What is heartening to hear is - “US subsidiary is doing well”…That has been the issue over multiple quarters until a couple of quarters ago

Besides, the cash conversion cycle have been a challenge

CNG adoption appears to be a massive tailwind at the moment

US has stopped losing money as was the case last year. That itself contributes Rs 15-20 crore to the annual profit.

Given EKC imports a fair share of their RM (seamless steel tubes) from China, I wonder how serious the fall out of China’s covid wave getting out of hand would be? As far as I know, the freight situation is already getting worse there.

Actually the input APM gas prices has been increased by around 130% with effective from 1st April’22 i.e from $2.9 /mBtub to $6.13/mBtu.

They gradually passing on such stiff hike…

EKC came out of ASM after a long time which seemed a good omen.

Further revision of limit from 5% to 10-20% may drive away operators indulging in the scrip.

One needs to be focused on business & last week interview on CNBC was good. valuation wise it remains one of the cheapest stocks for a leader in segment which itself is growing fast .

India produces nearly 50% of gas required locally tks to prolific KG basin & RIL production starting & ONGC next in line. Price increase in gas after a long time augurs well for further increase in India local gas production hopefully.

Discl- Invested

Some positive news coming on domestic gas production front at prolific KG basin now by ONGC preceded by start of RIL gas production . Domestic gas production even at 6-9 $ per BTU price is much better then high imported gas price.

US engineering and construction giant McDermott has delivered India’s Oil & Natural Gas Corporation’s (ONGC) with the keys to the KG-DWN-98/2 deep-water gas field development in the Krishna Godavari basin off India’s eastern coast.

The company said on Wednesday that the successful conclusion of the contract covering the subsea production, risers and umbilicals systems for the U-field was achieved in spite of the challenges posed by the Covid-19 pandemic and an active monsoon season.

McDermott, along with Baker Hughes and India’s Larsen & Toubro (L&T), was awarded a $1.69 billion integrated subsea contract by ONGC in October 2018 for work on the KG-DWN-98/2 asset.

McDermott chief operating officer Samik Mukherjee said that, completing the subsea campaign, combined with an earlier milestone of putting an early production system in place within 14 months, demonstrate what he described as the company’s “ability to deliver complex subsea projects in challenging circumstances”.

McDermott described the KG-DWN 98/2 project in the Cluster-2 region as “the largest and one of the most complex subsea projects in the Asia Pacific, involving major subsea infrastructure installation in ultra-deepwater”.

ONGC commissions huge offshore platform in prized Mumbai High asset

Read more

While the overall Cluster-2 development is said to be running behind schedule, owing to delays in commissioning key facilities, ONGC is tying back some of the gas fields to its existing infrastructure on the east coast.

The U-Field is now connected to ONGC’s Vashishta subsea infrastructure, it added.

First gas in 2020

ONGC achieved first gas from KG-DWN-98/2 development in 2020.

McDermott said in 2020 that the first gas from the deep-water block “involved the tie-back of a single well to the existing Vashishta facility”.

“At 4265 feet (1300 meters), the first well that has been opened for early first gas is the deepest water depth opened by ONGC,” it said.

Vintage rig: ONGC’s first jack-up Sagar Samrat converted into Mopu

Read more

The US-based contractor noted that it is delivering two gas systems for ONGC’s U-Field and R-Field.

“Upon completion, the gas field is expected to significantly increase domestic production, helping meet India’s increasing energy demands while lowering reliance on imports,” McDermott said.

Key milestone

Subramanian Sarma, senior executive vice president (energy) at L&T said “the opening of the U1-B (GX-06) well in the KG-DWN-98/2 block is a major milestone” for the consortium partner.

ONGC recovers offshore jacket stranded at Vietnam yard by Sapura cash woes

Read more

"That we managed to achieve this despite extremely difficult project terrain and weather conditions even as a global pandemic raged on, speaks volumes of the resolve of the project teams,” he noted.

Big spending

ONGC is spending more than $5 billion on the Cluster-2 development as part of a plan to produce more than 16 million cubic metres per day of gas and an additional 78,000 barrels per day of oil at peak from the region.

In addition to the Cluster-2 area, ONGC has been planning to launch the development of the KG-DWN-98/2 block’s Cluster-1 and Cluster-3 regions.

ONGC floats tender for two deep-water drillships amid oil price surge

Read more

At peak, the deep-water asset is expected to produce more than 35 MMcmd of gas and 78,000 bpd of crude, when all three clusters are brought on stream.

KG-DWN 98/2 lies offshore the Godavari River delta in the Bay of Bengal. It is located 35 kilometres offshore the state of Andhra Pradesh in water depths ranging from 300 to 3200 metres.

Read more

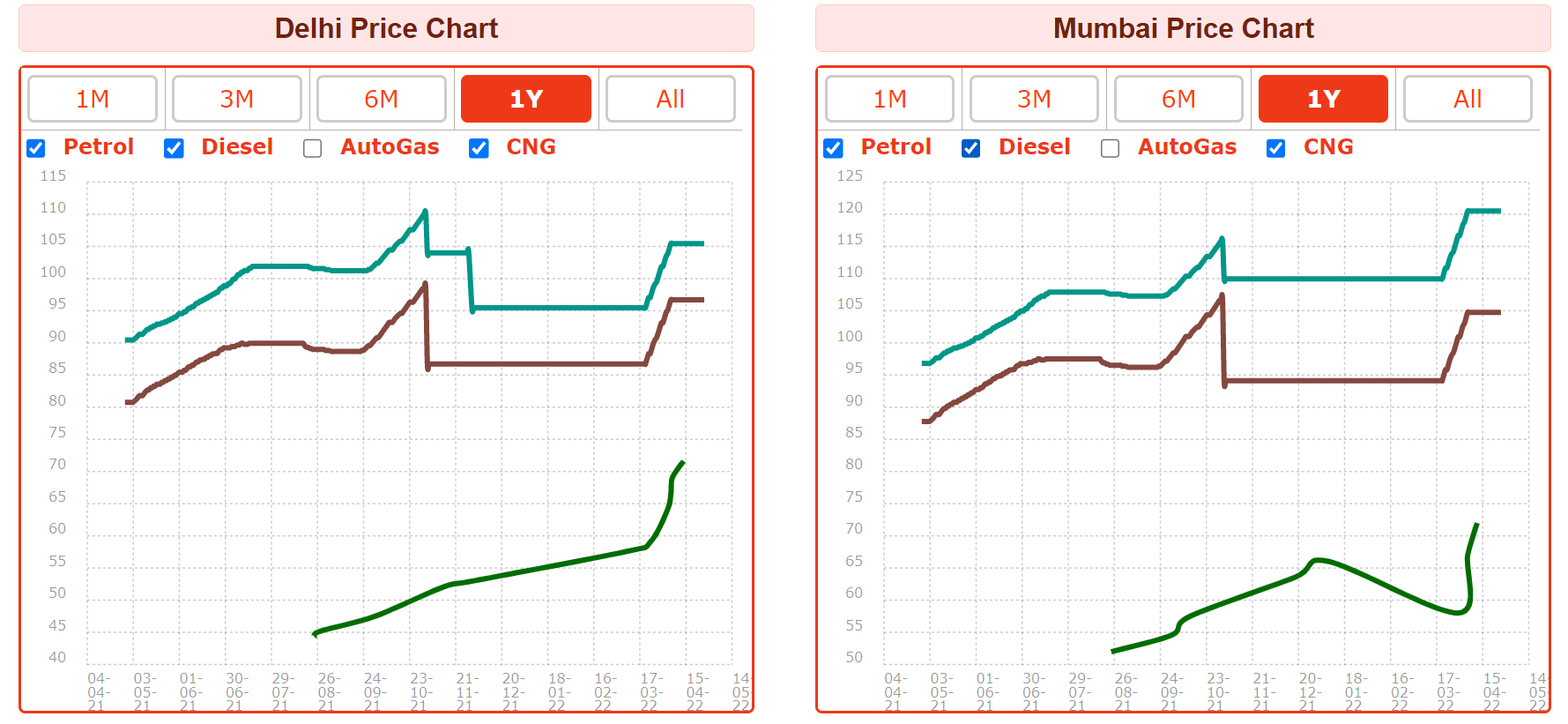

Since March CNG retail prices have spiked by about 24% and Rs 15/kg while petrol and diesel prices have spiked by 10-12% and Rs 10/litre.

With demand from CGD network, CNG transport and industrial cylinders turnover of EKC will cross turnover of INR 2,500 crs after greenfield expansion in FY 24 (without debt). So with margins of 15 % profits will be close to 400 crs - EPS of 35. minimum price will be Rs. 400. Not factoring increase in volumes in foreign subsidiaries. New countries investment being made by EKC is very low (for 80% equity).

In FY 22 EPS expected to be Rs 25, and in FY 23 it should be Rs. 30. By any metric price should cross 300.

Note - only interest cost used to be Rs. 40 to 50 crs every year for EKC which will be almost Nil.

Not sure how reliable these management projections are. For those who have been following the company for some time, how reliable have they been in the past.

In my experience, during last couple of years, they have been ‘good boys’ ![]() . They have walked most of the talk. You can see that in the debt reduction. Cashing out of the complex geographies, Started conference call with investors etc.

. They have walked most of the talk. You can see that in the debt reduction. Cashing out of the complex geographies, Started conference call with investors etc.

Gas prices shud come down around JULY

It seems there is a change in their auditor, have they informed earlier ?

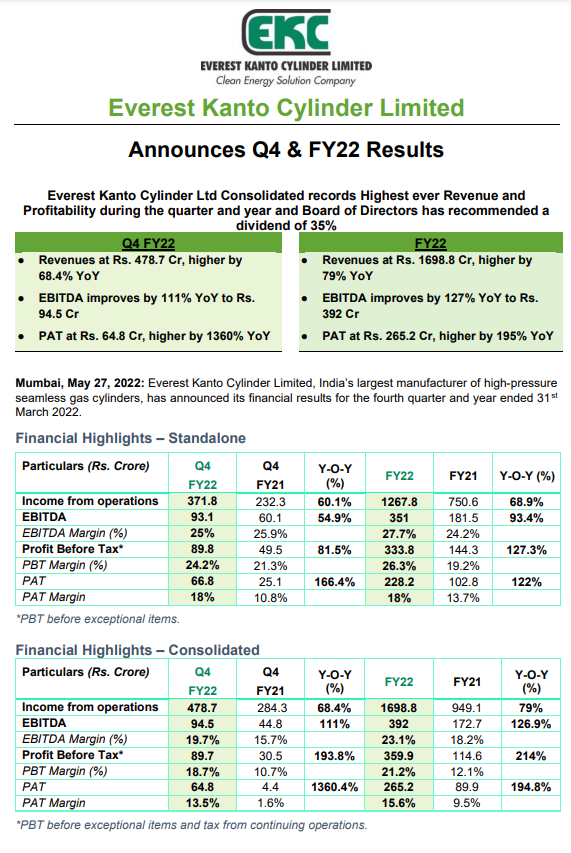

Standalone margins have expanded back to 24% as expected but the subsidiaries continue to be a sore point. US+Hungary has swung back into losses on a qoq basis.This could also be due to Hungary still being in initial stages of ramp up and thus being loss making(conjecture)

One issue atleast in the short term could be the cut in petrol/diesel prices and continued surge in CNG prices.

It seems the unit economics is getting a bit weaker.

It’s the same auditor as previous results.

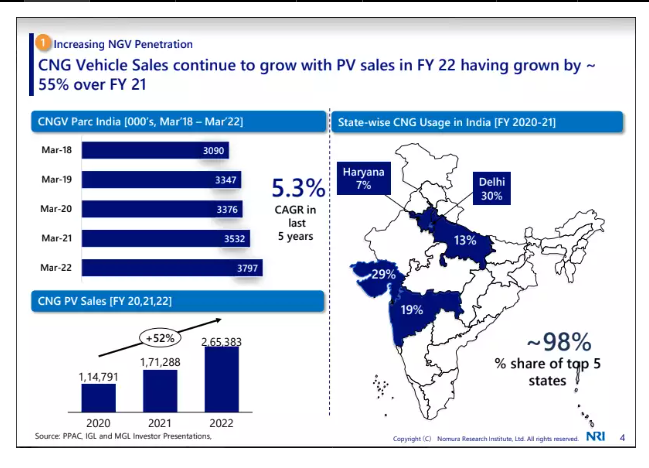

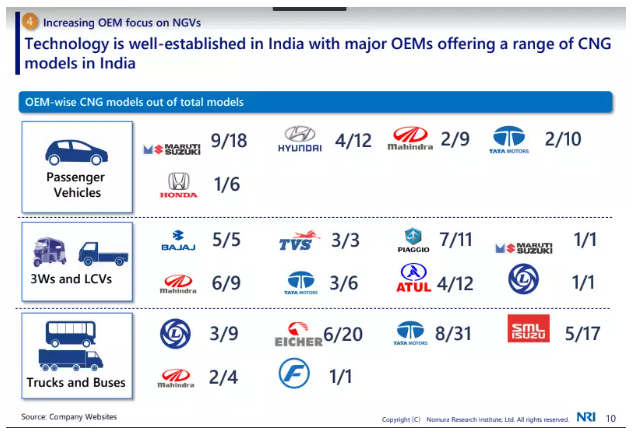

Acoording to NRI CNG vehicles sales continue to grow with PV sales in FY22 up by 55% to 2,65,383 overFY21. Close to 98% of CNG usage is concentrated in the states of Delhi, Haryana, Uttar Pradesh, Gujarat and Maharashtra.

“With increased differential TCO (total cost of ownership) benefits compared to other fuels, CNG is gaining prominence among consumer preference post BS VI. The technology is now well established in India with major OEMs concentrating on bringing in a range of cost efficient and fuel efficient CNG variants,” NRI said.