In all cases ROE is very high… there is huge gap in CMP and intrinsic value of the company… be patient and price will catch up… minimum price will be 400 in a few months…

Also, these countries are not new to the company. they are selling substantial volumes so there is not much market risk… which is the most important risk to be addressed… and as far as capability of setting up plants they have many plants in india and abroad so that should not be a problem!!

2 Likes

Intrinsic value cannot be very high as the use of CNG after 2030-35 is likely to drop off significantly as EV technologies gain widespread global adoption. In a DCF valuation, a lot of the intrinsic value is derived from terminal value. In case of CNG based companies like EKC, the terminal value is likely to be small.

Of course, EKC has the ability to pick up Hydrogen cylinders as another business unit when the hydrogen economy comes up. But so far how fast and at what scale Hydrogen economy will pick up is not clear and therefore will not be factored by market while arriving at intrinsic value.

7 Likes

Use of Petrol/ Diesel Vehicle will reduce however being clean fuel, use of CNG/PNG will increase. Coal Based Power Plants including CNG based vehicles will remain here till 2050 or even after that as well… Scrapage policy and strict environment norms will provide ample push for CNG based vehicles…

I feel criticism around Management’s ability to crisply reply to investor queries is slightly overdone . It is a difficult job to step in the shoes of Long term founder CEO in such a short time . I feel few quarters runway should be given before a judgement is passed on new CEOs abilities .

I saw clear intent to not only address all past CG issues but accept feedback on current concerns ( CEO accepted that Promoter loans are not good practice and I see it getting corrected fast )

I also see clear intent of Mgmt to cater to all possible potential both domestic as well as international by Brown/Green field expansions and JVs . Past mistakes on wrong Capital allocation would have definitely given sufficient insights to senior management before approving New Ventures . Only timely completion and execution stays as concerns considering external challenges coming from Varied quarters , with high demand scenario clearly visible .

In all the discussions and projections above , we seem to be missing immense CGD opportunity , which can add significant volume to demand tail wind .

I see a good earnings as well rerating potential in coming quarters

Views may be biased as Personally invested and increased allocation in current correction

7 Likes

Read more at:

Domestic gas production including CBM increasing slowly but steadily under new dynamic minister Mr Puri n evacuation under gas urja pipeline.

To all the veterans out here who are following this stock from sometime.

I am personally invested in Time Technoplast Ltd from sometime now, hence while doing scuttlebutt Everest Kanto did come to my knowledge. Some comparison here

Regd, EKC i understand there is lot of CAPEX going on with a good revenue potential, 712 Cr is what management guided. But when i read TTL, Management has guided for 5000CR by FY25 with cash level of 700cr. Current mcap of TTL is only 1600cr only. EV/sales is almost half.

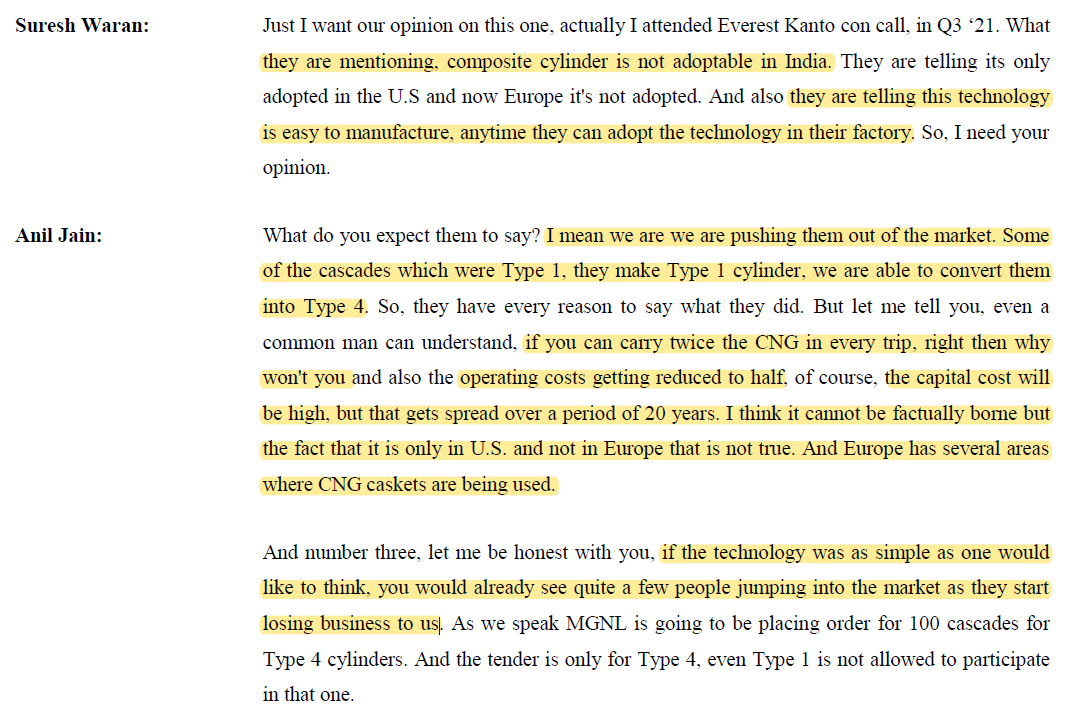

Also, in Q2FY22 concall, Late Mr. Jain of TTL said about EKC “I mean we are we are pushing them out of the market. Some of the cascades which were Type 1, they make Type 1 cylinder, we are able to convert them into Type 4. So, they have every reason to say what they did.”

I feel management of TTL seems more honest than EKC at the moment.

Any reasons why EKC may perform better than TTL?

6 Likes

Both Kanto and TTL are at ridiculous valuations with TTM PE high single digits or EV/EBITDA at mid single digits metrics, between two Kanto slightly better.

On quick glance it appears that Kanto higher margins( both GM and EBDITA), better balance sheet ( debt free, no pledging etc) and pure play CNG makes it slightly better off - one way to look at. Not necessarily only reason, mkt knows better.

If we were to look at CNG auto, both have different products( steel vs Composite), for now Kanto has its hands full with steel based orders, only time will tell when tide turns for Composite ( type 4)if it does. Obviously both mgmt will point in different directions.

As sector while things look quite rosy in near term, it equally looks super risky for longer term with terminal risks as well as tech disruptions( piped gas, EV, Hydrogen - name it). Generally sector takes precedence in overall valuations umbrella and thereafter leader, followed by others.

Kanto doesn’t have any institutional holding while TTL does. Does say something about mkt perception.

No promoter or insider buying in either counters at current levels, ( it did happen in March 20), another way to see how and where they see value. If anything TTL is not far away from those levels.

A sector with basket approach play candidate if one doesn’t see clear differentiation  . Clearly technicals and position sizing imp as well to handle wild swings.

. Clearly technicals and position sizing imp as well to handle wild swings.

Invested in EKC, studying other players.

12 Likes

Don’t think they’re too cheap. 65-70% of the Valuation resides in terminal value. If markets have taken a view that this business won’t sustain in the long run beyond this initial spurt of demand. Then these might remain at steady state PE ratio (10-15 times max). Investor stands to make earnings growth+some re-rating

Just a way of looking at what market perceives.

Disc:- sold and shifted to Piramal enterprises. Not Sebi registered

9 Likes

- Maruti see share of CNG going to 22% from 15%

- Tata expects CNG and EV to be both at 20% each, Jan 22 EV sales 2900+, CNG 3000+

Hyundai is not far behind in CNG push.

All three together makes up most of Volumes in industry, writing is on wall about CNG adoption atleast for forseeable future( 5+ years high growth), with OEM biggies and Govt betting on it, add 10000+ CNG stations infra, sizable savings one gets running on CNG, Atma Nirbhar aspects…doesn’t appear all stakeholders can be wrong to bet on it for a short duration. Unless we manage to build a country wide EV infra which many Developed nations are still working on it, having started decade back.

Spoke to a local retrofit dealer, Huge demand there as well( infact stock out for Kanto, Rama was available).

Numbers+ Newsflow is present, narrative is missing. Market in its own wisdom, will assign narrative and deserving valuations in due course. Even low teen PE rerating and growth gives a doubler.

11 Likes

Appreciate comments from @sharemarketgen_ (now deleted) and @Dev_S .

As far as Yash Pakka is concerned, i haven’t studied the company well enough,10x increase in revenue is too optimistic. I think management of TTL can be believed given their track record. For them it will be increase of 1500cr from existing 3500Cr.

I have friends working in Indian Oil, HPCL and have heard good comments regarding type IV cylinders and TTL has bagged some orders as well.

They have orders from Tesla regarding batteries as well, though revenue potential is small.

As Dev mentioned, basket approach is something i would want to play here and look to add EKC.

1 Like

The ecosystem for CNG is now scaling up after 20 years of its entry in India. Gas infrastructure companies that are investing thousands of crores of rupees would possibly have understood the potential. Participants on this forum believe that EVs will come and take over in three years flat. More a fashion statement than reality…

4 Likes

Time technoplst received 7.35 L Type IV cylinder of RS 170cr order from IOC today… Repeat order will follow. TTPL has also announce expansion for another 1 million capcity. IOC and other govenment companies slowly will repalced steel cylinder but it takes 5-7 years to reach that stage. Total demand 80 million cylinder /year.

3 Likes

Hinduja flagship commercial vehicle manufacturer Ashok Leyland said that CNG will be a big driver for its alternative fuel vehicle portfolio.

CNG’s share of total industry volume of commercial vehicles has constantly increased and as per data from the Society of Indian Automobile Manufacturers (SIAM), CNG trucks form about 10 percent of the market with the remaining 90 percent being diesel.

“In last two years, the delta between diesel and CNG increased which is leading to fast movement towards CNG. For shorter routes, CNG will become popular. The infrastructure like CNG fuel stations has also simultaneously built up,” said Sanjeev Kumar, head, MHCV, Ashok Leyland.

The company as part of its green mobility initiatives, has put in place a strong team to focus exclusively on alternate fuel technology that uses low carbon.

The company has entered the CNG CV goods carrier space with the launch of the E-Comet Star ICV (intermediate CV) CNG truck range.

The CNG trucks the company launched are available in two gross vehicle weight (GVW) options—16.1-tonne and 14.25-tonne—and three CNG cylinder options.

Kumar said that the transition to electric as a fuel for heavy tonnage vehicles like trucks will take some time while there will be faster adoption for CNG. “While electricity will be more prominent in buses, shifting to higher tonnage vehicles will take some time. I think as a progression after CNG there will be Liquefied Natural Gas (LNG) before electric,” Kumar said.

The primary reason, Kumar feels, is the development of infrastructure for CNG vehicles in various cities. “In various cities, the government has opened tenders for multiple tenders for city gas distribution companies. CNG infra is now present in multiple states. The pace of shift to electric will depend on the creation of such infra,” he said.

There are demands from private companies and state transport units as they also shift towards alternate fuel. Recently, the company has delivered 10 BS VI CNG buses to India’s largest airline for operation at New Delhi Airport.

But Ashok Leyland is simultaneously working on multiple alternate fuels other than CNG like electric, LNG, Methanol.

The Hinduja group recently launched a new electric vehicle firm, Switch Mobility by merging the electric commercial vehicle operations of Ashok Leyland and the former Optare Company as it seeks to secure a leading global position in net zero carbon buses and light commercial vehicles.

“We should be prepared and be ready that as and when the time and technology demands, we should be ready,” Kumar said.

EKC FOCUS IS ON COOMERCIAL CV SEGMENTS WITH ASHOK LEYLAND N TATA MOTORS ITS MAJOR CLIENTS.

6 Likes

How is the receipt of an order for composite LPG cylinders by Time Technoplast relevant to this thread which covers developments related to Everest Kanto, the largest manufacturer of CNG cylinders?

1 Like

TTPL is also going for CNG cylinder and gaskets and slowy replacing steel cylinder within few years. TTPL capacity of 1 million steel cyliner capacity which now tranforming to LPG/CNG cylinder and expanding. TYPE IV Cylinder are safest as they are FIRE PROOF. EKC will have tough competition in future…

1 Like

In your previous post, there was no mention of the IOC order being for LPG cylinders. Had to check the corporate announcement to understand that. TTPL has been claiming to capture the entire CNG cylinders market for a few years now, wish them all success.

2 Likes

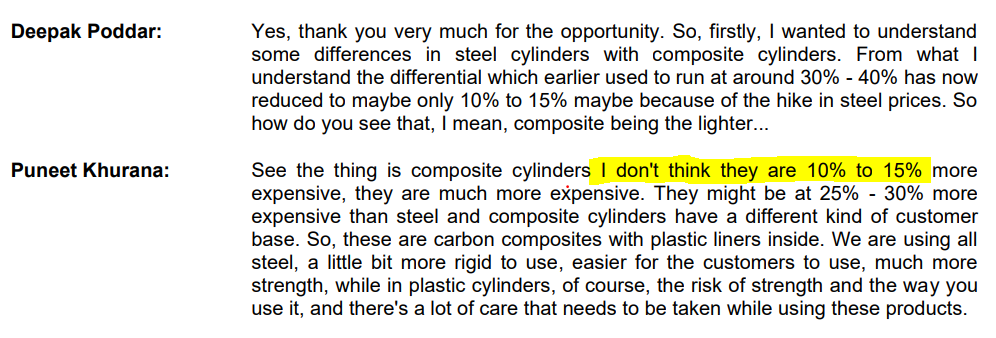

Time Technoplast management says 10-15% difference:

Everest Kanto saying 25-35%:

Do we have somebody on this forum with information of current market prices and their really difference?

4 Likes

In case somebody missed adding interesting comments by Time Technoplast on Everest Kanto in their Q2FY22 concall:

5 Likes

For the latest LPG tender, price quoted was ~2400. I don’t know latest pricing for steel cylinders.

3 Likes