The charts suggests the downside shall continue till 71-72 level since the downward moment has started after breakdown from neck level of the head and shoulder pattern.

2 Likes

Higher slippage means the loans are given at much lower rate than market rate, right ? which causing the contraction in NIM’s . Please correct I have less knowledge of these finance terms.

slippage means bad loans, so higher provisioning.

6 Likes

EQUITAS SFB experienced a rise in its GNPA ratio to 2.7% in 1QFY25, driven by increased slippages in the MFI segment (INR850m) and vehicle finance (INR1.5b), pushing the overall slippage ratio to 4.5%, which exceeds the management’s comfort level of 4%.

The stress in the MFI business is widespread across multiple regions, primarily due to over-leveraging issues within the industry. This ongoing stress has impacted profitability and will keep near-term performance in check.

However, with the bank successively reducing the MFI mix to ~17% (from 19% in FY22) and an anticipated recovery in vehicle finance, one can expect the slippage run-rate to ease from 2HFY25 onwards.

The Bank’s ability to swiftly recover from previous credit cycles (e.g., COVID-19, demonetization) with controlled credit costs supports optimism for an improvement in asset quality in the second half of FY25.

Borrower-level indebtedness in the industry has increased swiftly over the past couple of years after the change in guidelines by the RBI. The general level of borrower discipline (as observed in aspects such as center meeting attendance) has steadily declined. However, the industry associations for microfinance are working together to resolve the issue through coordinated efforts and some tightening of credit filters.

Accordingly, Equitas SFB has already implemented the MFIN guardrails as part of its business rule engine in microfinance. Rejection rates are likely to inch up, as all lenders implement these guardrails.

A large share of Equitas’ microfinance business is in Tamil Nadu, Karnataka and Maharashtra. There have been some collection-related challenges in select pockets of Tamil Nadu and Maharashtra. The bank does not have a sizeable microfinance business in the northern part of the country, with some limited presence in Rajasthan. The bank does not have any microfinance business in Bihar.

Management indicated that it does not see any major challenges to its income at the borrower

level. Hence, the company remains hopeful about the microfinance industry stabilizing over the next two quarters.

Credit cost for 1QFY25 was elevated (~3.5% of average gross advances) due to the creation of ~Rs1.8 bn of floating provisions. Excluding this floating provision, credit costs for the quarter stood at ~1.4% of average gross advances.

The creation of the floating provision also helped to reduce net NPA below 1%, which is one of the eligibility criteria for an SFB to transition into a universal bank.

Currently, microfinance is the only unsecured asset product offered by the bank. Over the next year or so, the bank might introduce a few new retail products such as personal loans and credit cards, with the objective of acquiring and retaining more liability customers.

The credit card product is expected to focus primarily on existing-to-bank customers. Even after the addition of personal loans and credit cards, management expects the overall share of unsecured loans to remain at or <20%.

The bank saw a sharp decline in the CASA ratio during the current rate cycle as it declined from a peak of ~52% in March 2022 to ~31% in June 2024.

Management indicated that the bank saw a steady shift in customer deposits from savings account to term deposits during the rate cycle, as the differential in interest rate on incremental term deposit and incremental SA deposit widened sharply.

Some of this shift was also encouraged by bank customer relationship officers to prevent the loss of business to competition. Management is now confident about maintaining the CASA ratio in the range of 30-35% (~31% as of June 2024).

In management’s view, cost of funds remains the biggest risk to the achievement of 1.8-2.0% RoA over the medium term.

Sources: Recent reports from Motilal Oswal and Kotak

9 Likes

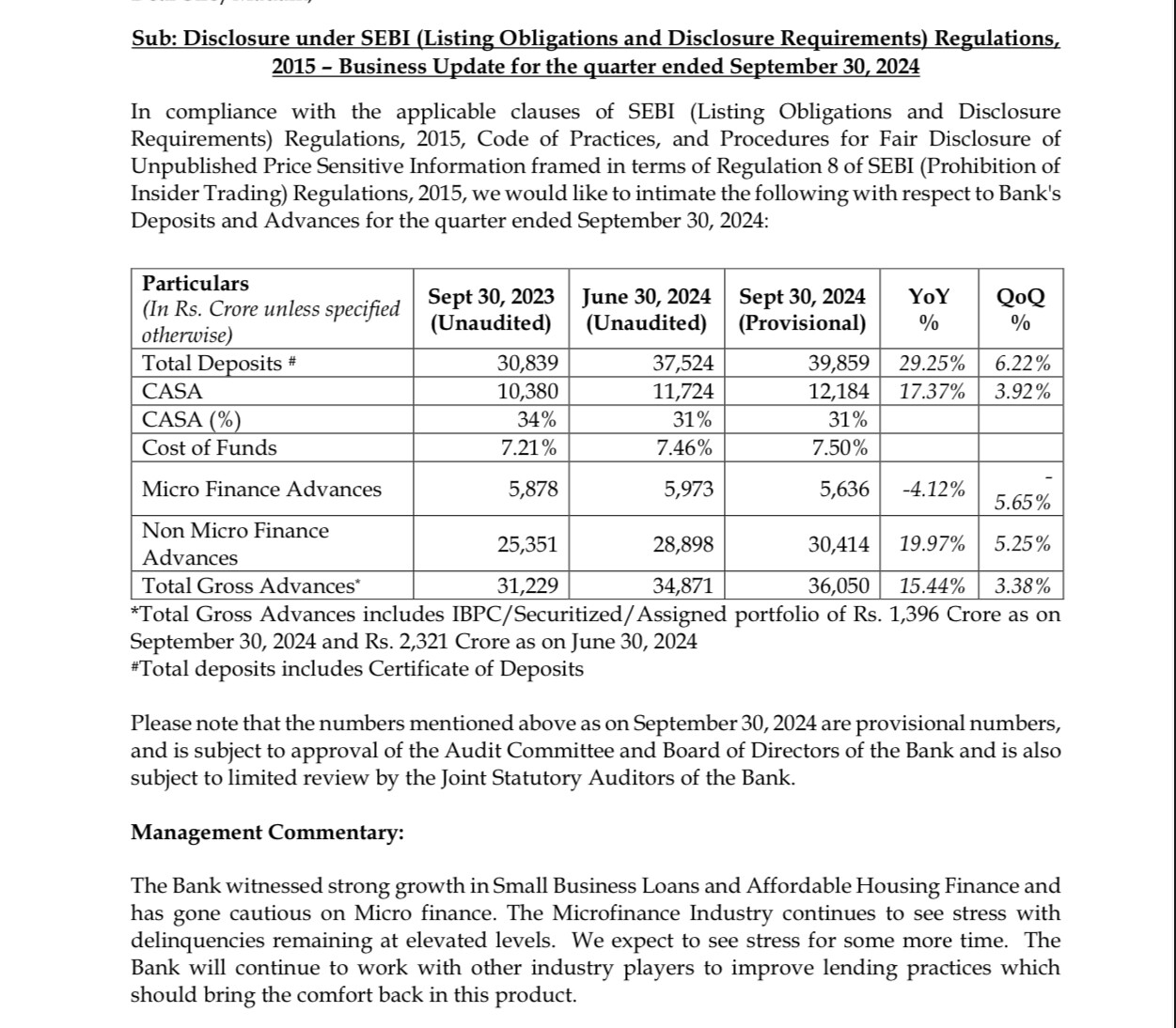

Key figures for q2 provisional

MANAGEMENT COMENTARY

Strong growth in Affordable Housing & SBL

MFI Industry witnessing stress at the moment & management expecting stress for some more time

MFI is 16 % of total advance & expected to go down further

Deposit growth steady, growth slowing down

Disc- invested

6 Likes

Overview of Microfinance Stress at Equitas Small Finance Bank

The primary concern is the elevated delinquencies in the microfinance portfolio.

Increased Slippages: The bank’s management acknowledges that microfinance asset quality is a concern, as slippages continue to be high. Gross slippages were 4.49% for Q1FY25, exceeding the bank’s comfort level of 4%. The microfinance portfolio contributed INR 85 crores to slippages in this quarter, a significant increase from INR 35 crores in the same period last year.

Impact on Credit Costs: The elevated slippages have led to a spike in credit costs for Q1FY25. The bank created a floating provision of INR 180 crores to align with the latest RBI guidelines for Small Finance Banks (SFBs) aiming to convert into Universal Banks. Excluding this provision, credit costs were 1.44%, with microfinance contributing INR 62 crores.

Reduced Disbursements: The bank has slowed down disbursements in the microfinance segment due to the challenging environment. Disbursements in this segment declined by 29% year-on-year.

Impact on Net Interest Margin (NIM): The reduced disbursement in the higher-yielding microfinance segment has contributed to a sequential decline in NIMs.

Factors Contributing to Microfinance Stress:

Industry-wide Issue: The management highlights that the stress in microfinance is a fundamental issue impacting the entire industry. This is unlike previous stress events triggered by external factors like demonetization or the COVID-19 pandemic.

Overlending and Increased Indebtedness: One of the key factors attributed to the stress is the increase in borrower indebtedness due to overlending practices in the industry. The implementation of uniform microfinance lending guidelines by the RBI is cited as a contributing factor. These guidelines led to an increase in the eligible loan amount for borrowers, which resulted in a rapid escalation of ticket sizes and overall borrower indebtedness as lenders competed to capture market share.

Lack of Discipline in Implementing the Code of Conduct: While industry players have signed a code of conduct to curb overlending, the bank’s management expresses concerns about its effectiveness on the ground level. The lack of strict adherence to the code is hindering efforts to control the rising delinquency levels.

Geographic Concentration of Stress: The stress is not uniformly distributed across all regions. The states of Punjab, Haryana, and Gujarat are experiencing significant problems. Certain branches in Maharashtra, Tamil Nadu (Erode), and other areas are also showing elevated stress levels.

Response to Microfinance Stress:

Focus on Micro-LAP: The bank is focusing on growing its Micro-LAP (Loan Against Property) portfolio within the Small Business Loans segment to compensate for the reduced focus on microfinance. Micro-LAP offers similar yields to microfinance and is considered a fully compliant Priority Sector Lending (PSL) product.

Cautious Approach to Microfinance Growth: The bank is exercising caution in disbursing new microfinance loans until there is more discipline in the sector. They aim to observe the industry’s collective efforts to improve discipline and monitor the effectiveness of the code of conduct before making any significant changes to their microfinance strategy.

Industry Collaboration: The bank is actively engaged in discussions with industry associations like Sa-Dhan, MFIN, and ASFB to address the stress in the microfinance sector. The goal is to collectively enforce the code of conduct and encourage responsible lending practices to restore stability to the industry.

Strengthening Collections: The bank is bolstering its collection efforts to improve the situation. This includes strategies like:

Increasing staff dedicated to collections.

Segmenting collections efforts by delinquency buckets.

Focusing on the underperforming Vehicle Finance segment.

Future Outlook:

The management expects to gain more clarity on the microfinance situation in the next two months. The trajectory of credit costs and microfinance mix will depend on whether the industry can effectively address the overlending issue and improve collection efficiency.

10 Likes

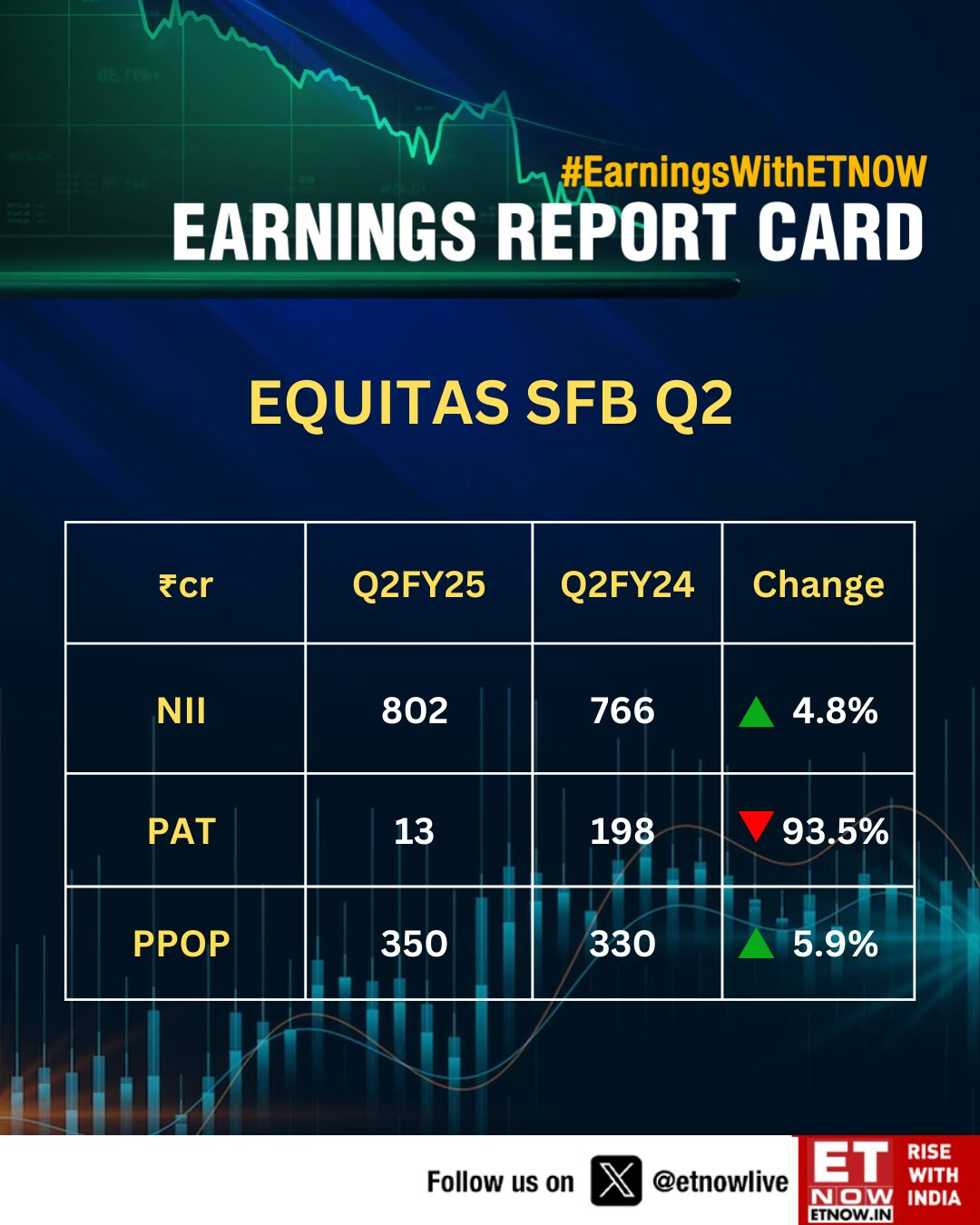

Equitas Small Finance Bank’s Q2 financial performance showed mixed results, with a sharp decline in net profit but solid growth in interest earned year-over-year.

Key Points from Q2 Results:

- Net Profit: The bank’s net profit fell drastically to ₹13 crores, a ~93.4% year-over-year (YoY) decline from ₹198 crores. This sharp drop was well below the market’s estimate of around ₹158 crores and was largely impacted by an increase in provisioning for potential loan defaults.

- Interest Earned: On a positive note, the bank saw a YoY growth of ~14.7% in interest earned, reaching ₹156 crores, up from ₹136 crores in the previous year. This increase suggests a growing loan book or higher interest rates that boosted the interest income.

- Asset Quality: The bank’s asset quality weakened, with Gross Non-Performing Assets (GNPA) rising to 2.95% from 2.73% quarter-over-quarter (QoQ), and Net Non-Performing Assets (NNPA) increasing to 0.97% from 0.83%. The rise in NPA levels signals a deterioration in loan quality, possibly due to macroeconomic challenges affecting borrowers’ ability to repay.

- Provisions: Equitas increased its provisions for potential loan losses to ₹33 crores, up from ₹30 crores in the previous quarter. This conservative approach to provisions may be in response to the rise in NPAs, which often indicate higher risk in the loan portfolio.

The decline in net profit despite an increase in interest income reflects the pressure from rising NPAs and higher provisioning costs. The positive growth in interest earned shows that the bank’s core lending business is growing, but the increase in provisions and deterioration in asset quality suggest challenges in maintaining profitability amidst economic uncertainties. Equitas’s conservative provisioning could help safeguard against future risks, but it will be important for the bank to improve asset quality to stabilize earnings.

This Q2 performance may also affect investor sentiment, given the gap between actual and estimated net profit, and the rising NPA levels are likely to remain a key area of focus in the coming quarters.

1 Like

Some of the challenges before bank was facing are being improved here like due to higher rates interest nii was concern,now it is improiving. Likewise there is stress in microfinance sector and gold loan sector as well of which microfinance is 18 percent of whole loan book. In bad times as well bank is resilient from core remaning problems could be solved in 3-4 quarters. As per some experts in gold loan sector, the real stress would come in q3 and q4 lets see how bank would perform.

5 Likes

Equitas Small Finance Bank: Navigating Challenges, Building for Recovery

Investment Thesis

Equitas Small Finance Bank faces short-term pressures stemming from elevated credit costs in its microfinance (MFI) portfolio. However, the bank’s proactive measures, strategic focus on secured lending, and improving operational dynamics set the stage for medium-term recovery.

Key Highlights Supporting the Investment Case:

1. Elevated Credit Costs and MFI Challenges

- Microfinance Pain Points: The MFI segment reported slippages of 8.7% in 2QFY25, driving overall gross slippages to 5.8%. Elevated provisions (up >400% YoY) kept credit costs high at ~4%.

- Provisioning Adjustments: The bank raised its Provision Coverage Ratio (PCR) to address stress in the MFI portfolio and meet regulatory requirements for universal banking eligibility.

- Shift in Lending Mix: MFI disbursements declined 33% YoY, while overall loan growth was impacted, with MFI now forming 16% of the portfolio.

2. Resilient Non-MFI Portfolio

- Strong Growth in Secured Lending: SBL (Small Business Loans) and Vehicle Finance grew at ~25% YoY and ~15% YoY, respectively, signaling resilience in the non-MFI book.

- Lower Loss Given Default (LGD): While delinquencies in the non-MFI portfolio rose slightly, the lower risk profile of secured loans mitigates significant credit cost concerns.

3. Operational and Financial Trends

- NII and Margin Pressure: NII growth of ~5% YoY lagged behind net advances growth (~18% YoY), as the loan mix shifted toward lower-yielding secured products. NIM contracted by ~35 bps QoQ.

- CASA Decline: CASA ratio dropped ~70 bps QoQ to ~31%, though deposit growth of ~29% YoY reflects a stronger funding position.

- CAR and Liquidity Strength: The bank maintains a comfortable Capital Adequacy Ratio (CAR) of 19.4% and a Loan-to-Deposit Ratio (LDR) of 87%.

4. Growth and Return Outlook

- Medium-Term Recovery in Returns: Despite near-term headwinds, management expects to achieve mid-teen RoE over the medium term, supported by operating leverage, improved MFI performance, and cost efficiency.

Monitorables and Risks

- Asset Quality Trends: Progress in MFI collection efficiency and stabilization of credit costs, particularly in the non-MFI book.

- Regulatory Compliance: Meeting universal bank eligibility requirements, including net NPL ratio below 1%.

- Operational Efficiency: Successful execution of cost-reduction initiatives to enhance profitability.

Sources: Kotak Daily & Centrum

2 Likes

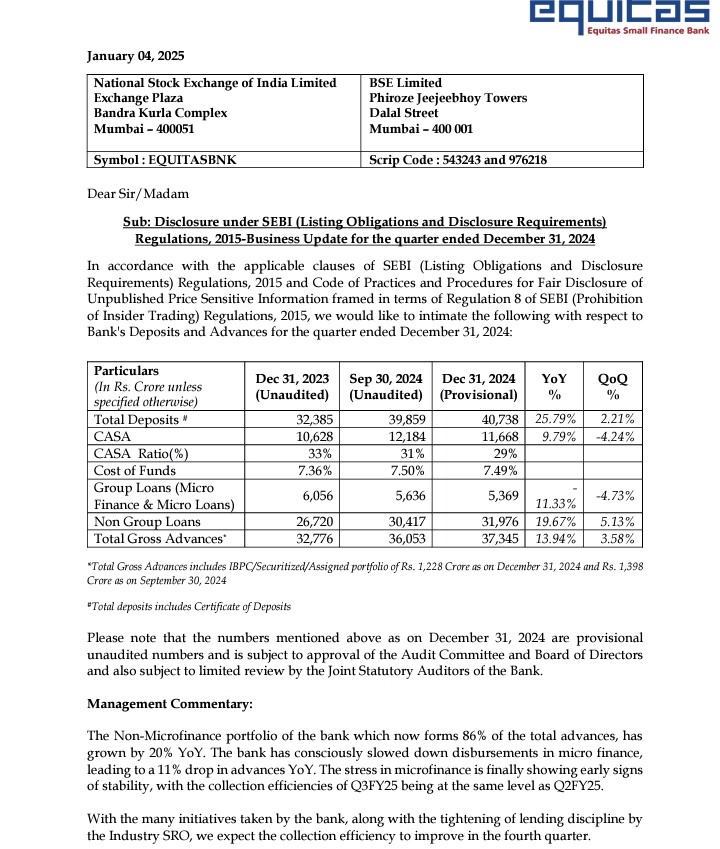

Q3 update

Management Commentary: The Non-Microfinance portfolio of the bank which now forms 86% of the total advances, has grown by 20% YoY. The bank has consciously slowed down disbursements in micro finance, leading to a 11% drop in advances YoY. The stress in microfinance is finally showing early signs of stability, with the collection efficiencies of Q3FY25 being at the same level as Q2FY25.

11 Likes

Technically also the price has taken a good support after correction it seems… just added to the portfolio this month… Will accumulate more if notice any strengthening signal.

2 Likes

Better than Q2 FY25 on profitability wise, NIM compression and mionr increase in NPA.

I guess matches the street expectations…not gone through concall.

Disc: Invested, might be biased.

3 Likes

Good results by equitas,with rate cut of 25bps it would benefit equitas as their 85 percent loan book is based on fixed interest rate and it can increase nims going forward.Roa and roe would be back to their prior levels in 2-3 quarters as it showed signs of improvement in this quarter.

Disclosure:invested

3 Likes

Equitas Bank: Key Developments and Outlook

-

Liability Franchise & CASA Mix:

- 30% CAGR in total deposits over the past four years.

- Deposit growth slowed in 9MFY25, with a sharp decline in CASA ratio to 28.6% YoY (down 1700bps over 2 years).

- Retail deposits remain healthy at 67%, but Savings Account (SA) balance growth is challenging due to preference for Term Deposits (TDs).

- Focus on mass affluent & HNI segment by realigning SA rates.

- CD ratio at 87% (3QFY25), supporting stable margins and SA profile, especially when the interest rate cycle turns.

- Expected 21% CAGR in deposits over FY25-27E.

-

Loan Growth & Asset Mix:

- 21% YoY loan growth in 3QFY25, driven by 26.7% growth in SBL.

- MFI exposure down to ~14.4% of AUM, with plans to reduce it to single digits.

- Focus on growth in secured products: micro-LAP, affordable housing, used CVs, and personal loans.

- Target of 22% CAGR in loans over FY25-27E, led by secured segments.

-

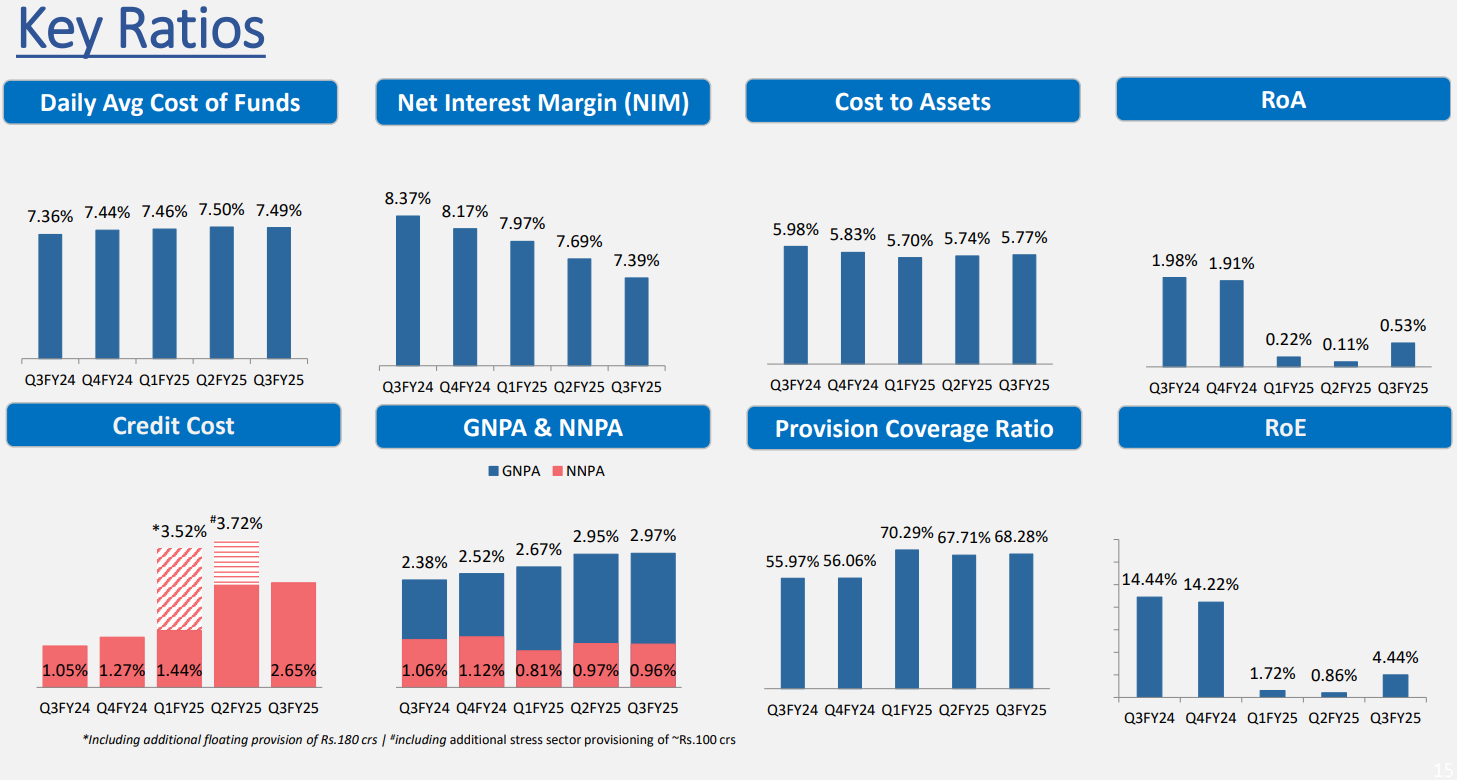

Asset Quality & Credit Costs:

- GNPA ratio increased to 2.97% in 3QFY25, with higher stress in the MFI segment (up to 14.2%).

- Non-MFI slippages improved, reducing from 2.28% to 1.11%.

- Elevated MFI stress remains a challenge, particularly in regions like Karnataka, with CE down to 90%.

- Collection efforts strengthened with 1,000 new employees.

- Credit cost remains elevated in the MFI segment, while non-MFI book remains manageable.

- MFI exposure expected to decline to single digits, reducing overall cyclicality in business.

The persistent challenges in the MFI segment have affected the bank’s profitability, which is expected to limit its near-term performance. However, the bank has reduced its MFI exposure to approximately 14% (down from 19% in FY22) and is implementing measures, including hiring 1,000 new employees to enhance collections in this segment. With its capacity to recover quickly from credit cycles and maintain controlled credit costs, the bank is likely to see improvements in asset quality in the future.

3 Likes