Basic Information:

- Oleochemicals are chemicals derived from natural oils and fats of plant origins.

- Oleochemicals can be categorised into:

- Basic oleochemicals such as fatty acids, fatty methyl esters, fatty alcohols, fatty amines and glycerol, and

- Their downstream derivatives obtained from further chemical modifications of these basic oleochemicals

- These oleochemicals exhibit special properties such as excellent emolliency, surface activity, emulsifying properties, as well as beneficial biological properties.

Value Chain Basics:

- Regarding the value chain, the palm trees are grown on the large lands where the palm trees are grown to maturity

- Once matured, the bunch is sterilized, threshed and oil is extracted. This oil goes into manufacturing various oleochemicals.

- Palm oil is then resorted to a process called splitting by exposing high pressure and high temperature where it is converted into glycerine and fatty acids

- Simultaneously palm oil is resorted to a process called trans-esterification, where it is converted to fatty alcohols and fatty methyl esters

- These products are known as oleochemicals and they are further resorted to sulfination, esterification, ethoxylation and neutralization to form speciality chemicals.

Following table shows the step by step products and the industry structure:

| Value Addition |

Products |

Profitability |

Consolidation |

Key Players |

| Oils & Fats |

Palm Oil, Soybean Oil, Mustard Oil |

Medium |

Medium |

Adani Wilmar |

| Basic Oleochemicals |

Fatty Acids, Fatty Alcohols, Glycerol |

Medium |

High |

Adani Wilmar |

| Derivatives |

Amines, Amides, Esters, Sulphates |

High |

High |

Balaji Amines, Fine Organics |

| Speciality Products |

Polymers, BTAC, lubricants |

High |

Very High |

Fine Organic |

Key Applications:

- Fatty Acids (includes Stearic acid, oleic acid): Soaps & Derivatives, plastics, rubbers, papers, lubricants, personal care, food and feed, candles

- Fatty Alcohols: Soaps & Detergents, Personal care, Lubricants, amines

- Glycerol: Soaps, Alkyl Resin, Food, Polyurethanes, tobacco

Key Points to note:

- Since oleochemcials are naturally processed and are totally biodegradable, they are finding a lot of growth in terms of replacement of petrochemicals which are hard to dispose

- Import of palm oil and oleochemicals attract import duty of 7%-20% which makes the manufacturing process costly. This cess is aimed at improving agricultural infrastructure of palm oil so that we are less reliant on Indonesia and Mayasia

- Malaysia & Indonesia account for 85% of palm oil production. The country, in a bid to become global palm oil destination, cleared vast swathes of lands and employed foreigners to plant palm trees. Once they abandoned the country on account of Covid 19, the palm oil production took a hit and hence prices rose

- Indian government have started introducing MSP’s for the mustard seed extracts and is working on DMH-11 variant which is genetically modified in order to reduce reliance on Indonesia and Malaysia

Fine Organics:

Founded in 1970, Fine Organics was the brainchild of Mr. Ramesh Shah, a Mumbai-based businessman with experience in chemical trading and Mr. Prakash Kamat. Together, they envisioned the potential of oleochemical derivatives and created an organization founded on the pillars of innovation and passion. Fine Organics introduced the Indian market to high-quality additives for specialty applications with raw materials from locally-grown plant sources and quality levels on par with international standards.

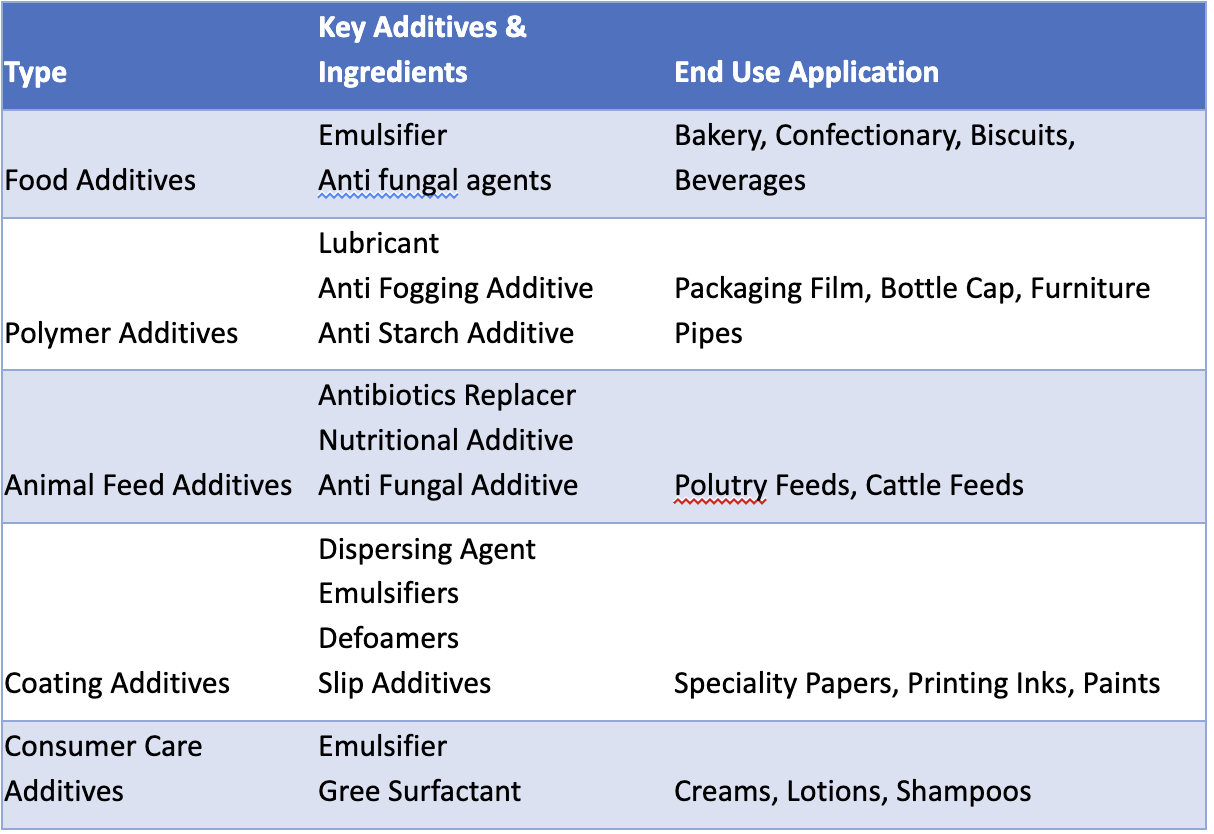

Today, Fine’s range of innovative additives have expanded their reach into several specialty applications in food, plastics, cosmetics, textiles, paints, inks, rubber and many more. They have a range of 450+ products which find applications in majorly food emulsifiers, plastic additives, Cosmetics and Pharmaceuticals.

- In Food additives, these products provide special characteristics to the product like increasing shelf life, good texture, good fluffiness etc. The market was calculated at $3.2 bn in 2021

- In Plastic additives, the products provide aesthetics, make plastic environmentally friendly, give durability to plastic etc. The market was calculated at $22 bn in 2021

Business Overview:

Fine Organics in the business of manufacturing oleochemicals based derivatives and speciality products used primarily in food additives, paint additives, polymer additives and speciality additives.

The company has the portfolio of 450+products with 180+ distributors and 800+ direct customers. The products constitute less than 1%-2% weight of the final product but they impart the structure and texture to the final products like foaming properties to consumer care, proper texture to the final biscuit/bread etc.

The company has 7 manufacturing capacities across Maharashtra. All of them are situated closer to port areas since they derive majority of revenue from exports customers

What I liked about the business?

- R&D nature of business: These products require high R&D and hence only players can afford the game. On the top of it, there is a patent evergreening which happens and hence the competitor is unable to replicate the formulation

- Capex Costs: High capex cost for R&D and process design

- Approval Process: Since these products cater to industries like food, animal etc., the companies take 3-5 years for the approval process which further constraints the ability of competitors to enter the market

- Focus on domestic palm oil and vegetable oil: Raw materials which are raw palm oil or basic oleochemicals gets imported from Indonesia/Malyasia. Indian government has started focussing on domestic production of oilseeds

- Limited Competition: Due to technological advanced chemistry, FIne Organics is the only player in India. Even globally, there are 6-7 competitors: Kerry group, danisco, palsgaard, Riken vitamin, Taiyo

- Pricing Power: The company enjoys a pidilite advantage means the cost of additives is less than 1% of the final cost of the product. Even if the company increases its price, there is minute difference in the final cost of the products of the customers

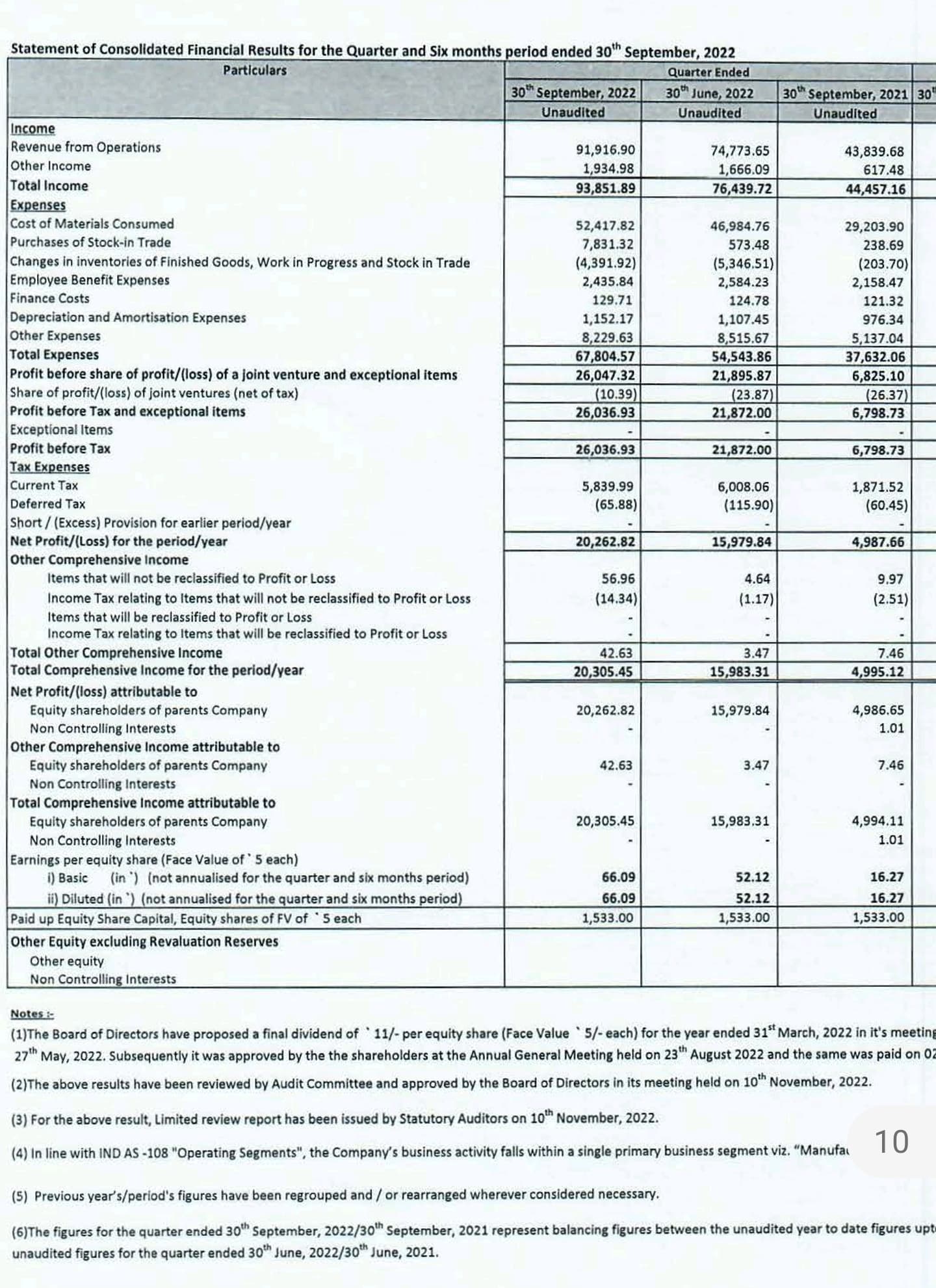

Financial performance:

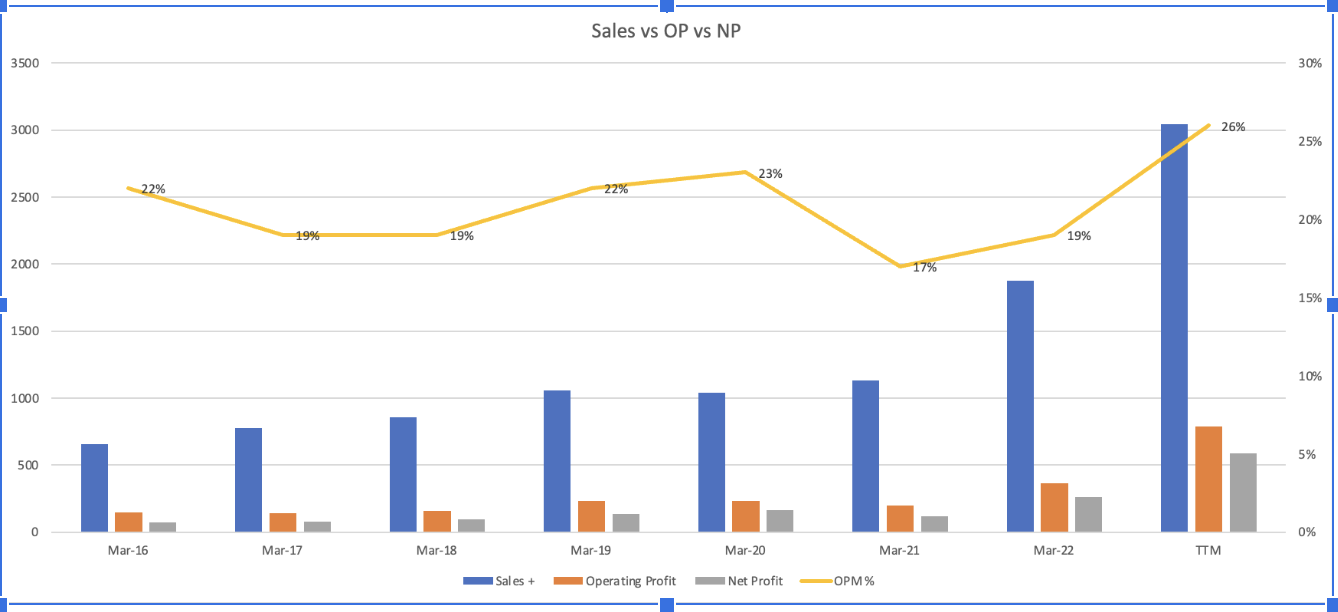

The following chart shows the sales vs Operating performance:

We can see a dip in OPM in 2020-21 due to the lockdowns during which the company had to incur high pre-production expenses but could not exercise sales.

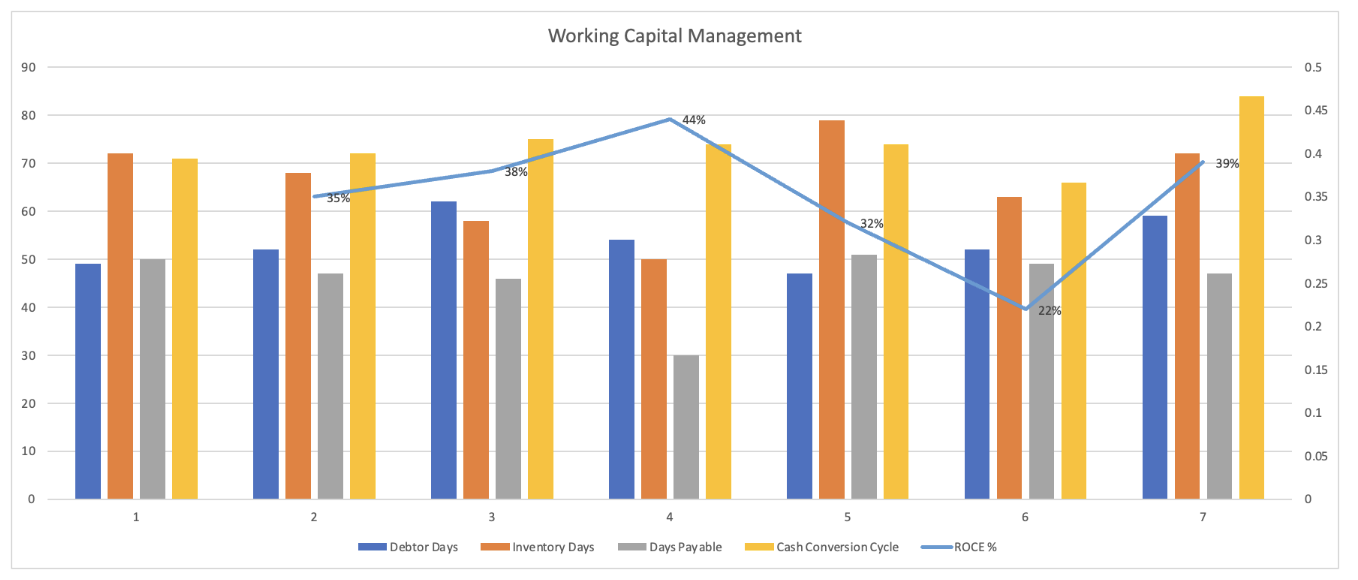

However even then, the company is able to manage the high ROCE:

The cash conversion cycle is consistent at 70-90 days primarily on account of >60% of revenues coming from export.

The delivery of the products to the customer takes time and on the top of it, the credit period provided to such customers increase the receivable days for the company

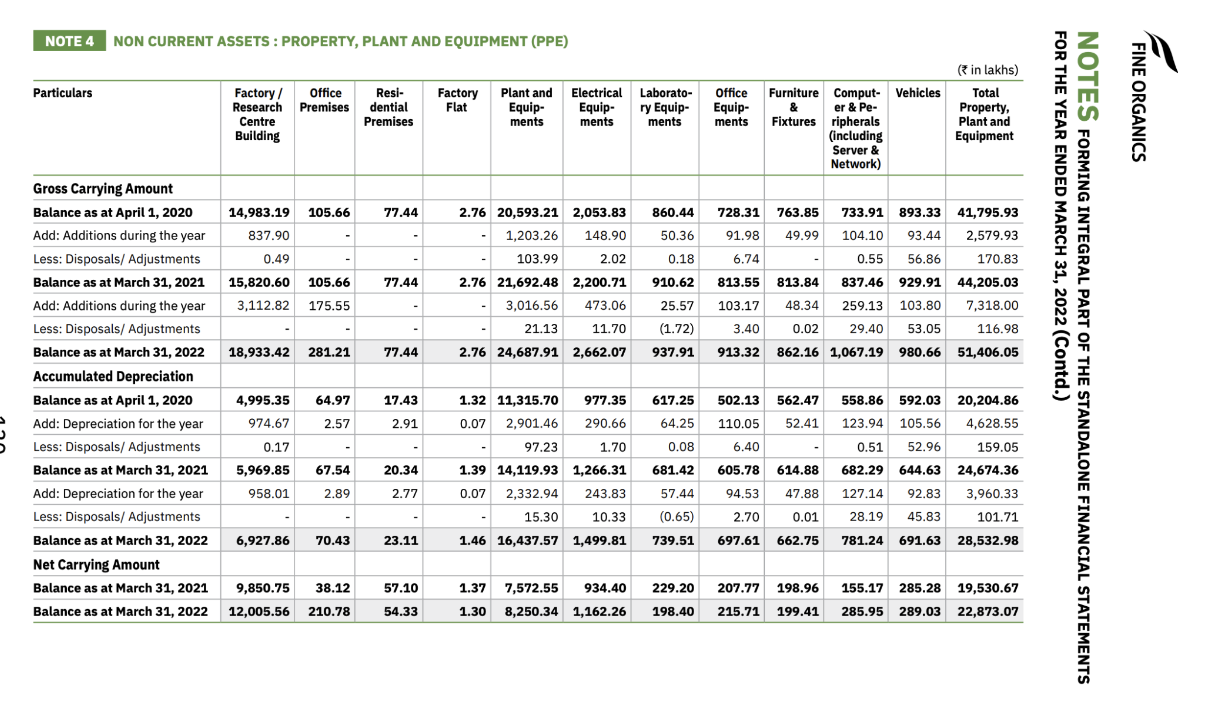

In case of fixed assets, the majority of the asset schedule lists factory, plant, equipments and electrical equipments which should be obvious given the R&D intensive nature of the products.

The promoter group has all together drawn the salary of 18 cr which is well within the limits. Sales to related parties is minuscule at 8.8 cr which is also well within the limits. However in non current financial instruments worth 43 cr, 40 cr went towards equity investments in subsidiaries[image]

There is a humongous increase in inventories from 126 cr to 236 cr to 296 cr in FY 20,21 and 22 respectively. As a result, the company is not able to convert Profits into cash flows in the recent years

Key Risk Factors:

- Unable to convert profits into cash for the last 2 years

- Volatility in raw material prices could impact the operating profits margin

- They have been issued a notice in the past for polluting the vicinity of their plants. Unable to comply with government could result in disruption of profit pools

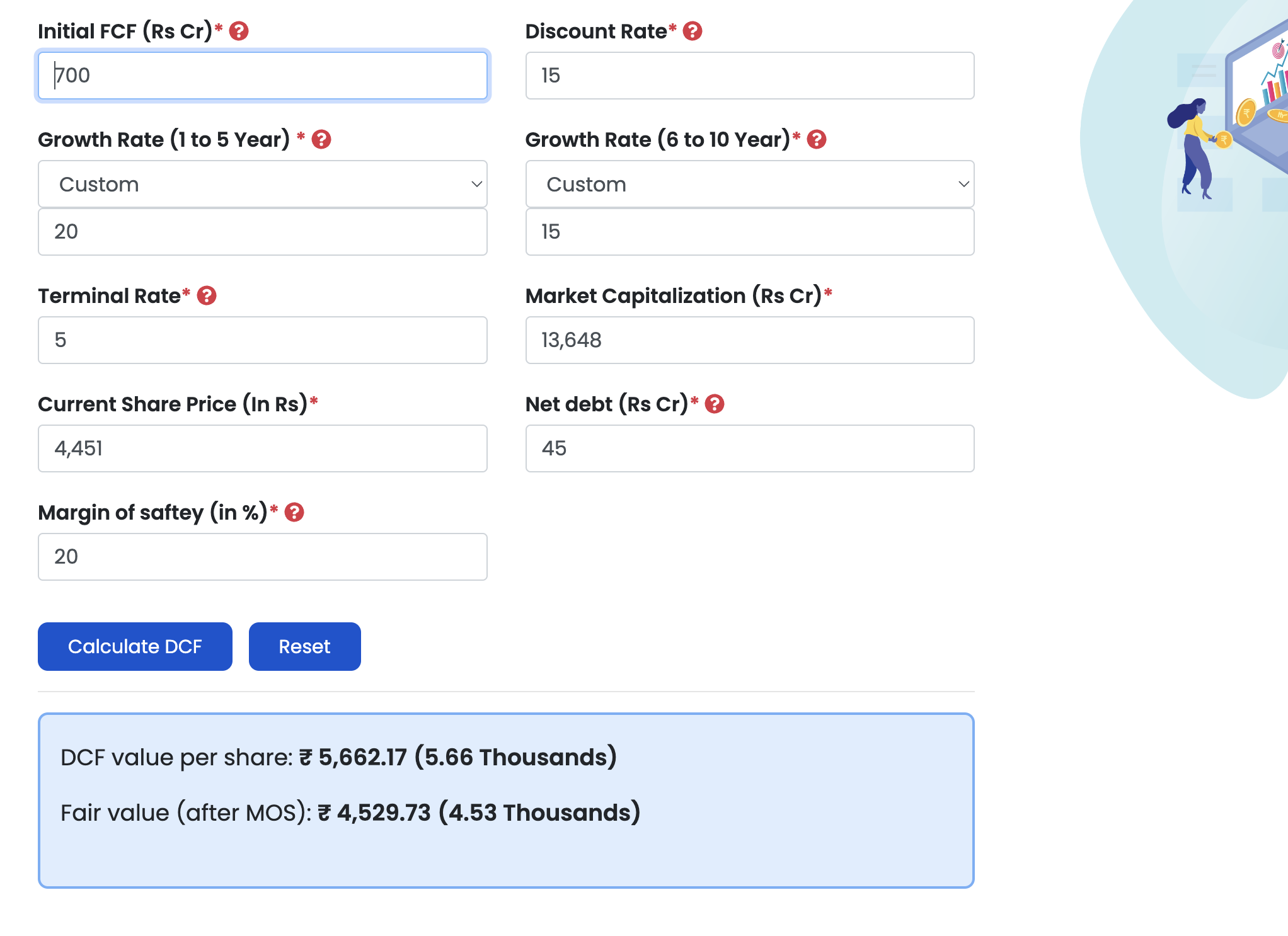

Valuations:

Given the limited competition and the concentrated nature of profit pools, the company is trading at 23 times which is decent. In DCF, considering the growth rates as 20%, 15% and 5%, the price comes at 4451 with 20% margin of error