Good points.

Besides its expanding in countries like Egypt where gas is available in abundance & oil lesser.

There the govt has made registrations of new cars possible only if it runs with CNG.

Opp size for CNG seems increasing nicely worldwide.

Good points.

Besides its expanding in countries like Egypt where gas is available in abundance & oil lesser.

There the govt has made registrations of new cars possible only if it runs with CNG.

Opp size for CNG seems increasing nicely worldwide.

The ~80% revenue growth that EKC has seen Y-o-Y, does anybody what’s the breakup between volume growth and realization growth?

EKC management refuses to disclose any sales volume details in either concalls or annual reports. Snapshots from Q4 concall

In my view, this split is important to project growth momentum for next 2-3 years. Volume growth is likely to be sustainable given the CNG infrastructure coming up, realization growth may or may not be sustainable given new capacities coming in and CNG and crude prices being super volatile.

Sales volumes in FY22 are possibly 9 Lakh cylinders as per this conversation in the Q4 call. What was the sales volume last year? As per AR, capacity was 7.2 Lakh cylinders. (Can’t access Q4FY21 concall transcript on website, throws an error)

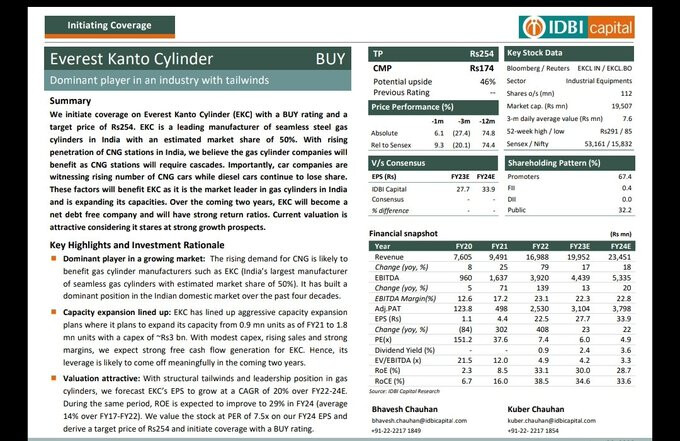

Some research report coverage at last.

IDBI cap initiates with TP 254rs

Leading mfr of seamless steel gas cylinder in India-mkt share of 50%

Rising number of CNG cars

To become net debt free in 2yrs

Strong return ratios

Overseas subsidiaries turning around

Capex:

0.9mn to 1.8mn

300cr

The Everest Kanto story is gradually gaining acceptance. IDBI Capital has initiated coverage on the stock with a Buy recommendation:

EKCL_IC_28062022.pdf (1.3 MB)

Last week, Capital Market too recommended the stock under their “Friday Telefolio Plus”. As time passes & the Co. is able to sustain/ improve its numbers, its only a matter of time before more investors begin to build conviction.

Multi bagger opportunities present themselves when there is growth both the earnings (EPS) as well as the multiple (PE). Everest Kanto potentially can benefit on both these counts going forward. I am invested based largely on this assumption, but as they say, “There is many a slip between the cup & the lip”, so to each his own!

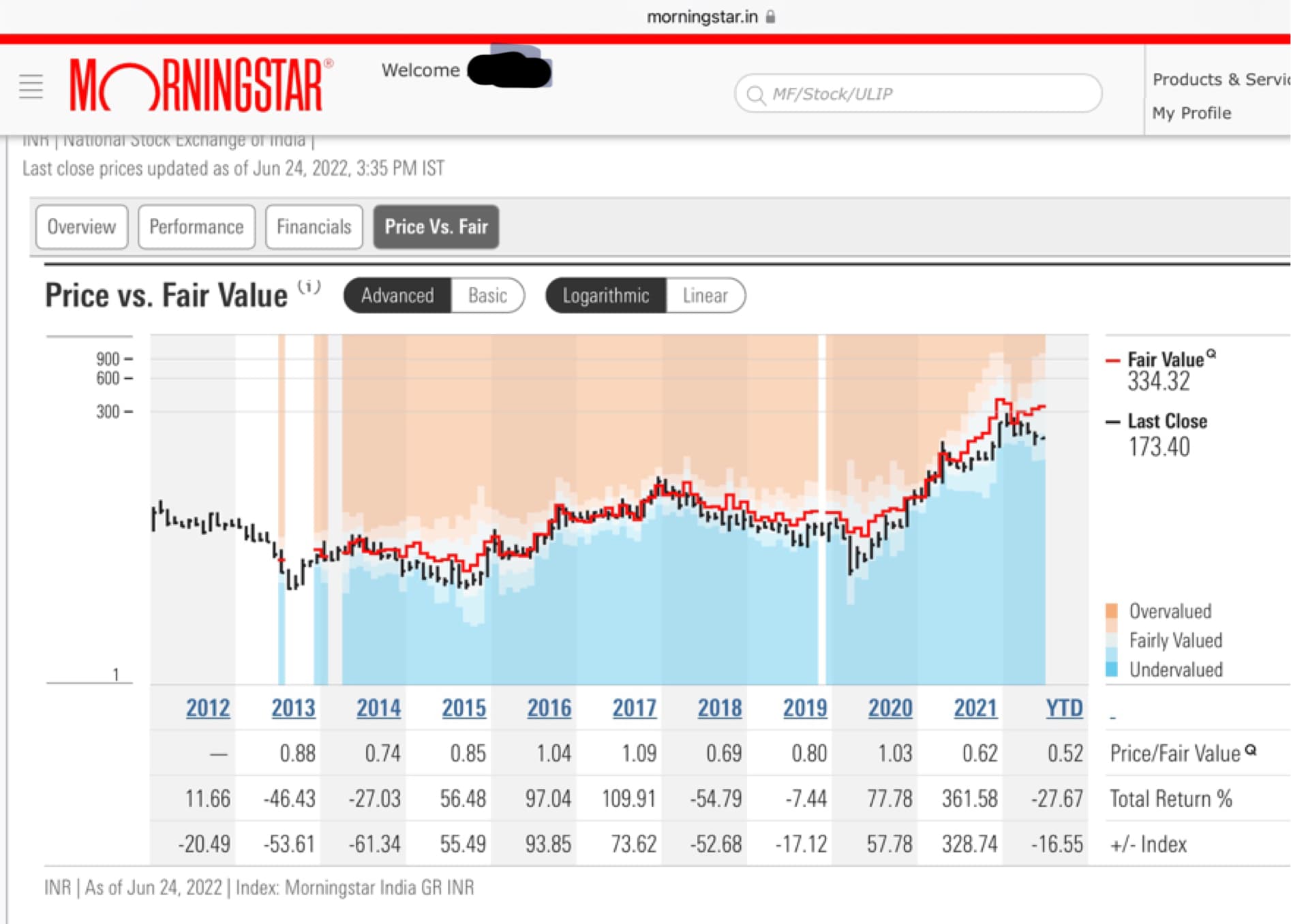

This shows Fair market value of EKC at 334.32/- (Source: Morningstar website)

Sharing news article summary:

“In 2014 the country had only about 900 CNG stations. Today we have 4500 CNG stations with plans to take this number to 8000 in the next 2 years. The number of PNG connections has also crossed 95 lakhs as compared to about 24 lakhs in 2014,” the union minister said."

This could be big opportunity for EKC, 77% increase in CNG station in just 2 years.

Dear all, Despite the excellent numbers and great fundamentals (though some short term blip due to unprecedented gas prices), market is still treating it as a cheap business and it is probably one of the cheapest stocks around wrt the numbers and dominant position.

What are the concerns which might be leading to these kind of valuations? Any comments?

Regards

Nikhil

Disc: Invested for some time but thinking of trimming now.

This is the reason for why the stock is not getting multiples. Talked to quite a few industry veterans. They said trust in promoters is very low especially when they do business outside India or announce they will do business outside India

The fact that all true investors should know that FII have increased their stake in EK from 0.37 % in March quarter to 0.79 % in June quarter . This too during a phase in which we all know overall FII sold into Indian equity . This speaks volumes of the positivity in the stock.

In my view, EKC and other CNG/LNG businesses will have a lower than expected PE multiple because the terminal value of the business (As calculated in a DCF valuation) is expected to be small. That’s because beyond 2035 or 2040, CNG use is expected to stop growing or even start declining. This is the current expectation and may turn out to be wrong and CNG may have a much longer runway than anticipated. But as long as the market doesn’t agree with that I don’t think EKC will trade at multiples of 20x PE or even 15x PE for a sustained period. In the last 5Y period, the stock hasn’t traded above 15x PE for about 20% of the duration i.e. 12 months max.

I try to run a DCF valuation for companies I am interested in. As per my calculations, EKC is fairly valued or maybe slightly under valued right now considering its long term cash flows. In addition, with my limited understanding of TA, I can see that the stock is forming a pretty clear Head & Shoulders pattern on the daily chart right now and any break below 155 may open up a target of 113. That would be a good buying opportunity in my view. I would buy EKC as a swing trade if I get the opportunity to pick it up around 125-130 levels. If the stock crosses 160-180 range, which is my estimate of long term fundamental value of the stock, I will sell it based on technical patterns.

The question for long term investors is, how can EKC increase its terminal value and therefore become a serious candidate for re-rating? One of the factors is continued improvement in corporate governance, which has been rightly pointed out several times in this thread. The other key factor is an entry into an allied business which has a much higher terminal value for e.g. the Hydrogen value chain. Any credible announcement of substantial capex into entering such an allied business will re-rate the company I believe.

Please note, this is purely my analysis of the company and the industry and is not meant in anyway to be investment advice. I may be completely wrong with my terminal value estimates. I am happy to be proven wrong, it will teach me a few more things about DCF valuation. The only way to learn is to put your understanding and thesis down in writing and observe how it plays out over time and refine your learnings basis the outcomes.

Edit : Added the technical chart and corrected the fair value level.

Brilliant Points . My assumptions was that Cylinders would be a key for Hydrogen applications around moving assets and delivery where Pipeline is not feasible . If possible please help me understand Hydrogen Value chain in more details

Thanks

There is a whole thread on Hydrogen economy made by @1957, you can go through it to understand the Hydrogen economy better - Green Hydrogen- The ultimate Green Fuel- Indian companies that are leading the Green revolution in India!

you need to take into account demand for hydrogen cylinders into your DCF calculations. while CNG may decline it will be replaced by hydrogen.

Hydrogen I believe needs cryogenic cylinders, which I am not sure Everest Kanto makes. or has capabilities to make.

https://www.sciencedirect.com/topics/engineering/cryogenic-hydrogen

to transport as liquid cryogenic cylinders are needed . EKC makes cylinders for compressed hydrogen gas.