Equitas Holding ltd.

CMP: 158 Marketcap: 4233 crore

Background:

Equitas Holding ltd. (EHL) is diversified NBFC offering loans to individuals and small & micro enterprises, which are economically weaker with low incomes and are underserved by the formal financing channels. It is the 5th largest microfinance company that provides micro loans and also offers vehicle finance, Small and Micro finance and housing finance to leverage on its existing customers.

A youtube link of EHL

Basically EHL is a holding company and has 100% stake in following:

-

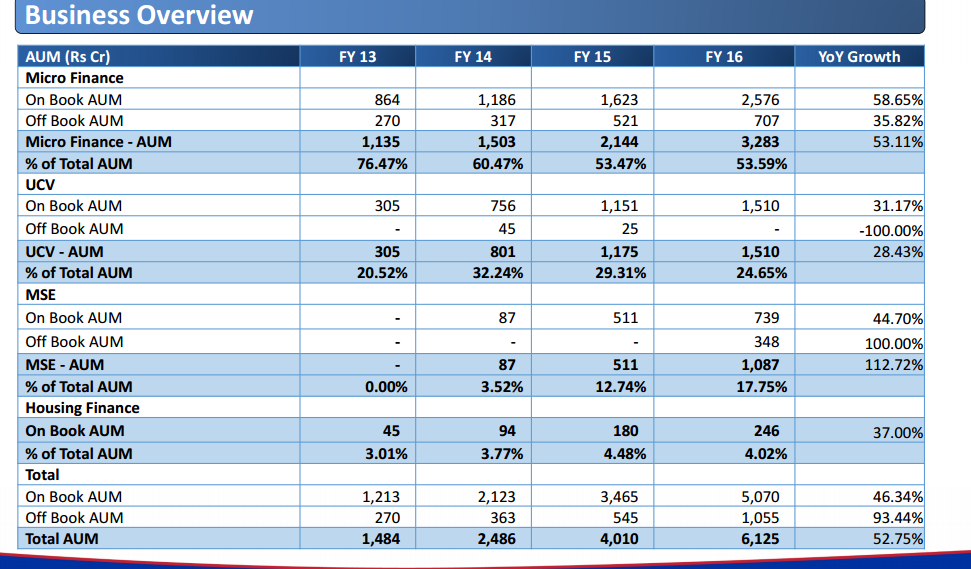

Microfinance business:

a. Offers loan with a ticket size of Rs 2000 to Rs 35,000 mainly to women entrepreneurs

b. Average ticket size is Rs 10,500 with 14 – 28 days collection cycle.

c. The whole process is based adopted by international microfinance companies where women are the borrower and repayment is at the centre.

d. Passbooks are issued to customers and centrally issued pre-printed stickers are used for each loan account evidencing cash receipt.(prevents fraud)

e. Equitas follows Grameen Model for MFI customers. -

Equitas Finance ltd.:

a. It offers loans for vehicle finance and micro & small enterprise loans.

b. Registered with RBI under asset finance company.

c. The main motive is to diversify this finances under unsecured lending business

d. This business has the highest Net interest margins as cost of funds is lower and the yields are the highest at nearly 20%.

e. Higher margins are possible due to higher yielding products like used cars. -

Vehicle finance business:

a. Operates through 134 branches in 13 states with major revenues comes from Tamil Nadu, Karnataka and Maharashtra.

b. To achieve operating leverage, EFL operates from the same branches of micro finance business.

c. Customers are sourced via field staff from their networks and relationships with transporters through various means including telecalling and direct marketing activity in transport hubs. It also enters into arrangements with dealers of used commercial vehicles.

d. Credit appraisal involves personal interview, guarantor, inspection of vehicles and document check.

e. It offers loans to Used CV borrowers and small fleet operators with ticket size in range of Rs 1.5 lakhs to Rs5 lakhs with tenure of 3 – 5 years

f. Asset quality at 150 dpd remains in line with industry levels but coverage ratios remains poor. -

Micro & Small Enterprise business.

a. Primarily focused to self- employed individuals operating small and micro business typically in urban and semi-urban areas.

b. Loans from Rs50,000 to Rs 500,000 with credible asset backing with evaluated cash flows.

c. Average ticket size is Rs 200,000

d. Major businesses from Tamil Nadu (77%) and rest from Maharashtra, Pondicherry, MP, Karnataka, Gujarat and Rajasthan. -

Housing Finance business:

a. Provide housing finance loan to self-employed individuals to higher income microfinance group with proper track record.

b. Ticket size 2 lakhs to 20 lakhs and loan tenure of 7 – 20 years.

c. Average ticket size of 5.70 lakhs with 2.6 lakhs for micro housing and Rs 12 lakhs for housing segment.

d. Non housing business with 21.5% and is under limit prescribed by NHB.

e. EHFL offers its housing loans through 14 branches across Tamil Nadu, Karnataka, Maharashtra and Pondicherry with most of these branches located in existing microfinance and vehicle finance branches.

f. Asset quality has been deteriorating but low coverage ratio (a concern) -

Small Finance bank:

a. EHL is amongst the few companies who got in principle license from RBI in OCT 2015 to set up a Small Finance bank.

b. This SFB will help EFL from restrictions made by NBFC.

c. There are some weak points against SFB:

i. Out of 75% lending to be given to Priority sector lending (PSL), 40% should be given to RBI specified sectors i.e. Agriculture where the company doesn’t have any strengths.( they will breach it by Gold loan offering and would create a new product offering.

ii. EHL would have to invest heavily into technology upgradation rapid branch expansion and augment employee base to support operations mainly in liability side.

iii. Equitas will have to depend on deposits to fund its growth as inter bank borrowings restrictions will come in and as it builds its CASA franchise it would have to depend on bulk borrowing and maintain high SLR & CRR. -

Equitas Technologies pvt ltd.:

a. Development of a technology platform for freight, logistics, carriers and related services which matches demand with supply and wherein various such vendors and customers can be brought together for further fulfilment of sales and services between them on a real time basis.

b. Brand name “WOWtruck”

c. It has 23 branches as of 31st march 2016

d. WOWtruck will be developed in various phases of which 1st was completed be end of December 2015

e. This would be completed by early Q2 FY17

Bearish View Point

-

Microfinance loans unsecured; susceptible to credit risks

a. Economically weaker sections, customers are at times unable to or may not provide accurate information about themselves. Further, in case of emergencies like death or major illness, microfinance customers may find it difficult to pay EMIs on time. These factors may lead to increased levels of NPAs. -

Heavy dependence on southern states, particularly Tamil Nadu

a. The operations have extended to other states like Maharashtra, Madhya Pradesh, Karnataka, Rajasthan, etc, branches and products continue to be concentrated in Tamil Nadu or factors such as a slowdown in sectors such as MSE, the company may pronounce effects on financial condition and results of operations. -

Scalability concerns due to regional presence

a. EHL being a strong player in Tamil Nadu and other southern regions, scalability of the leading business will be a concern due to regional presence. Also, with an SFB licence, better liability management will be needed to scale up resources.

Share holding pattern:

April 30, 2016(investor presentation)

Promoters

Corporate 13.8%

Mutual Funds 25.6%

FII 44.2%

DII

Others 14.0%

Market cap Free float 2077.65

P/E

SBI Mutual Fund recently bought

- Valuation:

o Ratios:

Particulars 2015 2014

Book value 43.54 102.13

ROA 2.98% 3.25%

ROE 11.19% 12.25%

ROCE 13.49% 13.99%

Fixed asset turnover 11.37 9.87

Receivable days 670.87 696.70

Inventory days 0.00 0.00

Payable days 33.96 33.93

Cash conversion cycle 636.91 662.77

Total debt/Equity 2.59 2.49

Interest cover 1.55 1.60

o P & L A/c:

Mar-16 Mar-15 Mar-14

SALES 1110.93 755.06 482.43

SALES% 47.13% 56.51% 70.98%

EBITDA 705.85 465.82 308.44

EBITDA% 51.52 61.69% 63.93%

NET PROFIT 167.14 106.99 74.32

NETPROFIT MARGIN 15.04 14.17% 15.41%

NET PROGIT GROWTH 56.22 43.96% 132.98%

EPS 6.21 4.48 3.99

Disc: Not invested