You should definitely find in AR it is a subsidiary financials are also there

What will happen to received money by selling Wowtruck. Will they paid to shareholders?

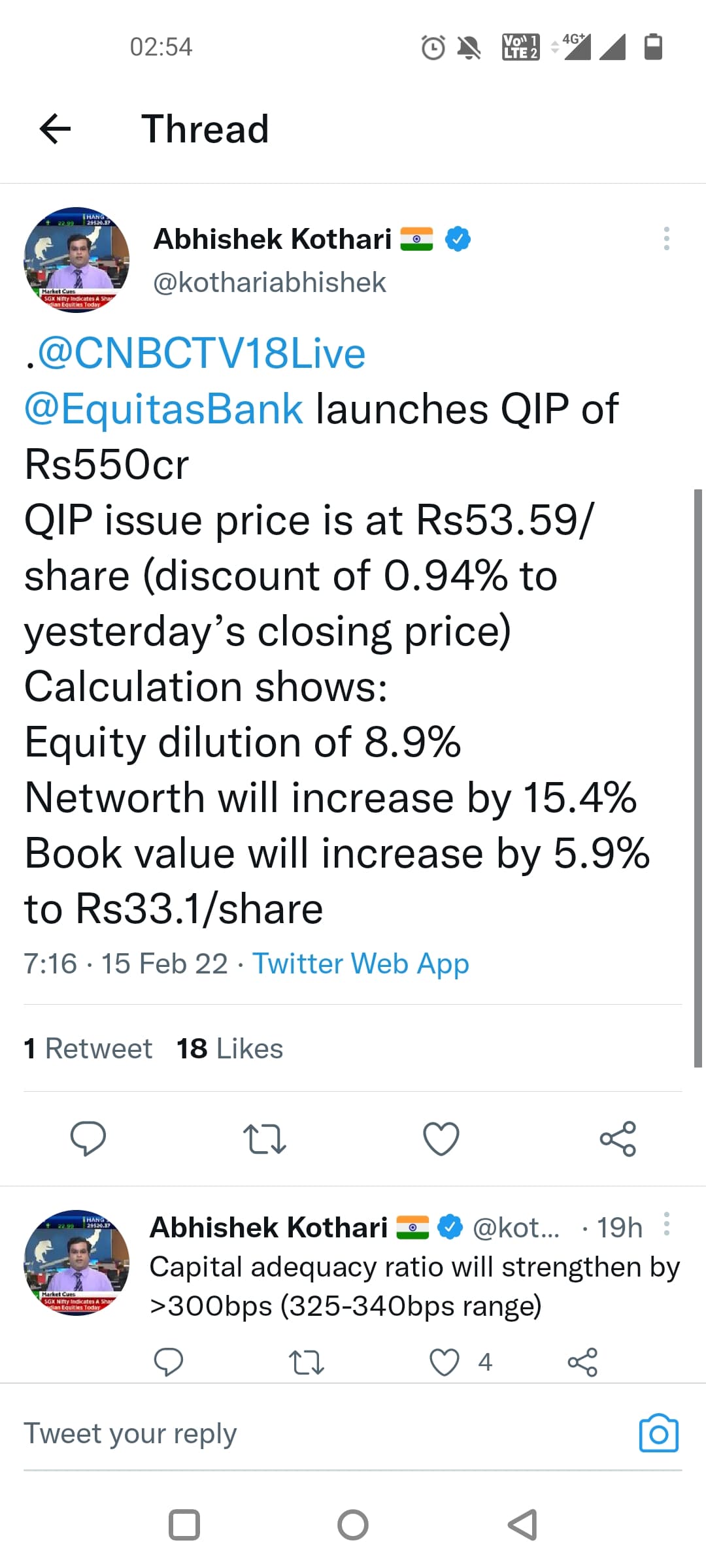

Does this QIP change the merger ratio?

2 Likes

no. Because, irrespective of this QIP, the worth of EH’s shareholding over ESFB remains the same.

It will, as they have a lesser % of outstanding shares than what they did before QIP.

Only in case Equitas holdings had bought shares in QIP in same proportion as their current holding %, the merger ratio would have remained the same.

Lets take a example.

Cpmany A - parent company

Company B - Child company (A holds 80% of B)

Total shares available in A = 800

Price of each share of A = Rs. 10

Market cap = Rs. 8000

Total shares available in B = 1000

Price of each share of B = Rs. 10

Market cap of B = Rs. 10000

A’s holding value in B (800 shares) = Rs. 8000

If deal was announced as 1:1 merger

Now QIP of 200 shares announced

Total shares available in B = 1200

Price of each share of B = Rs. 10

Market cap of B = Rs. 12000

A’s holding value in B (800 shares) = Rs. 8000

Here in case irrespective of QIP, the value of parent company’s stake in child remains same. Then why would a merger ratio change?

Correct me if I am wrong, have no expertise in this area

4 Likes

Thats because previously A owned 80% of B, but after QIP, A owns only 66.7% of B. So what A might get in terms of number of shares of B will undergo a change

How come it will change? Swap ratios are based on what you own. Not based on companies total outstanding shares.

1 Like

If we just look at qip it is just equity dilution to raise money.

So the swap ratio will remain the same and the stock price is also adjusted after qip by looking at their equity raising issue.

In very basic terms, they have done QIP to increase the pizza size so you will own less in percentage but your value will remain the same.

Also as I am looking they might be selling their tech arm before the reverse merger so what will they be doing with that money buy more stake or will do dividend.

3 Likes

Does anyone was able to get what valuation can there selling subsidiary will be and can it even be substantial as their sales will be around cr180 if the market there starts to stabilize.

I personally see that the only peer at least in the startup world is blackbuck and in their past funding and looking at current sales the overall market cap to sales is around 6 times yes wow truck is asset-light and blackbucks also do a lot more things so can still assume it to be around 6 only so we can assume when it sells at the same price and be around 180*6=1080cr and if we do all discount I still see it selling not less then 700-800 cr that is around 20-25% of current business.

So they might get significant cash that they can pay as buyback, dividend, or even increase their stake (Regulatory issues might come as it is a banking business).

Note:- I was only able to see that they don’t list wow truck revenue especially so I think other revenues is all into this so just looked there later and 1-2 past consolidated revenues

I am personally starting to invest in it so can be a little biased.

2 Likes

Good analysis over small finance banking.

And also ignore the targets as always.

5 Likes

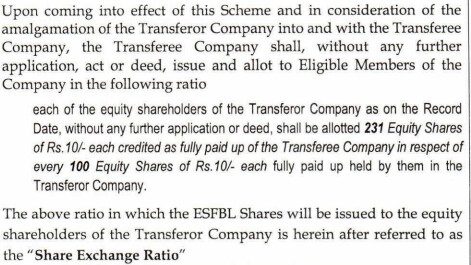

merger ratio decided.

5 Likes

It was already decided last year.

1 Like

Continuing the steady decline the cost of funds is down to 6.43%.

4 Likes

Good work on liability continues, it will outshine once it find the fix for growth in quality loan book.

2 Likes

Data from the investor presentation. Good stuff:

- Cost of funds further down to 6.20%.

- Casa at 52%. Also retail % of term desposit

- CRAR at 25.16%. So much room to grow and increase the RoE which is at 12.2%.

- Slight reduction in GNPA to 4.06%. Net provisioning remains almost the same.

- High disbursement rate. Increase of 15% QoQ, 29% YoY. This results in 4.6% increase in QoQ gross advances.

- Opex isn’t increasing. Note that the decline from 240 to 209 cr is due to reversal of excess grauity and leave salary in this quarter.

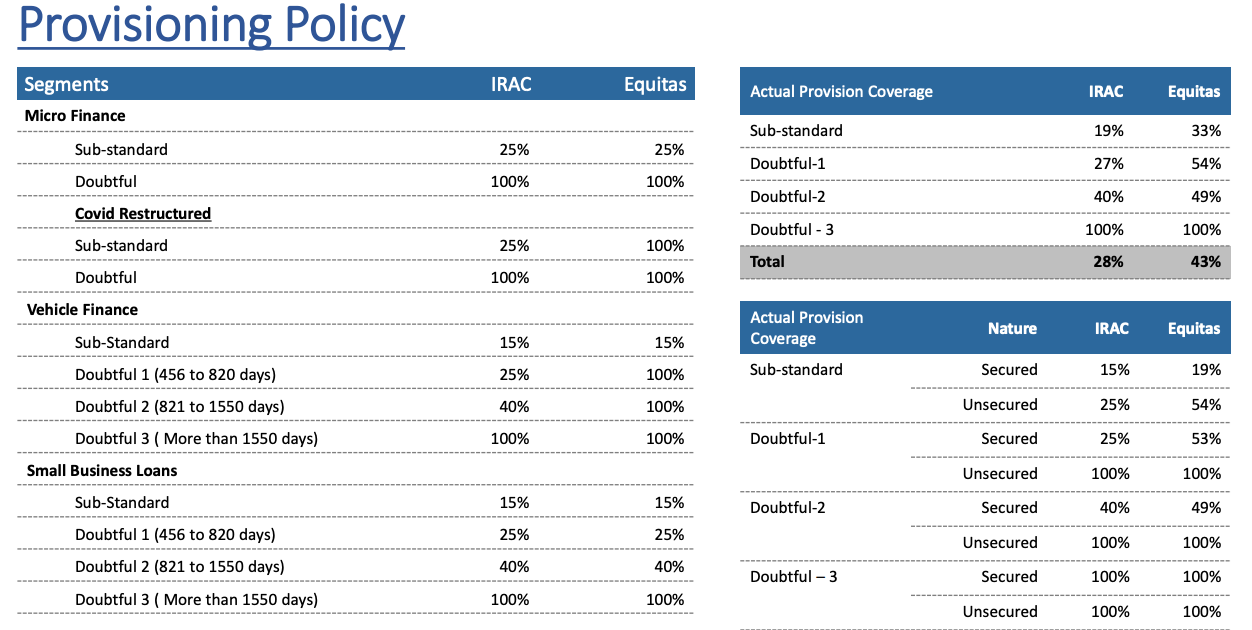

Bad stuff: Provisioning and writeoffs are worrysome:

- Writeoff of 191 cr in this quarter which is ~1 % of gross loans.

- Addition of 408cr NPA, highest for FY22. Although this was expected due to the restructuring 2.0

- Continuously declining PCR at 42.73% now (46.81% last quarter.

Though a lower PCR can be somewhat justified by the fact that Equitas has > 80% of assets secured. And Their provisioning against unsecured loan is higher than what this lone number represents.

Sub standard unsecured loans are 54% provisioned.

I do have questions on how much writeoff is actually a loss to the bank, since we have secured loans. How much is the bank able to recover as a % of the advance?

disc: invested

4 Likes

When major banks NPA s are declining in the 4th quarter equitas is not in such path… PCR reduction is highly worrying factor…Any decent justification in concall??

As per Q3 concall they have 200 cr of provision against the total restructured book. This 200 cr is not considered while calculating PCR.

To understand how write off and provisions work see this. I explained it in HDFC Bank thread.

2 Likes