Does this fall in stock price is due to stock correction or there is some fundamentals changes in company(except resignation of CEO)??

Is it good to buy at this point??

Does this fall in stock price is due to stock correction or there is some fundamentals changes in company(except resignation of CEO)??

Is it good to buy at this point??

Management is one of the biggest fundamental for any banking stock.

This is super subjective question! I have added more of equitas to my holding.

Disc: invested

Across forums, everyone is saying that fundamentals has not changed and as per the con call CEO will stay till the time successor is appointed. So what exactly is happening with the stock? Is there something which is being missed by all?

I think market is discounting the resignation of vasudevan as if there is no future for the company and it was a one man show. Also they might be anticipating rise in npa due to upcoming recession. So these 2 factors are being discounted in my opinion. And when discounting happens it happens to extreme just like when discounting for future growth happens it happens to extreme It’s like in short term market is like a voting machine. same thing happening in my opinion.

Disclosure: invested and added recently in the fall.

Planning to add more once see further improvement in fundamentals like npa numbers (ratio as well as absolute), incremental roe, provision coverage ratio (which is quite low now), growth. so I’ll wait for q1fy23 results.

I remember that they have done restructuring of loans. Is there any effect due to restructuring on stock price? Is there any thing which we are missing?

Restructuring usually done when borrowers are stressed in finance. So to avoid them becoming npa it’s done. Luckily moratorium given was for 6 months from October 2021. So effect of restructuring on npa has already happened. That’s why fundamentals are improving. Usually restructured loans are future source of npa. but for this case they are not anymore. See the previous discussion in this forum.

The upcoming AGM has interesting proposals:

Reappoint Mr Vasudevan as the MD & CEO for 3 years with an increase in compensation ~40%. The last comp revision was done in 2018 when he was reappointed.

Change the structure of the board from single non independent director - MD&CEO to 3 non independent executive directors - MD&CEO and 2 Whole time executive directors. The proposed 2 whole time directors are being internally promoted - Mr. Rohit Gangadharrao Phadke & Mr. Murali Vaidyanathan.

This is significant because irrespective of who becomes the next MD, the two new whole time directors by position will have a good chunk of the MD’s responsibilities.

How does this work? Has he agreed to the extension and forgone / delayed his philanthropic aspirations?

He had agreed to be with Equitas till they find a successor. Till then he will be the MD&CEO and the board will keep reappointing him for 3 years.

I’m still unclear. He had said he will continue till they find a successor, yes. But is the timeline for finding the successor of the order of magnitude of 3 years or more? Never heard of that before.

It could be a day or month or years, we don’t know that.

Mr Vasudevan’s tenure was ending and the board is following the standard procedure of reappointing him. The reappointment has always been of 3 years.

Whenever the search completes he will resign and the new person will be appointed by the board.

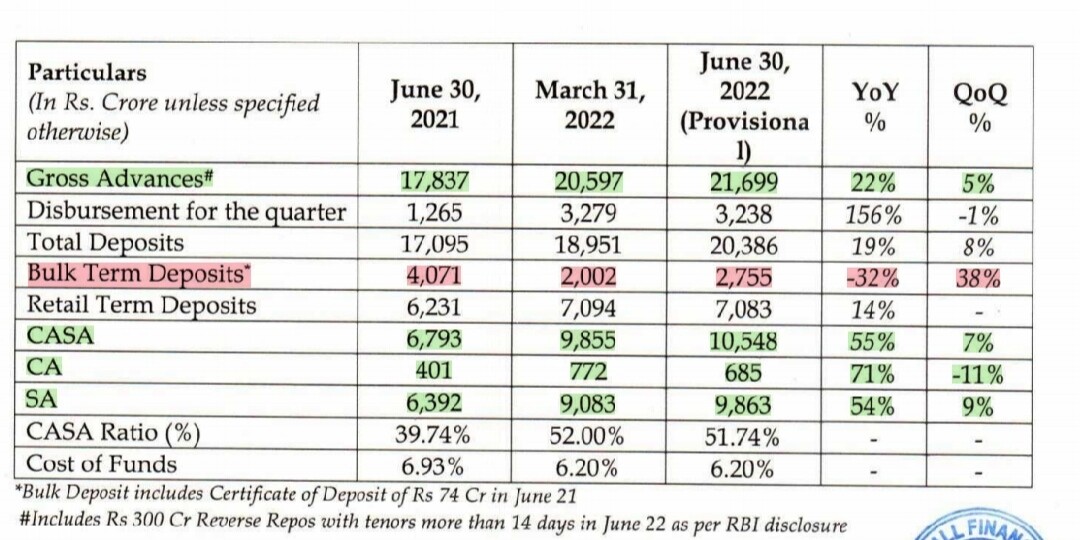

Growth is coming back. 5% sequential growth in advances! However there is sequential rise in Savings account and degrowth Current account. Although cost of funds is constant qoq. Bulk term deposits also increased very sharply qoq.Anyway the most important thing to look for is NPA numbers. waiting for result.

Disclosure: Invested. avrg price: 114.

How exactly do we read into “Includes 300 Cr, Reverse Repo with…”

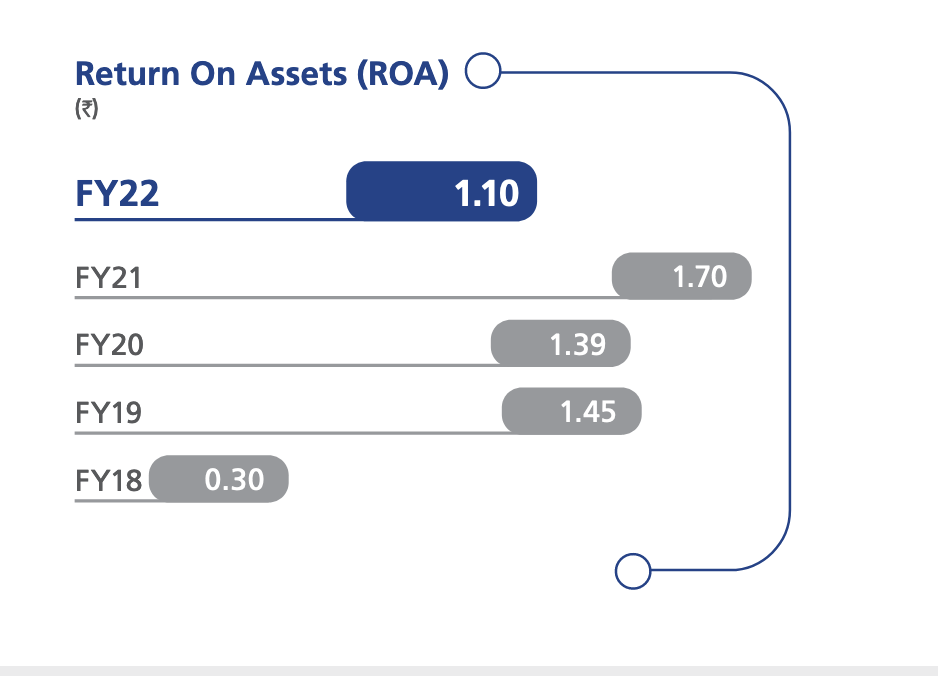

@Sameer_Upadhyayula Major reason is higher provision in FY22

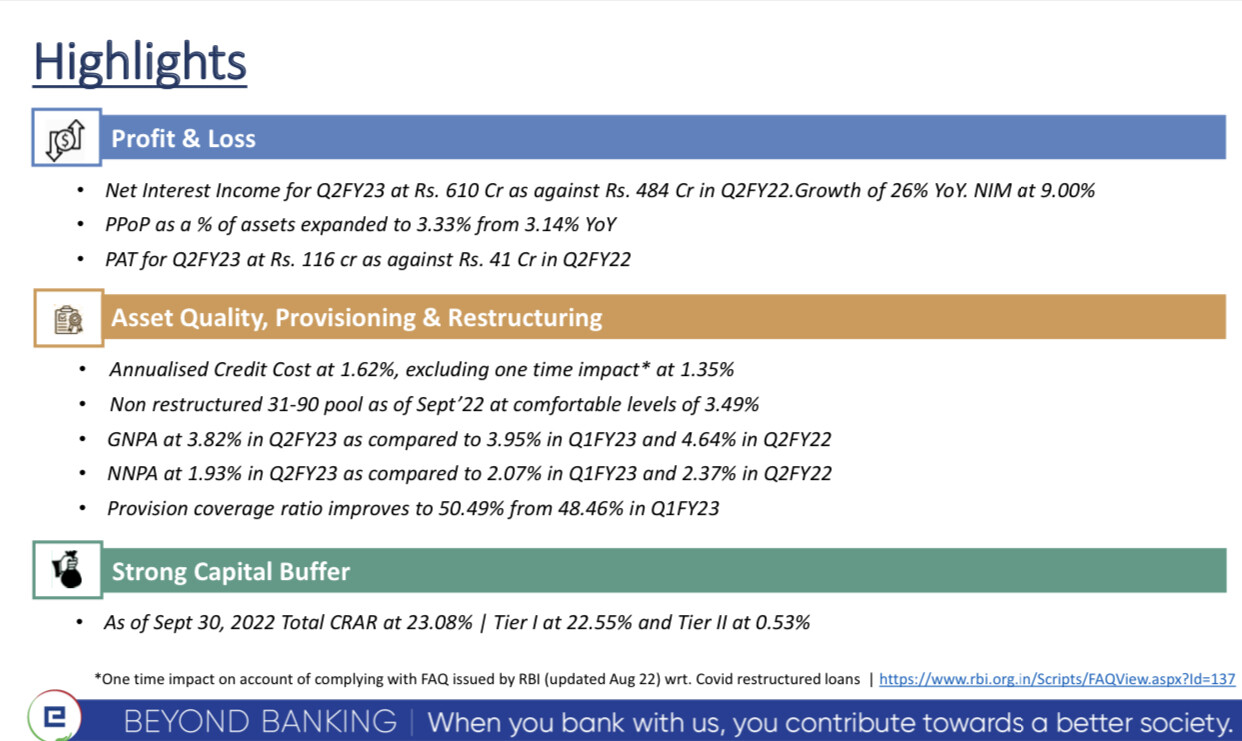

Notes from Presentation & concall:

Opex increased 412 cr. Last quarter: 356cr. The opex would have been 443cr as there was a one time reversal of 31cr for some employee provision. The increased employee cost is due to wage inflation. Increase in other expenses is largely due to technology investment. Opex will not stabilize as we continue to invest but it will not substantially increase the cost to income.

Credit cost is 140 cr against net advances 21.6k cr. Last quarter credit cost was 123cr.

Restructured book size reduced from 1500 to 1200cr. Out of 1200cr:

Fresh slippage for this quarter: 296cr. It was 408cr last quarter. Slippage from RL is ~ 156cr & non RL 140cr.

High writeoff of 130cr. Last quarter was even higher ~200cr.

NCLT ordered for a meeting with shareholders which is scheduled for 7th september. Merger process will be complete few months before the guided date of March 2023.

Out of 286 cr of RL NPA from last quarter, 95 cr was written off.

Credit cost guidance is less than 2%, target is 1.5% for the year which is possible as per the mgmt because q4 credit cost can be less than even 1% as there won’t be RL book. [I personally doubt this would be possible, but who knows…]

Q2 provisioning should be less than q1 and lesser thereafter. Mainly because of one time increase in provisioning for RL book. Management also commented that the high provisioning is really not required because loss from recovery is less than 40% for CV & almost 0 for SBL as SBL is backed by property.

CoF is not expected to rise despite the rate hike.

Equitas had a similar restructured book for 1 to 90 DPD last quarter. We can expect around the same amount of fresh NPA coming from the pending restructured loan book in the next quarter.

disc: invested. Will continue holding because I agree with the management that as the RL book going down we will see significant increase in ROA & ROE in the coming quarters.

Good results from Equitas SFB. Snippets from the investor presentation. Hoping for the merger to be completed soon.

I think it will change nothing short term. They get the approval to buy but does that mean they are actually going on and buying? Not sure. Could not get this cleared yet. Do they already hold some of Equitas SFB, I have not researched.

DSP MF currently owns 8.5% of Equitas Holdings. Any entity has to take permission to hold more than 5% stake in a bank that is why probably they are taking this permission. Because after the reverse merger DSP is likely to hold more than 5% stake in the SFB due to its 8.5% stake in equitas Holdings.

Will be interesting to see the change in equitas’s CASA now that they have reduced the savings account interest rate after a long time.