Katalyst wealth tweeted about EKC among their latest reco.

2 Likes

Credit rating update from Care

The rating rationale behind the upgrade ( and the company’s customer list ) is worth reading !

Regards,

Abhijit.

[Discl : Invested ]

13 Likes

| standalone | Consol | ||||||

|---|---|---|---|---|---|---|---|

| q1 fy 23 | q4 fy 22 | q1 fy 22 | q1 fy 23 | q4 fy 22 | q1 fy 22 | ||

| 110% | 113% | ||||||

| sales | 271 | 376 | 247 | 380 | 478 | 335 | |

| cost | 227 | 286 | 168 | 331 | 396 | 257 | |

| margin | 44 | 90 | 79 | 49 | 82 | 78 | |

| 16% | 24% | 32% | 13% | 17% | 23% | ||

| 134% | 168% | ||||||

| RM | 161 | 206 | 120 | 217 | 260 | 129 | |

| 59% | 55% | 49% | 57% | 54% | 39% | ||

| 150% | |||||||

| power | 15 | 15 | 10 | ||||

| 6% | 4% | 4% | |||||

| others | 35 | 48 | 24 | ||||

| 13% | 13% | 10% | |||||

| emp | 8 | 8 | 8 | ||||

| 3.5% | 2.8% | 4.8% |

3 Likes

Raw material is the problem… with steel prices coming down in June/ July next quarter will be much better.

1 lac additional cylinders capacity in Q2 (brownfield expansion) so volumes should also increase.

3 Likes

While I am optimistic, reduction in steel price, if contract based, may not reflect in Q2.

From Q1-22, There is increase in revenue from India and US/Hungary. UAE is flattish.

2 Likes

Poor results?

India business EBITDA has sharply come down, subsidiaries have done well this Q.

1 Like

This quarter is extremely bad and lot of it can be attributable to lower margins due to elevated RM prices . Bigger concern is lower than expected sales in domestic . Need to deep dive to understand this , since they have always been claiming more than 90-95% capacity utilizations . Ideally they should have passed on certain high RM cost and that should have reflected in their Toplines too . Reasons for lower domestic sales number are key

4 Likes

Reason for low domestic sales can be increasing cng prices

1 Like

Just an observation

Results were quite alarming not only on front of margin compression but Q-Q de growth in domestic sales also.

Lesson learnt : a company with a past track record of poor corporate governance(even though it might be improving) is one bad quarter away from limit down (which is compounded by liquidity issues in small cap companies)

3 Likes

What is the probability of results improving next quarter? Considering the demand and high entry barriers in the industry.

If we look rationally, the results were not so bad that a down circuit is warranted. It is something else which is leading to loss of confidence in the company. While earlier corporate governance was questionable, the management did came across as trying to make amends. However the perception has still not changed and probably worsened.

Due to this, I have got out of my entire positions today. Generally I have seen that anything which goes circuit down takes a lot of time to come back. With that perspective, I exited the counter. However I will keep it in watchlist and monitor the progress of the organization and market verdict as time passes.

Regards,

Nikhil

1 Like

But if we look closely the FII/FPI have increased their shareholding by almost double in the June quarter showing their keen interest in the stock …that too at a time when overall they had reduced the portfolio.

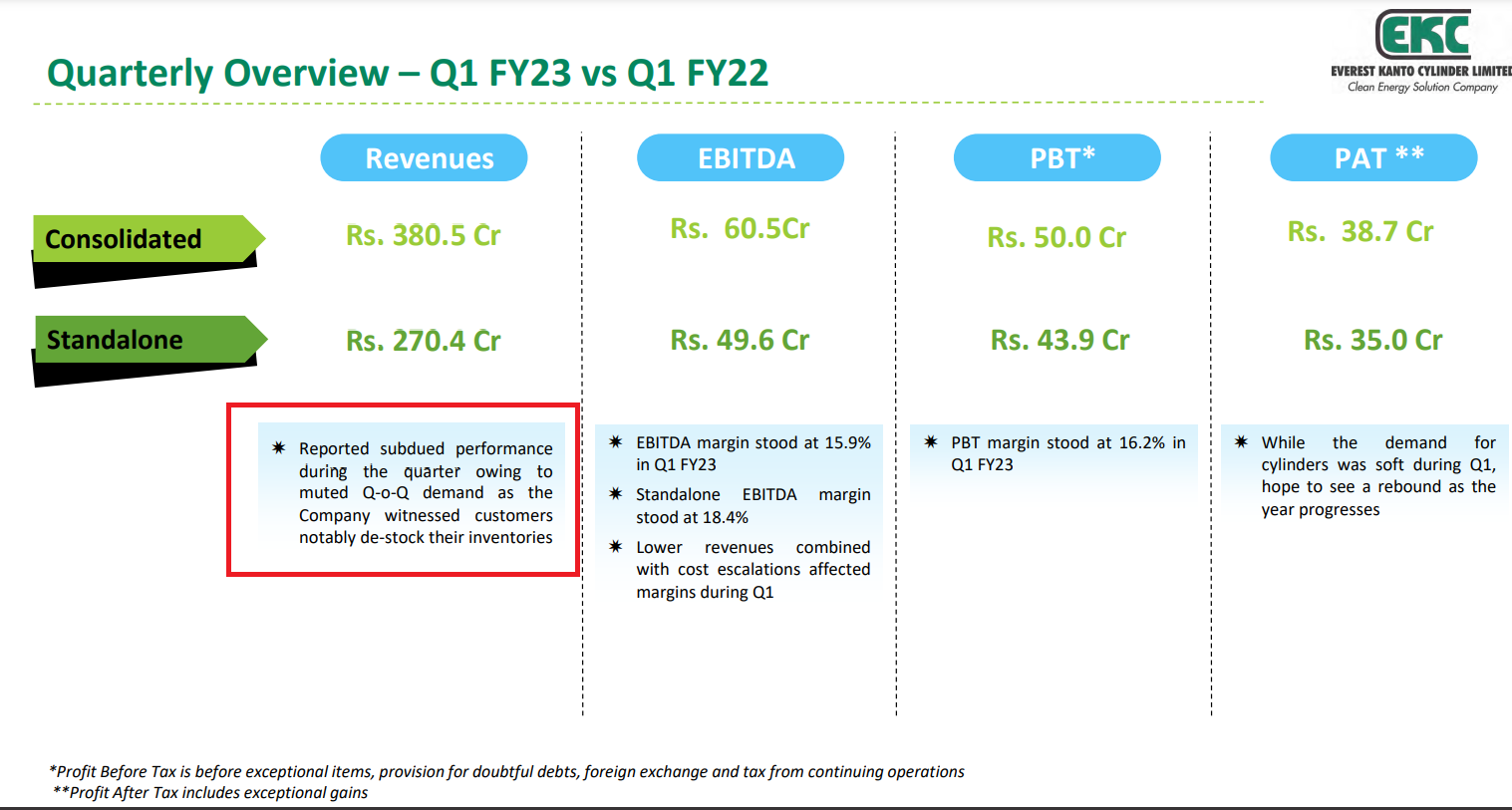

Key points to note from the presentation:

-

Reported subdued performance during the quarter owing to muted Q-o-Q demand as the Company witnessed customers notably de-stock their inventories

-

Lower revenues combined with cost escalations affected margins during Q1

-

While the demand for cylinders was soft during Q1, hope to see a rebound as the year progresses

1 Like

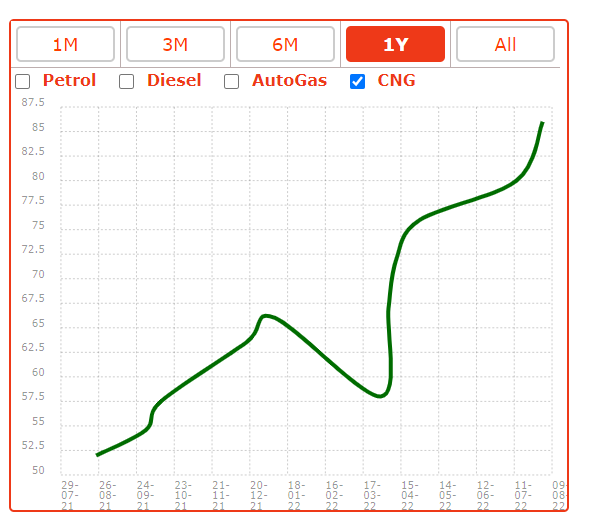

Chart for CNG prices in India. Clearly unprecedented increase. Rather than “hope”, it would have been honest and transparent - had the management provided the trend of demand they are seeing in Q2 so far…

2 Likes

Few months back,I had pointed out that this could lead to some volume dampening in the short term.

3 Likes

The oil ministry has ordered the diversion of natural gas from industries to the city gas distribution sector to cool CNG and piped cooking gas prices that have shot up by 70 per cent on the use of imported fuel.

Less than three months after it ordered the use of costlier imported LNG to meet incremental demand for automobile fuel CNG and household kitchen gas PNG, the ministry on August 10 reverted to an old policy of primarily supplying domestically produced gas for city gas operations.

The allocation for city gas operators like Indraprastha Gas Ltd in Delhi and Mahanagar Gas Ltd of Mumbai has been increased from 17.5 million standard cubic meters per day to 20.78 mmscmd, officials said.

The increased allocation will meet 94 per cent of the demand for CNG to automobiles and piped cooking gas to household kitchens in the country.

Previously, about 83-84 per cent of the demand was met and the remaining was met through the import of LNG by GAIL, they said.

Use of domestic gas instead of imported fuel will bring down the cost of raw material and ease CNG and PNG rates, officials said.

The move follows a massive jump in CNG and PNG prices in the country in the last one year as operators used costlier imported LNG. CNG prices in Delhi went up by a massive 74 per cent (from Rs 43.40 per kg in July 2021 to Rs 75.61 per kg now) while PNG prices rose by 70 per cent (from Rs 29.66 per standard cubic meter to Rs 50.59 per scm).

Natural gas is the raw material that is used for CNG and PNG. This gas comes from fields such as Mumbai High and Bassein in the Arabian Sea. As the domestic production of gas is insufficient to meet all the requirements, the fuel is imported in the form of Liquefied Natural Gas (LNG) in ships.

To promote the use of cleaner fuel, the government in 2014 included the City Gas Distribution (CGD) sector on the top priority list for receiving gas from older or regulated fields of state-owned ONGC and Oil India.

The CGD was put on a ‘no cut’ priority sector and allocation was made twice a year – in April and October – based on consumption data of the previous six months.

The ministry made such full allocation in March 2021 and thereafter, in May 2022, issued an amendment to the 2014 supply guideline to state that incremental demand over and above the last year’s level would be met through imported LNG.

State-owned gas utility GAIL was asked to average out the price of domestically produced gas and imported LNG every month and supply gas at a pooled price.

This pooled price for August came to USD 10.5 per million British thermal unit. In comparison, the gas from regulated fields of ONGC is priced at USD 6.1 per mmBtu (it was USD 2.9 last year when CNG operators started meeting additional demand through imported LNG).

LNG rates shot up this year, leading to a hike in CNG and PNG prices, officials said.

Spot or current LNG prices have more than doubled in the last few months to about USD 40 per mmBtu.

With industry saying that CNG was losing an edge over petrol and diesel because of the price hikes, the ministry relented and agreed to increase the allocation of gas from regulated fields, they said.

The allocation for CGD was increased by cutting some supplies to LPG-making plants of GAIL and petrochemical units of ONGC, officials said.

City gas operators complained against the May 2022 guideline as it meant using high-priced imported LNG, which led to frequent CNG and piped natural gas price hikes, they said.

After the latest amendment, the gas price will come down to USD 7.5 from USD 10.5, officials said.

“Supply for domestic gas to the CGD entities shall be made only up to the quantity available and allocated to GAIL for CNG (transport) and PNG (domestic) segment instead of 102.5 per cent of consumption level in the previous quarter,” the August 10 order of the ministry said.

5 Likes

Just finished listening to the EKC call - they have highlighted sharp drop in CV OEM volumes in June. I checked Tata Motors concall, the same has been clearly called out in their presentation and earnings call. In the LCV segment, CNG volumes have come down from 40% in FY22 to 26% in Q1 FY23 due to lack of price arbitrage between CNG and diesel. Tata Motors will keep a watch on how CNG v Diesel demand evolved and they are not concluding anything yet basis 1Q numbers.

Ashok Leyland in its earnings call has said that its seen some shift of LCV demand away from CNG into EVs also due to CNG prices.

So the short to medium term demand scenario for EKC in the auto CNG segment may be challenging. LNG supply chains are complex and if Europe and Russia can’t strike an agreement on resuming overland gas supplies before this winter, the LNG pricing in global markets may remain disrupted for an extended period of time as Europe buys more LNG.

Coming to the concall, several investors expressed their displeasure over lack of and poor quality of information/disclosures made by the company regarding its results - for e.g. a simple data on Cylinder volume trends or industry wise breakup of demand is not given by EKC. I agree with the same, its quite frustrating as an investor because with the lack of data, negative surprises are 100% possible like this one.

After having tracked this company for over a year now and listened to Management in 4-5 concalls, I am not able to trust the promoters here. I have learnt over this quarter, that trust in Management is paramount as an investor and its better to get out leaving potential money on the table but having peace of mind, if one can’t trust the Promoters. The company may be in a value zone right now in terms of price, but poor Managements can often reduce value, making companies value traps.

Disclaimer: This is not investment advice. Everybody is entitled to their personal opinions and I am sure there are many people here who remain bullish on EKC and the promoters and that’s perfectly fine. One reason I put down my thesis and my call in writing is also so that I can look back in the future and take learnings from my thought processes. I reserve the right to be 100% wrong.

18 Likes