

25 Likes

This is a great analysis of the results. From various analysis, it seems that expected revenue growth rate is around 10%. Did you come across any estimates of the revenue growth during your analysis?

1 Like

Hi, Great analysis. Just a query: I am not sure how China dumping is impacting here. The oleochemical additives which FO deals in, is having very few players globally. Not sure if China dumping is actually the cause of concern. Till now, I am not able to figure out such a drastic change in revenue

2 Likes

Have had a detailed call with SGA which handle Fine’s investor relations. Important points to note:

-

The way they defined fine’s products are through the following analogy: Say you want to cook Chicken. You just need handful of spices as a proportion of total volume of chicken. But these handful spices in small amount, makes big difference. Similarly, fine’s products provide the finished touches in such a way that it is not possible to manufacture the final products without them

-

There are a couple of competitors in the oleochemical based additives. However, the bouquet of products which are present with Fine is huge. Hence the MNC’s tend to go with the supplier having a range of products rather than a singular product

-

They sign the contract with MNC’s for the supply. This contract can be short term or long term depending upon the prevailing price of raw material. When the raw material prices are high, the customers tend to sign short contract vis a vis long contracts when the prices are low

-

SGA iterated that 28% EBITDA displayed is unsustainable. The prime reason was a lot of inventory of raw material undertaken during lockdown which got sold for high prices in 2021 due to raw material inflation. These contracts were short term

-

Contracts are up for renewal this quarter. The prime objective of the customers would be to sign long term contracts this time since RM prices have normalized. Going forward there might be the pressure in margins

-

One should expect a steady state 18%-20% EBITDA. China has no impact on this business since it is highly specialized. The application of these products are in a mission critical sector, hence the suppliers cannot be changed easily

-

Although the content of Fine Organics <0.8% by weight in the final composition, still they do not enjoy pricing power (as opposed to what is claimed by Marcellus). The MNC’s always treat them as “just a raw material provider”.

15 Likes

I think we need to see Fine Org in a different perspective.

If the buyer views their products as a must have and they cant do without them its a very big competitive advantage or “Moat” as its called. The possibiltity of a competitor entering becomes less and customer stickiness will help grow the business. It will take years for any other vendor to meet the levels of quality.

In my view if the product they sell is a small portion or the overall spend and very important it means that the company at some point will have a pricing power since they will not go below a certain price point and compete on pricing and can ( if they have the stomach) demand a better pricing ( I wouldnt like to believe what a PR agency says), and this is something we can try in our personal lives as well. That beside such companies will always be in demand and will find ways to increase their spend share with new products. The expertise of the company provides a lot of comfort that they will be able to compete in any environment.

Happy to get feedback and also be corrected.

6 Likes