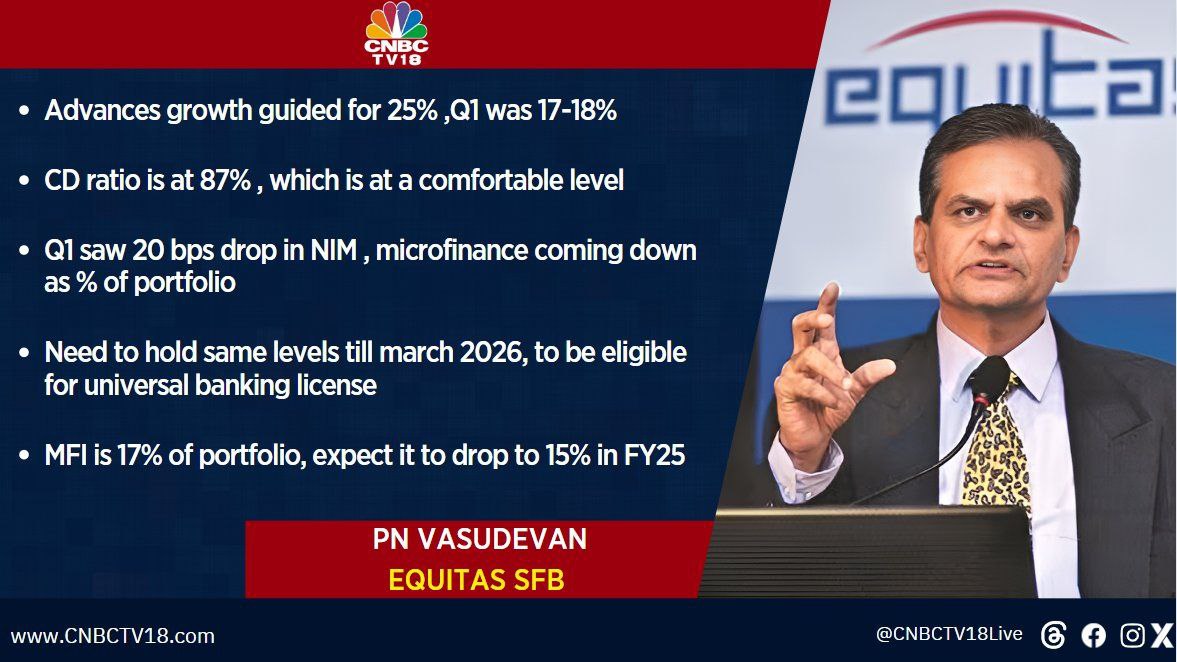

PN Vasudevan’s latest interview explaining their business model in detail.

PN Vasudevan’s latest interview explaining their business model in detail.

Very good interview by ceo

Interesting Set of Result

Improvevement in Net NPA with growth.

However profitability has taken a hit with a floating provision of 180cr. Can anyone expllain what it means.

Did anyone attend the concal today.

Bank is going for universal bank license as mentioned in investor presentation

and bank is going through rbi guidelines

Even after high provisions

There ppop grew by 9 % YOY

I think ppop is pre provisions operating profit. Provisions will be deducted from this to get profit for the period. As equitas set aside 304 cr as provisions, hence profit after tax is 26 cr

yes,you are right profit is 26cr

For au mostly they would get license

But ujjivan still behind as there majority of book is still unsecured

GNPA limit is 3%, not 2%

yes my bad. you are correct.

What differentiates equitas from another small finance bank is that Their 85 percent loan book is fixed means when rate cut would be there, nims wont fall much.

RBI hasn’t defined what they consider a diversified book. Do they mean product diversification, geographic, income groups etc? No one knows yet.

If being concentrated in unsecured is not diversified, the same applies to being concentrated in secured. Most of the SFBs, and banks like Bandhan are highly concentrated in their home state which has and can have adverse effects.

So we will need to wait and watch what the RBI considers diversified and safe enough to be given a UBL.

When rates rise, and the economy’s growth is strong, NIMs compress because competition for deposits rises and CoF increases. Floating rate loans are quickly repriced but fixed rate loans are not and thus NIMs contract. This is what happened with Equitas because as you said they are a majority fixed rate book.

When rates fall, this usually happens in a slowing economy, as the CB may have overtightened, the lender’s need for deposit growth is not as high as credit demand may not be as high as in the scenario above, thus lenders are quick to reprice deposits, CoF reduces. However, the lenders are in no hurry to reprice the loans and pass on the falling rate benefit 1:1. Thus NIMs usually expand in this scenario.

So the default state in a rate cut environment is NIMs expanding and not falling as you have mentioned.

@hack2abi what advantage does fixed rate loans offer to equitas then?

The only think that I can thing of is that NIM expansion their case would be greater when the rates fall, since they won’t reprise older advances and will reprice deposits immediately?

Has fallen to 52 week low today. Any negative triggers?

FY25Q1 Concall Summary

Positives

Negatives

Q&A

I’ve tried to understand and summarize whatever I found interesting. Any and every feedback is appreciated.

Did they mention about stress due to recent floods and landslides in TN and KL?

Nothing on that. In fact, management was asked the reason for the elevated delinquencies in microfinance. I’ll add the quote from the concall here.

It’s (microfinance delinquencies) really been moving badly. And what started in some is actually spreading to more pockets now. And this is not really led by some event risk. It’s not a political or it’s not a flagged kind of a natural disaster-related issue. So this is something that is actually fundamental to the industry itself.

Page: 10-11 of the concall.

Also, the landslides are much more recent in nature. So, if there is any effect due to that, it’ll probably come up in the next quarterly results/concall.