It seems that both cos. are underplaying the competition.However,the key thing to note is that EKC has the capability to manufacture composite cylinders.Management said,“We are continuously watching this market so we are also keenly looking, in case we feel that the market has matured, we’ll definitely

be taking some position, some actions to be a part of it too.”

2 Likes

I don’t see pricing is going to be deterrent here. It is a good investment for OMCs which is going to help in many ways

- Life span of the cylinder is higher than regular steel cylinder

- Less weight always saves lot of freight costs (less the weight less the fuel you burn )

- From customer point of view they can clearly see through the quantity left, even customer is paying a one time deposit to switch they will recover the same by not returning the cylinder that has little more gas left that one cannot see from outside from steel cylinder

1 Like

While there seems to be a lot of debate about the comparison between composite & steel cylinders, perhaps the market is growing enough to accommodate both types! Investors are free have a preference & invest accordingly. For investors to make money, the Company, whether Time Technoplast or Everest Kanto, must grow both in terms of earnings (EPS) going forward & hopefully get re-rated in terms of getting a higher multiple in the foreseeable future. Also, the valuation of the relevant stock at the time of purchase also has a material impact on the extent of gains that one makes on the investment.

I too hold a tracking position in Time Technoplast. However, what drew me towards Everest apart from the factors mentioned above on earnings growth & valuations, was the higher operating margins, which despite the fall in the last quarter are still much higher. I see growth both in earnings as well as the multiple here. That said, there are many investors to think otherwise & they may even be right - so to each his own! Besides, as investors we are free to change our views. If the performance of Time Techno picks up in the future, I may increase investment in it. One stock need not be bad for the other to be good!

33 Likes

EKC will also benefit from increase in Crude Oil Prices as push for CNG Infrastructure will expedite.

4 Likes

with oil prices going to be at high levels, CNG adoption will increase faster. EKC should try to expand capacity faster…

also with 300 to 400 crores annual profit they should also give higher dividend…

3 Likes

agree with views. i hold substantial investments in both companies. demand for CNG infra whether it is cylinders (both types), steel pipes for pipelines and all supporting equipment will be high for at least 10 years…

3 Likes

6 Likes

CNG vehicle sales keeps increasing world over. Augurs well for EKC.

10 Likes

The country’s largest carmaker Maruti Suzuki is looking at producing more than half a million CNG-powered vehicles in the upcoming financial year amid growing consumer preference triggered by a sharp increase in the price of motor fuels.

The company has firmed up plans to produce 600,000 CNG vehicles in FY23 – which is more than half of a million CNG vehicles it has sold in the local market cumulatively in the last two decades. T …

2 Likes

I think Maruti is not a client for EKC, the only big player who is not a client…but again Maruti is a company which can have more sales in CNG than the others combined together

1 Like

Well, it may change in future. In concall, the Co has said that as Maruti increases its number of units sold, it may consider more CNG cylinder vendors to meet the demand. This is a huge chance for EKC. Considering the history and capacity of EKC, Maruti will give use them.

3 Likes

Could you please share the source? Or any link/report?

1 Like

India needs to offer clarity on incentives for ethanol-blending and using biogas and CNG as auto fuels as costly electric vehicles won’t be enough to drive adoption of cleaner mobility, according to Maruti Suzuki India Ltd.’s RC Bhargava. “Electric vehicles are just one part of the multiple technologies we will need to reduce dependence on oil imports and slash carbon emissions,” said Bhargava, c

Read more at: Maruti Suzuki's Bhargava Bats For Incentives On CNG To Ethanol-Blended Fuel Vehicles

Copyright © BloombergQuint

3 Likes

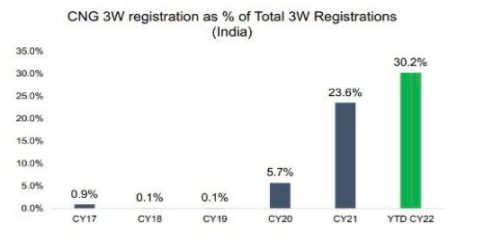

Looking at this company in detail, it feels like a lot of tailwinds in terms of upcoming CGD stations, rising CNG pumps, Car companies launching CNG variants. All these should likely benefit EKC which claims 50% market share in India. Valuation looks cheap assuming numbers sustain and it can grow its capacity 3x from 0.9 mn cylinders to 2.5-2.8 in 5 years.

But I worry about few things:

- Whether margins will sustain. Some rough calculation indicates company is making Rs3-4000/cylinder currently vs. last few years average of Rs1000/cylinder

- The business is not capital intensive and company aims to set up business overseas. A log of debt will be paid off in 6 months I think and then it may keep investing overseas. Prviously. overseas operations have struggled. They have less margins and low return ratios and earnings have been erratic. Dubai subsidiary doing OK but India operations doing very good .

3, There were operating losses in FY13-16. This seems like too long period in which company continued to make operating losses. It seems like commodity business and oversupply can cause margin disruption. Also, newer companies entering the markets seeing the current tailwinds - Dividends may be good option for excess cash that company may generate, but promoters not of the mindset of paying out cash. So capital allocation will be very important to watch hereon.

Overall, i feel cheap valuation, industry leadership and industry tailwinds make it attractive.

Discl: Not invested

7 Likes

Dividend policy is quite critical for the company as costs of current expansions in india and Hungary are not much. With annual cash generation of 300 to 350 cr they will have to pay off the promoter loans and give remaining cash as dividend. They will have to do it as investment requirement for future is not much and cash accruals can meet all capex needs. Out of EPS of 35 they should give dividend of at least Rs 25 every year from FY 23 onwards.

Company as a prudent measure should come out with a defined dividend policy.

1 Like

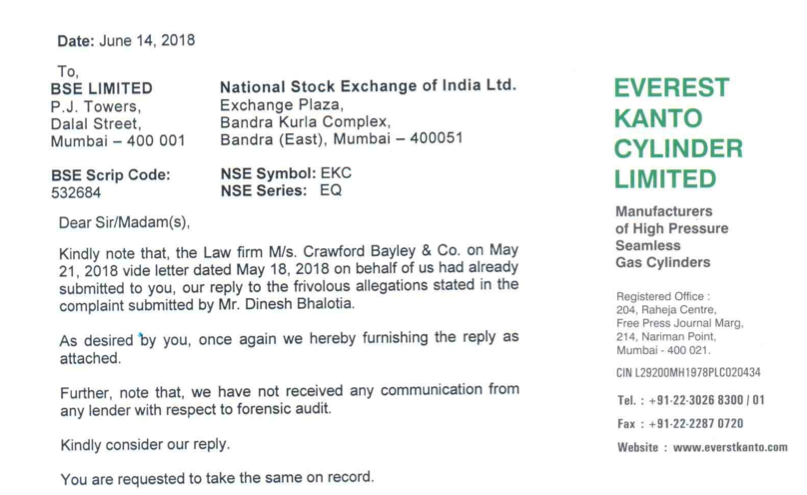

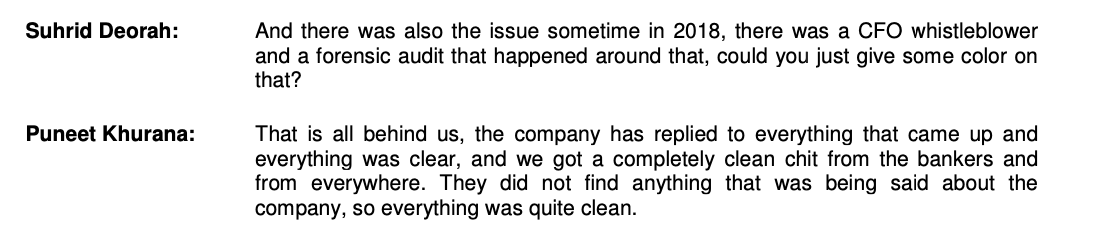

Does anybody know how these accusations were handled by the company? What was the fallout?

This was the reply submitted by management on above news

Also, they answered this in one of earning calls as follows:-

Unable to find the reply submitted by law firm Crawford Bayley. Please share if anyone have copy of that reply.

4 Likes

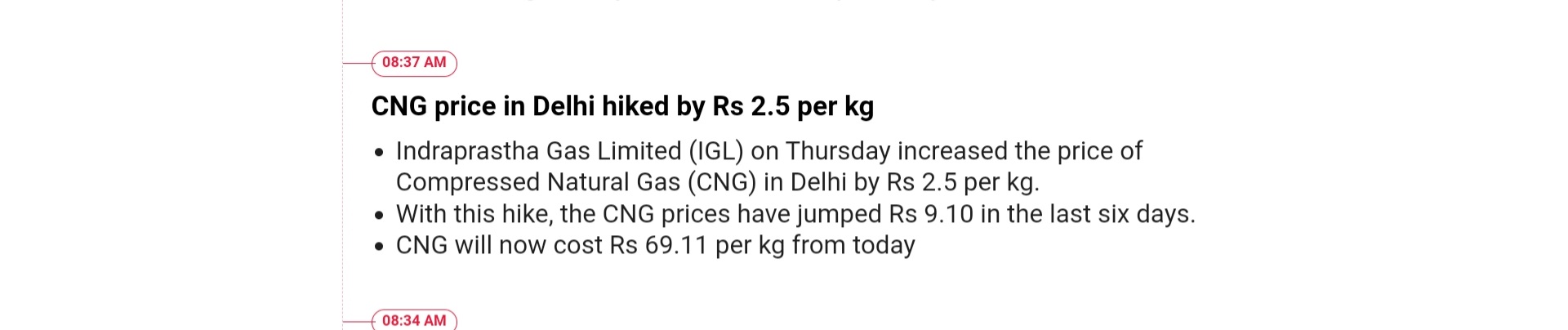

With energy crunch all around, CNG is flaring up as well, reducing the spread with other fuel options, someone using CNG was not happy with long queues in filling stations as well( metro city)

While OEM push on CNG is visible, persistent high CNG prices may make people think twice between CNG vs EV. This might be temp, Hope CNG prices cool off in coming times. These scenarios makes CNG theme proxy plays tricky.

4 Likes

Even Power prices are increasing… Lithium prices are increasing… Copper prices are increasing… already few state discoms have increased power prices and almost every one will do in the next few months. So, i feel all of them will coexist and may go up and down depending on the tech progress and raw material availability…