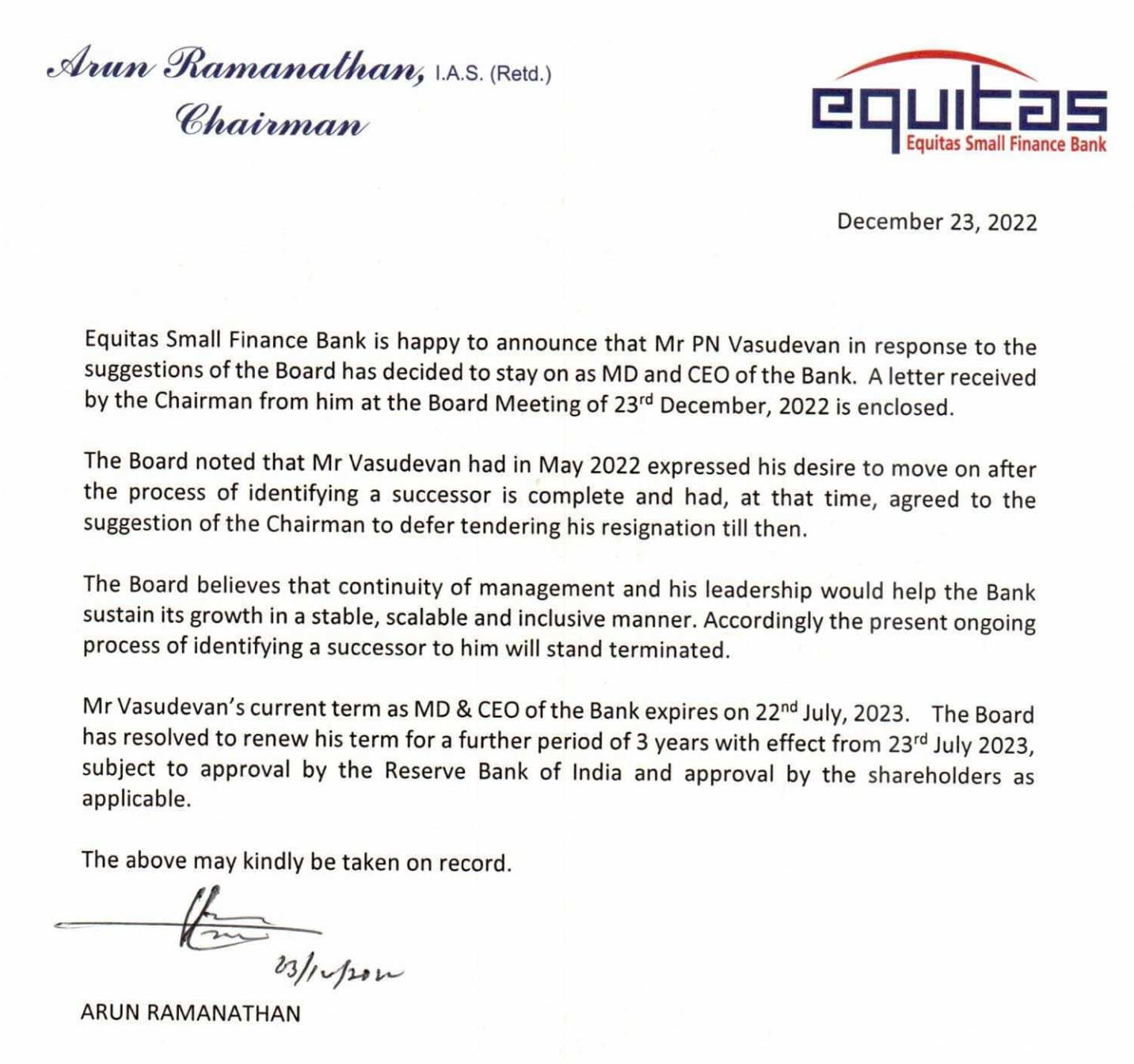

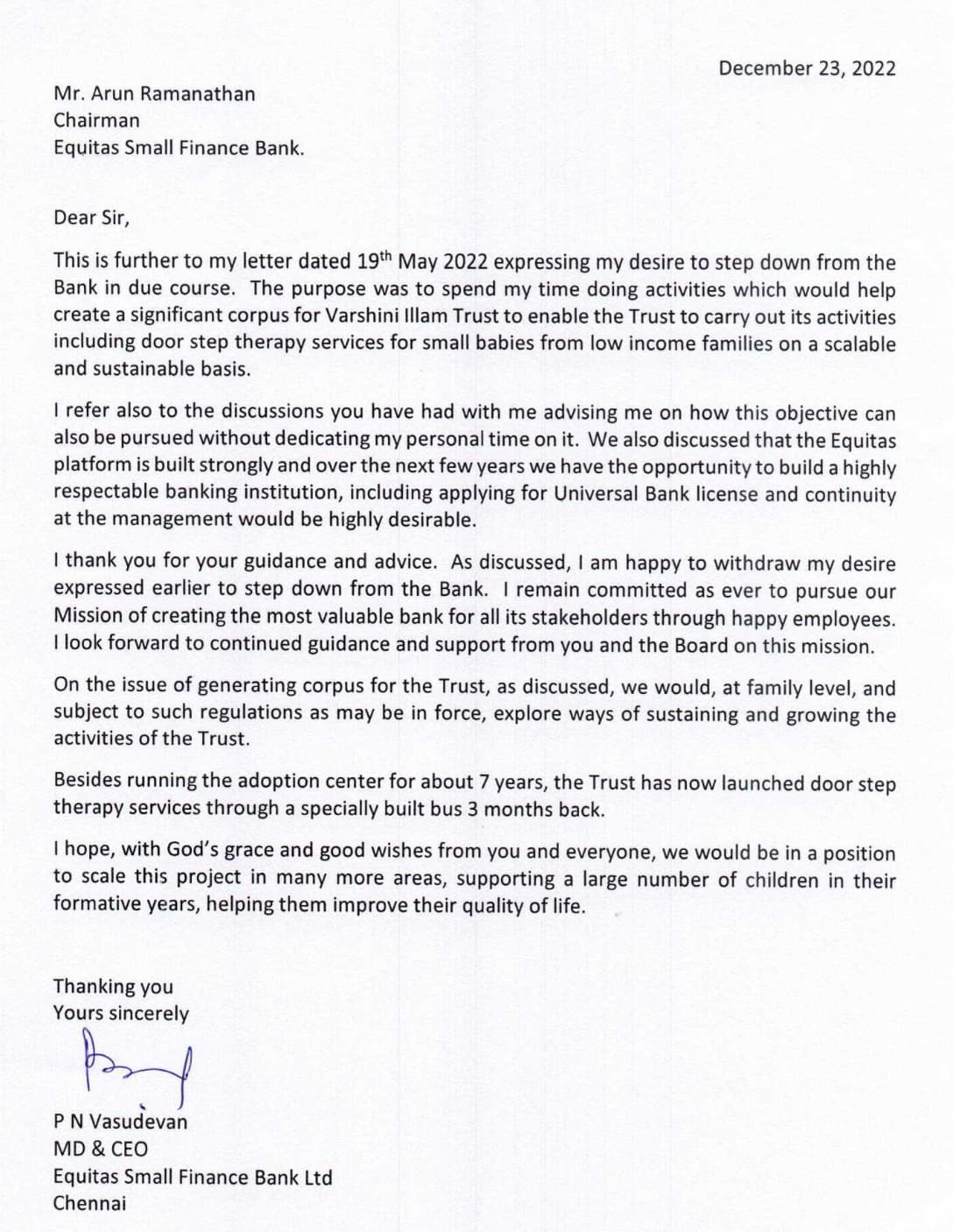

PN Vasudevan decides to stay.

14 Likes

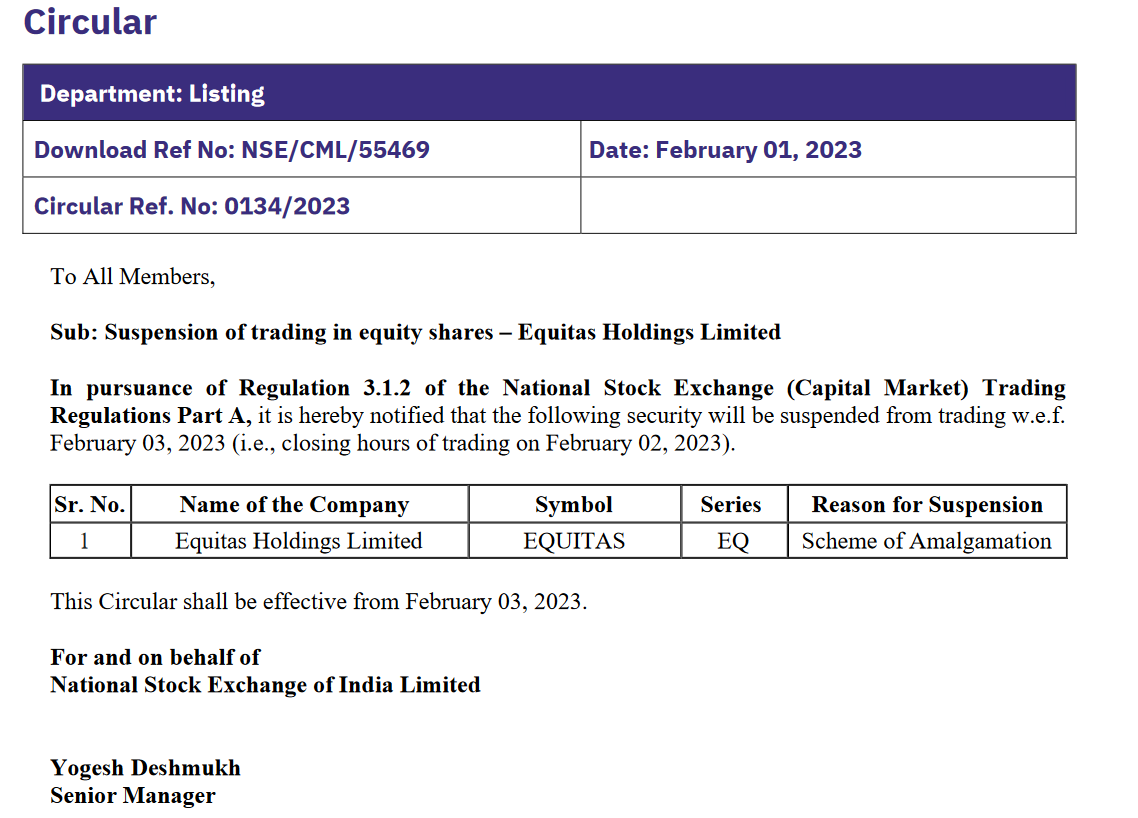

On recent announcement it was stated that there would be hearing by NCLT FOR merger deal.

It was due on 21 December was I was not able to see / find any new updates and what was the result anywhere.

And also not able to see the due date of merger.

Just want to know have I missed something or these results are not generally released or there was some update of change of date etc.

In recent management interview MD PN Vasudevan told that they have submitted all the required documents before the bench. Now the decision is pending with them. It is expected to come near end of January 2023 .

5 Likes

When can we expect the newly allotted shares to start trading?

2 Likes

Listing is expected by end of Feb 2023.

Source: Equitas SFB concall opening remarks

6 Likes

Usually 30-45 DAYS from date of delisting.

2 Likes

Who told you it has been credited? Why unnecessary panic? Have patience. You will receive email from your broker and nse probably one or two before it starts trading on exchanges.

Received the credit of Equitas SFB shares, but I guess may take a couple of more days before it can be traded.

EQUITAS SMALL FINANCE BANK LIMITED#EQUITY SHARES OF RS.10/- LISTING /TRADING APPROVAL AWAITED

1 Like

Expecting a fall with fresh supply of shares hitting the markets in the next week. Lets see.

3 Likes

The credit of shares can take between 30 - 45 days from the record date. You’ll receive an email from CDSL once the shares are credited to your demat account

Record date was February 03 2023. So the credit should happen anytime in the next couple of weeks

Posting here as on the other thread, normal profiles can’t post. Good numbers

Equitas Small Finance Bank Q4FY23 Provisional Business Update:

Gross Advances for the quarter at Rs. 28,061 Crs, up 36% YoY and 13% QoQ

Disbursements for the quarter at Rs. 5,917 Crs, up 80% YoY and 23% QoQ

Total Deposits for the quarter at Rs. 25,381 Crs, up 34% YoY and 8% QoQ

Please find below link to view the press release:

15 Likes

1 Like

Hi Ishmohit,

I am a student of SOIC. Just small question about Equitas ? How much visibility they have beyond TamilNadu also are their VF, SBL or HF customers different from MFI customers ?

From credit ratings report Jul 22,

In terms of geographical diversity, 54% of Equitas SFB’s portfolio is housed in Tamil Nadu which makes the book susceptible to local socio-political issues and this, in CRISIL Ratings’ opinion, remains a challenge for the bank.

This is a always a weakness according to number of credit ratings reports.

1 Like

Interesting interview on how the bank will look like going forward:-

-

Guiding for AUM growth of 25-30% per annum.

-

In couple of years AUM should reach 45,000+ crores.

-

NIM’s- as new products get introduced with slightly higher ticket size, overall NIM might come down a bit due to newer products. Overall spreads will remain the same. NIMs should be close to 8.5% in 2-3 years. NIM is a factor of product mix that we have. New products like personal loan or credit cards etc.

-

Microfinance will come down to 14% over the next few years.

-

Present in small commercial vehicles as these address the local environment. Think it’s less risker than financing long haul commercial vehicles.

-

GNPA is at pre covid levels. Credit cost will come back to the pre covid level at 1.2-1.25% level.

-

Fairly under leveraged, going forward increasing leverage will help ROE to increase further.

-

Restructuring was high as customer segment was such. Haven’t seen much pain from RSL book, today it is below 1%. Against RSL book, have 88% covered under provisioning.

Disc: no reco. No transaction in last 30 days.

18 Likes

-

Post the decrease in SA interest rates done in Dec22, the SA deposits had a de-growth this quarter, as expected. It has dropped from Rs 10,021Cr to Rs 9758Cr. Overall the customer deposits have continued to rise. CASA has dropped from 46% to 42%.

-

COF have increased by 0.21%. Most likely the savvy depositors either transferred their funds to other accounts or booked a TD with Equitas.

-

Either way it will be Equitas’ loss here. It’ll reflect either in lower deposit growth or higher COF.

I don’t quite get the strategy here. If anyone here understood their strategy, do share your views.

2 Likes

- Vasudevan PN said he will continue for the whole of his remaining 8 yr tenure. 3 of which have been approved by RBI.

- Will apply for universal banking when RBI opens that window.

- WIll launch Personal loans this FY and Credit cards in next FY. (will take time to build up) (This will not sacrifice the 18-20% unsecured loan book)

- Should sustain growth of 25-30% for this year and some financial years to follow.

Even the management might be looking at equitas holding thread to be renamed to Equitas SFB on Valuepickr. ![]()

![]()

![]()

Disclosure: Makes around 35% + of my investments

7 Likes

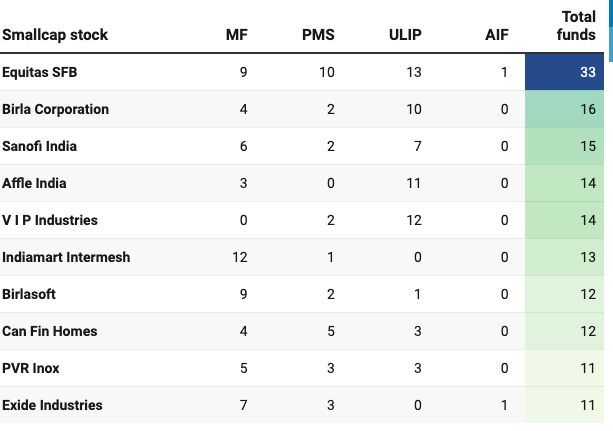

Equitas is #1

1 Like

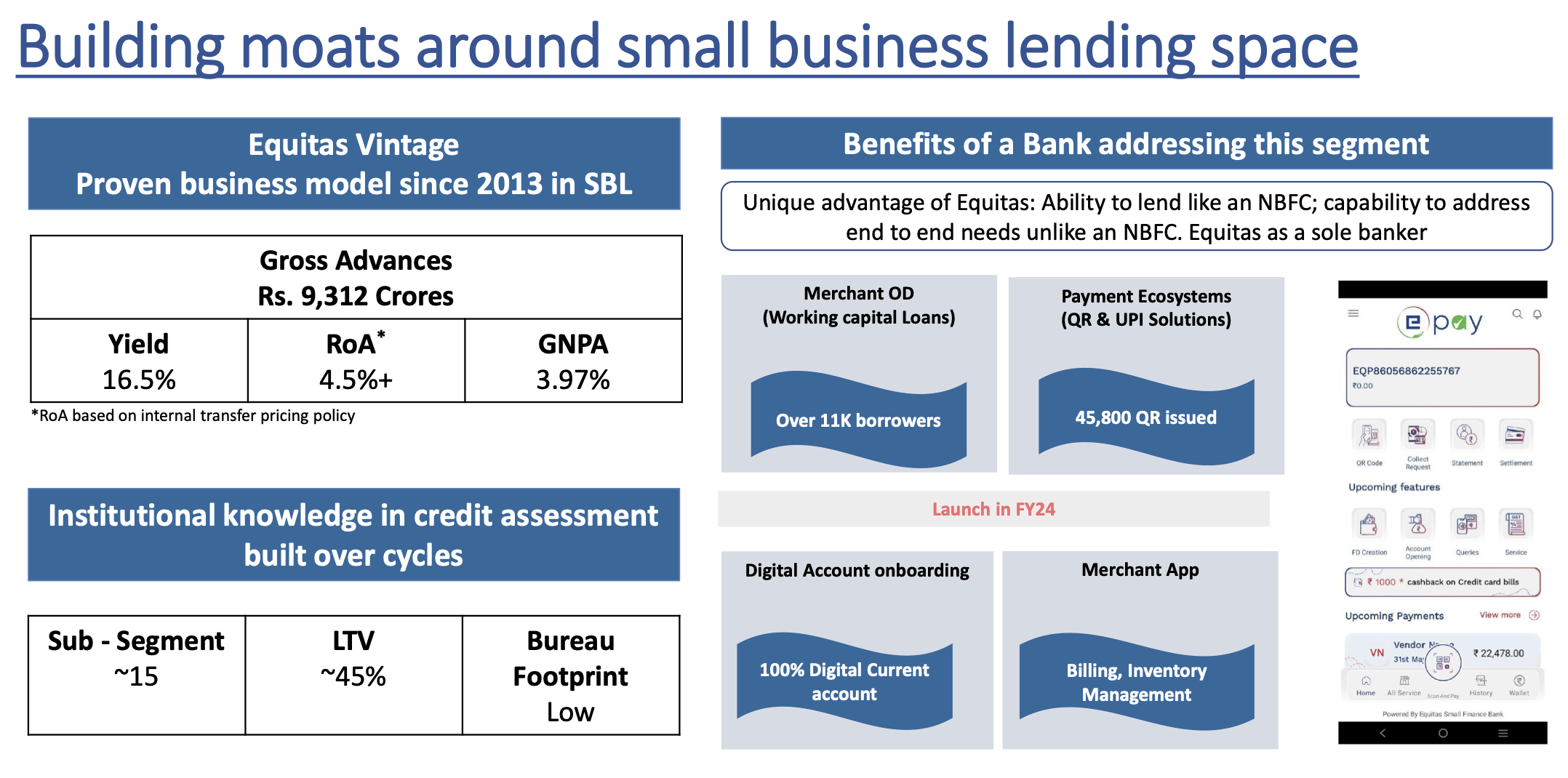

Unit Level Economics of Equitas SFB in different products:- (Posting here as other thread isn’t open)

- Small Business Loans:- These loans contribute 36% to the entire book, and have grown at a CAGR of 44% between FY15-FY23.

This Business unit does ROA of 4.5%+.

Average ticket size of these loans is below 6 lakh rupees.

These loans are high opex in nature but are extremely profitable as seen by the ROA. This is similar to what FIVE star finance or Aptus do. Only real difference is- that EQUITAS has much lower cost of funds vs the other 2.

Average Credit cost from FY19 till date has been 2% in this division and this includes the covid wave. In FY23, GNPAs were 3%+ in this business unit. As the end borrowers have just recovered. Overall, RSL loans and GNPAs have fallen back to pre covid levels in Q4FY23.

Average GNPA in this division has been 3.14% vs Industry average of 4%+.

Yields in this segments are close to 18%.

2. Microfinance:-

This business division used to be 28% of the mix in FY18 and this has fallen to 18% in FY23. Management has guided to bring MFIN below 15% over the medium term.

This has been a deliberate strategy, as EQUITAS was primarily a Microfinance institution. Mix of Microfinance has fallen over the last 10 years.

This is indicated by their Yields, as Yields in unsecured loans are the highest. Overall Yields have fallen from 21% in FY18 to 17% as the mix of Secured asset class has increased as a % of the book.

Mircofinance Unit Economics:-

ROA of 4-5%. Average ticket size remains small at Rs.27,000 and Credit cost is 2.5%. Yields on these loans are 21%+.

- Vehicle Finance:- This segment contributes 25% to the overall loan mix.

In the Vehicle finance book, 71% of the loans are given to Small & Light Commercial Vehicles.

22% of the loans are given to Medium & Heavy Commercial vehicles.

This business unit had poor profitability in last 2 years due to covid related stress. ROA was sub 1.1% and Yields on these loans are close to 16%. High in opex, as indicated by 5.5%, cost to assets ratio. Recovery of Profitability in this unit can cushion the overall ROA going forward.

- Housing Finance:- this contributed 10% to the overall Loan Mix. These loans have an average ticket size of less than 10 lakh rupees. This is similar to what AAVAS, Aptus and Home first do.

Yields on these loans are :- 10.3%.

This a fully secure loan product. Opex in this business is very high, as this business unit has started scaling up just recently.

The bank is also going to launch other products like credit cards and Personal loans.

Closing thoughts:-

-Bank has consistently started hitting 2% ROA in last 2 Quarters. And the incremental ROE has gone above 15% in Q4FY23. If these numbers sustain with asset quality sustaining, things can become interesting.

As AU with 8% unsecured loan book+ 92% secured book,1.8% ROA is at 4.56x Price to book.(165 rs is the latest BVPS)

Equitas has re-rated a bit but given the Book Value per share is at 45 rs (post merger). There could still be some room looking at the changes in incremental profitability.

Currently, only 2 Small finance Banks have transitioned to secured products. Others are still majorly in Microfinance or IGL loans.

Disc: Not a recommendation to buy or sell by any means. Sources used:- Investor presentation, QIP Document, Philip capital report, and Kotak Report.

51 Likes