Increase in NPA was expected because 9% of their book was restructured 1700 cr. Moratorium given was 2-3 months from September 2021. So I think whatever NPA was supposed to come from restructured book has already come.

1 Like

As per lower pcr ratio the bank used to have 45% pcr im 2018 too so this is not the first time.

But they need to increase their pcr ratio. if no more stress comes from restructured pool then their actual pcr ratio becomes 75% (400 cr standard provision+200 cr for restructured book)/800 cr gnpa.

need to listen to the q4 concall for present status.

1 Like

I did not aware of that 200cr separate provision… Yet pcr below 50 bothering

How much of the book is still restructured?

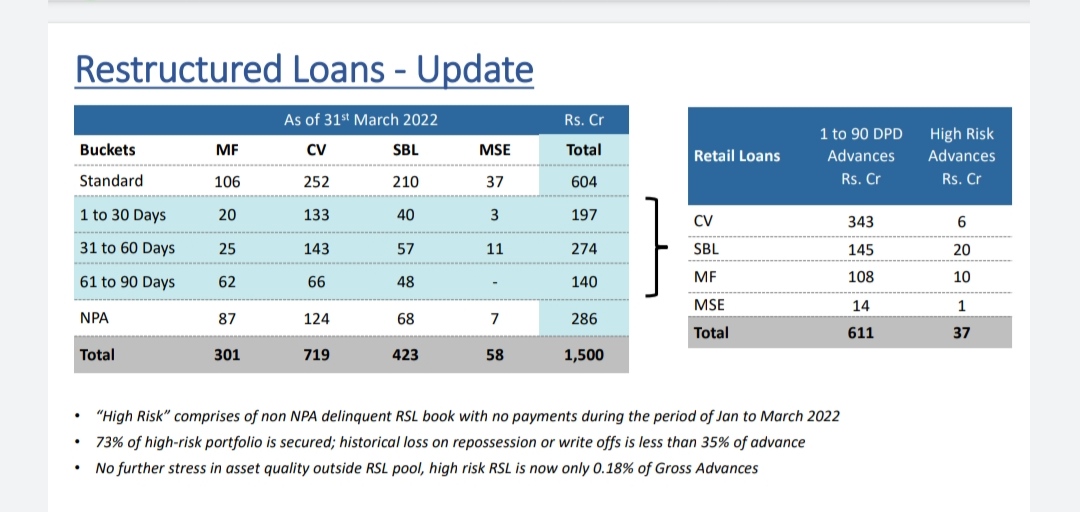

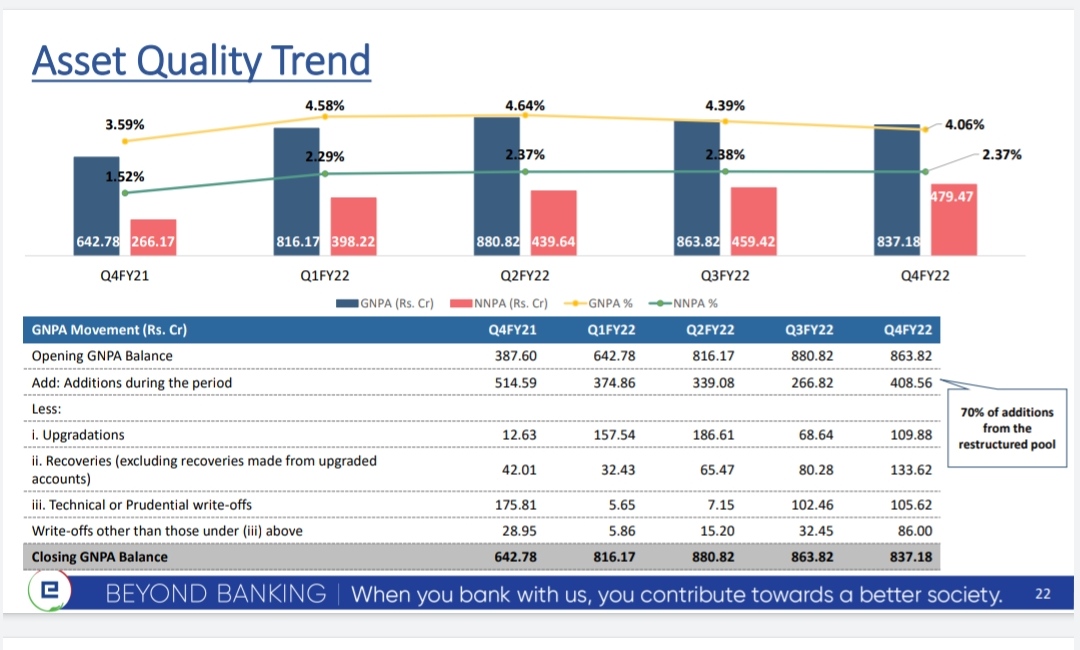

60-90 DPD is 140 cr this can slip into npa in this quarter. this is from q4 presentation

restructured book is 1500 cr

one more thing I found about this bank is usually every q4 they do a lot of writeoff to clean the book so gnpa reduces usually.

1 Like

Why just 60-90d? till 30th June we have 90 days. Any loan from 1 to 90 dpd can slip into npa.

Thanks, I understand how provisions and writeoff work.

My question is more on if a loan is secured then what amount does the bank lose?

Say there is a 100cr secured loan but it needs to be written off. I don’t think a provision of 100cr will be used for it because bank will be able to recover a portion of the loan through the security it holds. What % is the bank typically able to recover is my question.

Yes it can happen but recoveries and upgrades also happen simultaneously. So we should see net slippage.

1 Like

It depends on the type of underlying asset which is secured. if it’s a gold loan you get 100% money back. If it’s some old junk machine you won’t get any money back. but no body gives loan on whatever is the underlying asset value. Lets say there is 100 rs gold jewellery then you can get 75 rs maximum loan. this is called loan to value (ltv ratio). Higher the ltv lower is the margin of safety.

2 Likes

Q4Fy22 concall notes:

- 15% of the loan book is linked to repo rate

- credit cost of non restructured book is 1.25% in q4 on annualized basis.

- Billing for all of the restructured book was in q3 so whatever customers were unable to come out of stress has already become npa. Remaining non npa restructured book we believe there will not be further deterioration.

- Expecting 30% growth this year. Last year most of the sales team was deployed on collection because 9% of the book was restructured. now they are redeployed for growth.

- Out of 1500 cr restructured book 611 cr is 1-90 DPD and 286 cr is npa. out of that 611 cr, 37 cr has not paid a single emi in jan-march but 17cr of those 37 cr has paid one emi in april. so restructured book is now behaving like main book. so redeployed sales team for growth, because this year our whole focus was on collection. now since we are focusing on growth we should be able to grow the book by 35%.

- 593 cr total provisioning. 358 cr npa provision(used for calculating pcr)+ 235 cr standard provision including restructured. specifically for restructured book 152 cr.

- 90bps drop in yield on sequential basis: Diversifying into formal lending. They need lower interest rate. this will not compromise our nim and pat.

- PCR reduction is optical. loans which are 100% provided are getting written off. Targeting 60% pcr.

- credit cost guidance for 1.5% in fy23. without restructured book causing any npa this quarter credit would have been 1.25% which is business as usual.

- 61-90 DPD Being 140 cr: They have paid something inspite of going through 1st wave 2nd wave. so that tells clearly that their intent is not bad. that gives confidence that they will pay. because they have seen the worse.

- 1% sequential degrowth in interest income inspite 5 % sequential loan book growth: most of the aum growth happened in march month and also due to disbursement to lower yielding products catering to formal economy.

- there is a 1 yr monitor period for restructured loans. if they do not slip into npa then they will become standard

- effect of RBI increasing repo rate for entire fy23 on cost of funds: 10-15 bps.

- On a conservative basis fy23 exit roa should be 2% because operating leverage kicking in is clearly visible and credit cost is also reducing.

- Operating leverage: 10-15 Branch addition this fy. most of the growth will come from digital.

8 Likes

Its a premium content. please share the summary

@Souresh_Pal Sorry, Didn’t realise… I could read it when I posted and now it’s behind paywall…, I remember the holding company discount was mouthwatering 70% now dropped to 25%… but still persists… news doesn’t move the needle for Equitas SFB shareholders…

Wondering what others clearance are pending… if someone can share would be of help in fixing my timeline

PN Vasudevan, Founder MD and CEO has resigned to take charity work. Does look genuine.

Hope the bank does not go the way Ujjivan did.

Captain of the ship steps down… Not good to see

1 Like

Post the resignation of the CEO, how do you evaluate Equitas Holding?

- Demerger should go as per the plan

- What about succession planning?

Stock has been going down since the news but do not see any fundamentals being changed.

How long does existing CEO plans to stay?

there should be no impact on demerger.

PS Vasudevan (Current CEO) will stay till successor is appointed and takes over, post that he would continue on the board in non -executive position

3 Likes