FY 22 PPT

Co Shud get rerated.

FY 22 PPT

Co Shud get rerated.

Post these results now feel the new range will be 250-300 soon . The future looks bright with CNG . Yesterday a taxi I ordered was fitted with a CNG ( BRAND NEW ) and he informed the swift gave him 25 avg on CNG and it cost him 83 rs a km .

The concall was held today at 4 pm and company has already made the audio available on it’s website.

In earlier quarters the intimation of the call also used to happen many days after the results.Good to see that the IR team has taken things up a notch.

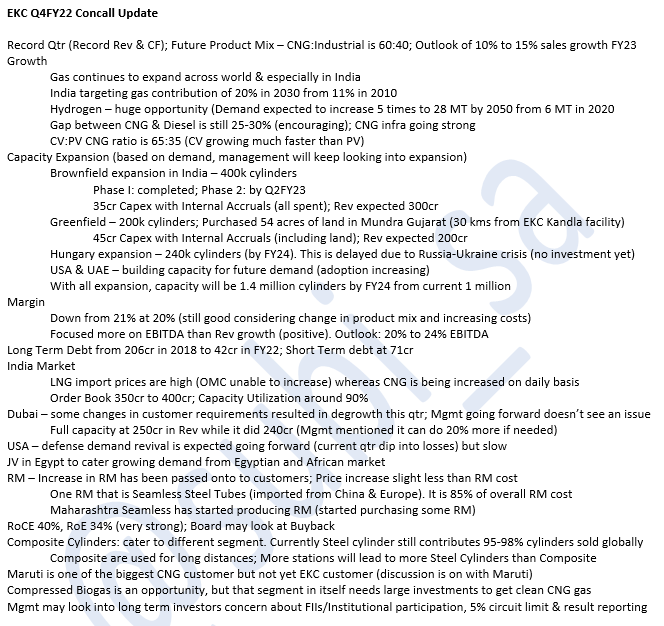

Everest Kanto Cylinder Q4FY22 Concall Update

(Nirmal Bang Securities)

Expect volume growth of 10-15% in FY23

Outlook: Positive

• Revenue came at Rs. 479 Cr (+3% QoQ, +68% YoY)

• India revenue came at Rs. 372 Cr (+60%), UAE at Rs. 53 Cr (+57%) and US cum Hungary at Rs. 52 Cr (+160%).

• Gross Profit Margins came at 45.6% vs QoQ 44.5%, YoY 47.9%.

• EBITDA Margin came at 19.7% vs QoQ 21%, YoY 14.4%. EBITDA margin guidance is in the range of 20-24%.

• Within CNG, mix between PV:CV is 35:65.

• Co is on track to complete the 2nd phase of the 1,00,000 brownfield capacity in India by Q2FY23.

• The above is in addition to the greenfield capacity of 200,000 cylinders that the co is pursuing in parallel for which co has acquired 53 acres of land at Mundra. This 2,00,000 cylinders capacity will have potential to generate revenue of Rs. 200 Cr and will cost Rs. 45 Cr. It will be funded by internal accruals. The facility will come up in 3 phases of which the first phase will complete in Q2FY24.

• Thus the current 10,00,000 cylinder capacity in India will increase to 13,00,000 in coming years.

• Co was working on expansion of 2,40,000 cylinders in Hungary. However due to the ongoing Russian war, co has postponed its plans until it has more clarity. Total capex required will be Rs. 134 Cr in Hungary. EKC will invest Rs. 20 Cr. Govt of Hungary will provide an incentive of EUR 4.8 mn and remaining would be funded via debt.

• Co will set up of a CNG cylinder production facility in Egypt in the form of a JV with a local Egyptian partner with majority holding being with EKC.

Stock is trading at P/E of 8.0x FY22.

Fantastic results from the company

Double bottom reversal. Technical indicators also seem to be aligining.

Management giving very conservative guidance.

Bit perplexed with the MD’s responses on the media and concalls. Being conservative is fine but one sentence answers without much clarity to a good set of questions in Q4 2022 concall makes the management credibility a debatable issue. Hope I am not the only one thinking in these lines

Totally agree with you and even I felt the same. At the moment taking a conservative approach in the allocation unless I see a solid management commentary in the near future.

CGD segment is the biggest demand driver for EKC. All companies supplying to CGD like Ratnamani and JSW (Steel pipes) are gaining due to this. EKC is going to run at full capacity for next 10 years due to CGD expansion.

Demand is also high due to CNG stations (cascades), CNG transports and CNG cars and also industrial users. CNG is clean fuel and is going to replace other fuels.

EVs have their own challenges. By the time EV grows Hydrogen technology will come in - technology is evolving faster than we know.

With so many cylinders being sold we are forgetting that replacement of old CNG cars and industrial cylinders will happen. EKC has been selling cylinders for 40 years which will lead to more replacement demand.

With so many demand drivers, I will not be surprised if EKC announces increase in capacity at their greenfield plant in Gujarat from 2 lacs to 6 lacs cylinders this quarter itself. Also i am assuming the cylinders will be larger as CGD cylinders are much larger than car CNG cylinders - leading to higher sales and profits. By FY 24 EPS should be 35. If the new foreign subsidiaries become operational then it could be higher. Based on India alone the price at 12PE should be 400 in a years time. Risk is negligible and return is certain !!

Request other forum members to add or give counter views.

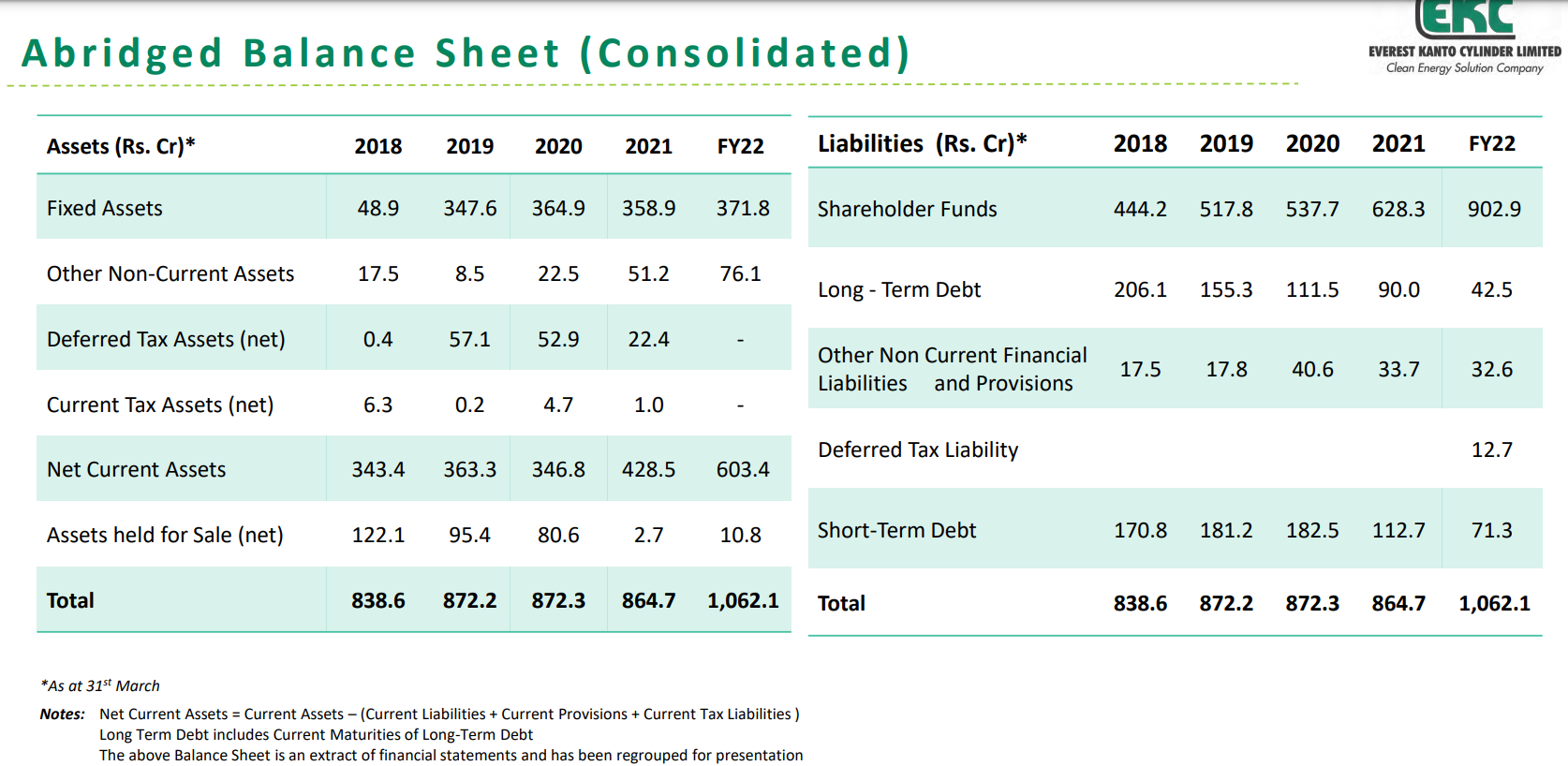

In 2017 management was confident of becoming a debt free company by the end of FY18.

Source: Company To Be Debt Free By End Of FY18: Everest Kanto Cylinders - YouTube

Whereas, till FY22 still the company is having Rs.42cr as long term debt.

well, the trend clearly shows it’s decreasing and they’re serious about reducing it. What else is there to analyze, specifically on the debt front?

Nothing to analyze whether the debt is reducing but the comment was more on the management’s credibility.

Being confident on a news channel about reducing debt within a year and that same debt is still not being reduced in the following four years does tell us something about the management.

how? Your own screenshots show it as reduced from 206 to 42! If anything, all it shows the management being overly optimistic about their growth and that they havent caught on the COVID wave to expand when everyone was running for cylinders.

By “reduced” I meant becoming debt free.

One side management saying they will become debt free in months and then they it take four years and still the company is not debt free. That is what I meant.

Management evaluation is a subjective thing so I will leave it up to you but I shared that video for food for thought on management’s prior guidance.

EKC went through a near death experience due to their aggressive expansion specially overseas colliding with global slowdown in 2008 & US sanctions on Iran which had become their biggest customer .

Founder Late Mr Prem Kumar Khurana son of a refugee from Pakistan worked in account section for an IOC dealer who encouraged hime to go on his own. he started an Unit in Tarapur went for a collaboration with Kento Japan & reversed engineered to gain the technological knowhow. He was having huge growth mindset & expanded aggressively overseas once he saw not much growth coming in India which proved to be his undoing due to abovementioned reasons.

Inspite of all the issue unlike others he repaid FCCB in full without any haircut even when Yes bank was the only bank willing to fund him albeit at high intt rate against promoter promoter shares pledging. All these shares were depledged recently after new CFO came as tailwinds returned to CNG sector & selling off some overseas plants in China & thailand. This speaks volumes about promoters ethics & intent and gives a big comfort to minority shareholders.

EKC is nicely walking the talk over last several qtrs under 2nd gen who though may not be eloquent are totally focused on business. Tailwinds hv returned back for sector in India as wel as abroad & co is executing nicely with debt being reduced nicely, *

ROCE NOW 40% ROE 34 %, ALMOST ZERO LONG TERM DEBT NOW lot PE at 8 which is low for a market leader in a segment growing fast giving huge margin of safety, 67% promoter stake all depledged, capex coming online & more in offing.*

One needs to be focused on business & not get distracted by stupid 5% limit making the share volatile rather take advantage of its volatility.

They had also not said anything about expansion so should we say the management is bad. surplus cash is being used for brownfield and greenfield expansions. if expansions were not happening they would have become debt free long time back.

I would say management is very good to see the changing demand scenario and go for expansion in India at the right time - especially after their Gandhidham plant had to be sold as the demand did not pick up as they had anticipated - they were ahead of their time. Also China was a wrong country to set up such a large plant.

Now their expansion model with local partner is the right way to go ahead with minimum capital and quickly and at same time having 80% ownership. they are leveraging their leadership position to grow larger.