Thanks for sharing the results. Would like to add couple of more points here:

Bank is going to apply for universal bank license in FY 24. This will help it to drift loan book more towards Urban customers and sell Loans such as PL/VL/SME loans and credit cards since a Universal bank needs to have only 40% PSL lending against 75% for SFB. This will protect bank in a better way in covid type macro disasters.

The way Bank has grown Small business loans with Overdraft facility also added- It is a feather in the cap which not even large banks can poach since it is not based on proprietary lending models and needs some variations as per customer needs. To my understanding, this is a game changer for the bank. With only 50% LTV, it has high security against NPA.

Cost of funds will moderate in rest of the year and NIM around 9% should be manageable since deposit rates have peaked. Mind you-AU SFB has 5.5% NIM much lower than IDFC NIM of 6.3%. AU is too expensive as compared to Equitas.

Equitas has NIM of 8.75% with 81% secured book as compared to 9.2% of Ujjivan with only 26% secured.

Fee income is growing well with good focus on wealth, cross sell.

Huge respect and credit to MD Vasudevan sir who has 37 years work ex: 20 years with Cholamandalam. Few might know that in 2005, he was a contender of CEO of cholamandalam but he left and started Equitas microfinance. He has a strong team with him from Chola who takes care of Assets & liabilities. Vasu sir knows his stuff very well and is a very humble person.

Bank’s growth us highly dependent on its Leader and employees. I went through a linkedin post where equitas employees were extremely happy being part of the bank as compared to Large banks such as HDFC, Axis where attrition is 35-40%. Believe me, employees are fed up of the target culture and business pressure.

IMHO, Equitas is a strong contender for long term compounding if it doesnt commit any mistakes since banking is all about not doing big mistakes as per Mr. Aditya Puri. Happy investing!

Hi All,

As i see, the Q1 2024 results have been good with significant growth in disbursement and PAT. Well, NIM has gone down a bit but as per market standards.

Then why has the share price been falling since yesterday? Have I missed any news or updates?

@abhinav_sinha You are correct plus this is regular profit booking as many investors would have bought it before results. Further, investors are also more bullish towards unsecured/micro finance at the moment due to present euphoria. Some might be shifting to microfinance and Ujjivan SFB.

ok. Thanks for the reply. So this looks like a temporary drop in share prices hopefully as the fundamentals are still strong. Or I am wrong?

If it is temporary, then we can treat it as possibly a buying opoortunity.

Absolutely. No issue with financials, that can be vouched. You should also study the investor presentation and understand the loan book. It is 81% secured and only 19% microfinance. Even during covid, Equitas has not posted any quarter in red since the book is secured and diversified in SME finance, Vehicle loans, Microfinance.

In Q1 FY 24, NIM pressure was there due to high FD Rates and Loans being fixed for avg tenor of 2 years. Still NIM is quite strong at 8.75% which Mgmt has told can go down to 8.50% in FY 24 which shall again start going up when Interest rates start declining. AU SFB has NIM of 5.5% with quite similar loan book. Equitas is a long term stock so temporary blips are always possible. It cannot be compared with any microfinance lender. I feel one should focus on the strengths of the bank such as Strong leader, Stable management, Very strong growth in deposits, 25% plus loan growth, Low PE on forward basis, Strong CASA & Retail deposit franchise, Huge potential in small business secured loans in informal economy, good fee income and plans for universal bank.

Hi Sudhanshu, I followed your posts on Ujjivan SFB as well. Do you see better prospects for Equitas as compared to Ujjivan? Would like to know your take on it

Both banks are doing good in their expertise segments. Ujjivan is microfinance leader and has affordable housing book. They have not been successful in MSME financing till now. Equitas is very strong in SME loans and Vehicle finance alongwith affordable housing. Today entire financial space is talking about lack of credit in MSME space. Key for Ujjivan long term sustained performance is Diversification to secured lending to avoid major impact from macro economic shocks and key for Equitas is maintaining NIM’s, cost to income. Ujiivan at present has very low NPA ratio plus operating leverage is playing out since microfinance is low cost business. Seeing the past track, microfinance is growing strongly now but it is difficult to grow this business at 25% CAGR since it is unsecured and dependent upon economy doing well since you are lending at the bottom of pyramid. At present, Ujjivan looks cheaper than Equitas. Equitas is much cheaper than AU SFB. So, compare Ujjivan with Utkarsh/Credit access/Fusion/Suryodaya and Equitas with AU SFB. I am invested in both since both have a good long term journey as these banks are addressing informal economy which is very tough for large banks since they lack experience and focus being too big in formal economy. I personally feel, India’s growth in next 2 decades shall be much higher in Tier 2, 3 and below markets. In last 7 years, no other SFB has been able to grow deposits, assets, retail business so well as compared to Equitas/Ujjivan/AU. So credit has to be given to these banks as being leaders in small finance space which are still building the bank franchise.

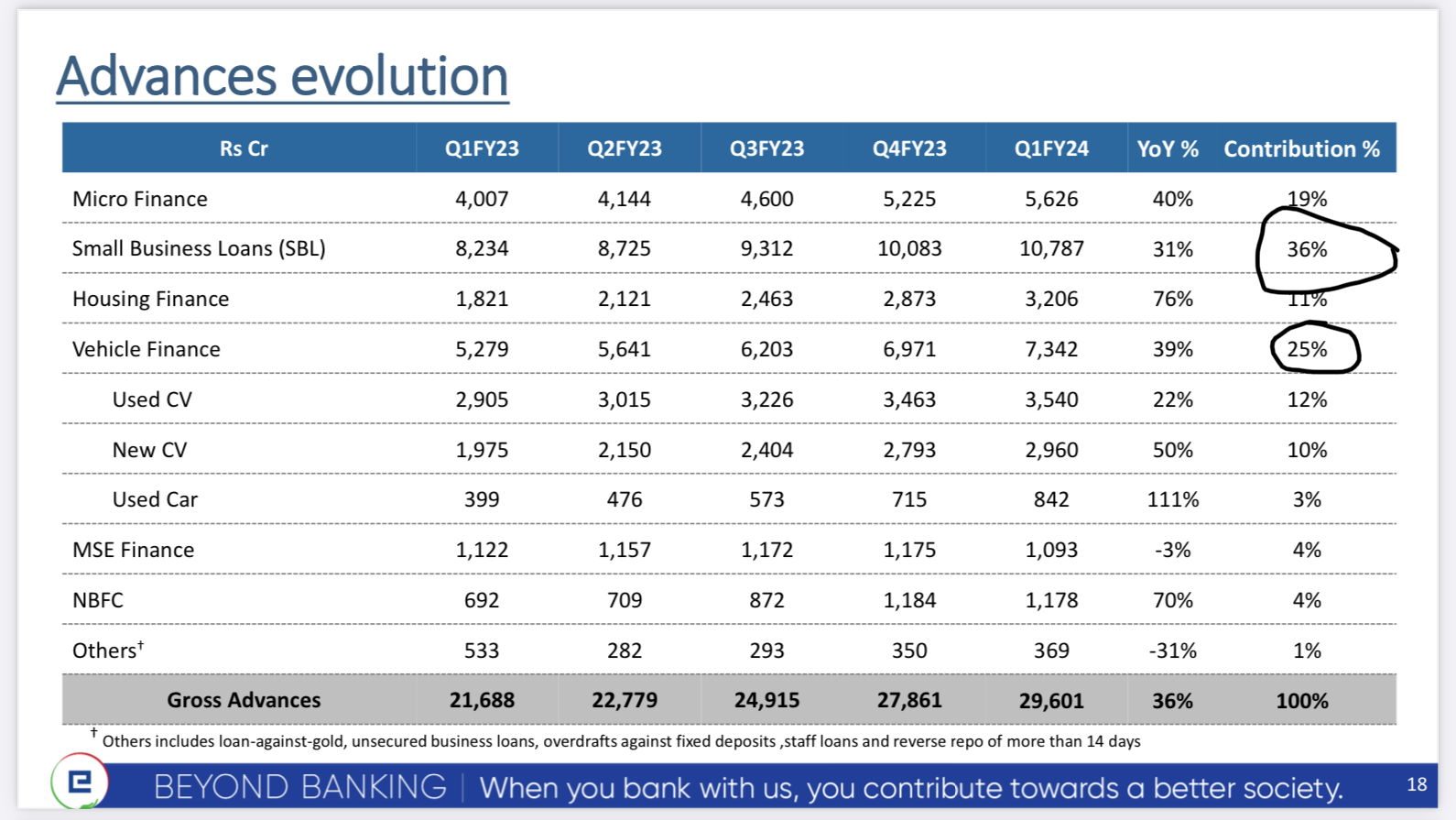

As we can see in the above graph (from Crisil research), AU and Capital have completely moved away from unsecured Microfinance lending. Equitas has reduced the exposure to MFI to 19%. This will make their business robust as most of their lending is secured.

I prefer investing in good quality/high growth small caps so i prefer Equitas over AU SFB. Plus, the leadership at Equitas is also good.

As Sudhanshu said, it should be a long term story. So dips in price can be treated as opportunities. Contrarian thoughts are welcome.

AU SFB is expensive. Few points to mention about AU as compared to Equitas:

AU ROA is 1.70% and ROE id 13.50%.; Equitas ROA is 2.10% and ROE is 14.54%

AU Yield on assets is 13.80% whereas Equitas is at 17-18% since Equitas SBL Loans have a higher ROI as compared to AU SBL plus equitas has some microfinance also. SBL loans is a huge opportunity and equitas has managed the risks very well in Covid which reflects their strength in the segment as compared to peers.

AU is guiding at 5.5% NIM whereas equitas after repricing of deposits is guiding at 8.50% NIM.

AU P/B TTM is 4.2 times and Equitas is at 1.89 times. Both are predicting similar 25% plus growth.

Thanks for nice analysis, what is your view on the low PCR in Equitas ~ 58% (while its increasing) v/s general industry standards of 75%+…Ujjivan is at 94%, AU at 74%. Does that increase risk for Equitas v/s UJJ or AU?

Hi. Management has guided to improve PCR to 70% over next 1-2 years. The loans are largely secured with low LTV and I believe even the valuation would also be on a conservative basis unlike metros, which would result in high recovery. There is not much risk as per one of the Analysts mentioning sufficient PCR during latest concall. Even Management which is also conservative was of the view that current PCR is satisfactory since borrowers who are still gradually coming out of covid impact are paying back loans, so till the time recovery is certain, it doesnt make sense to write off the loan. PCR cannot be compared with Ujjivan as it has high microfinance book. AU might be having higher PCR since loan book is also double of Equitas. If you see the NNPA amount it is 300 crore approx for Equitas, which looks manageable.

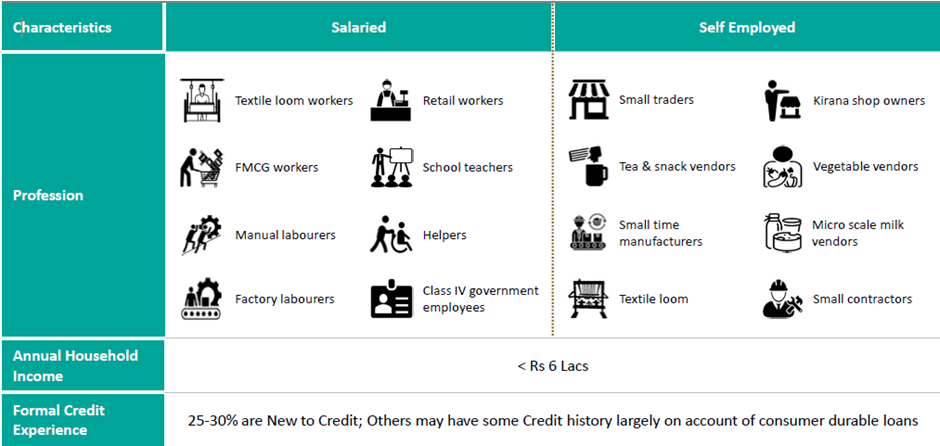

Informal economy participants as per ppt of one NBFC. These people are very careful in NPA since they generally take credit from Money lenders at high ROI. SFB/NBFC are giving them credit at half rate of market i.e. 16-18% p.a. .They will try a lot to save the only property incase of Equitas SBL security from being taken away from them. Hence, if macro economy is doing well, this sector will not have large NPA.

To calculate the Earnings Power Value (EPV) for a stock, you typically need to estimate the sustainable earnings and choose an appropriate discount rate. In this case, I’ll make some assumptions to estimate sustainable earnings and use a hypothetical discount rate for illustrative purposes. Please note that this is a simplified calculation and should not be considered a precise valuation.

Let’s assume that the sustainable earnings for Equitas are the average net profit over the past five years, which would be from March 2019 to March 2023:

Net Profit (March 2019 to March 2023):

244 + 384 + 281 + 574 + 668 = 2151

Average Net Profit (Sustainable Earnings):

2151 / 5 = 430.2

Now, let’s assume a hypothetical discount rate of 10% for this calculation.

So, using these assumptions, the estimated Earnings Power Value (EPV) for the stock would be 4,302.

Please keep in mind that this is a simplified calculation for illustration purposes, and in practice, determining sustainable earnings and selecting an appropriate discount rate would require a more in-depth financial analysis and consideration of various factors. Additionally, different analysts may use different methods and assumptions, which can lead to different EPV estimates.

Overall it seems to be very impressive results . Their ability to operate at such high NIMs and maintaining NPAs under control , with such a high percentage of secured book is one of the best . The valuation gap between them and AU may reduce in coming months .

May not be very relevant for bank’s offering high interest on S/B accounts . With average cost of SB around 6.2 in CASA and average TD rate around 7.2% money will move interchangeably between both the categories . It would be important to track overall cost of deposits and Retails TD contribution

Festivals coming in will improve cashflows for households in H2

Commerial vehicles and SBL have healthy indicators, can push more high yielding products

CASA an area of focus for the bank, will grow the book going forward

Old deposits getting replaced with new ones, interest costs to go up to 7.5%

NIM drop to remain stable within guidance

Demand remains strong for CV. Focus on LCV

Demand to remain strong for Consumer Vehicle loans as festive season is here

Bank sold non performing advances to ARC for 162Cr (SBL book), recovered 118 Cr and wrote off 44 cr

Interest cost to move to 7.5% over the next 6 months

Increased the lending rates in different products will experience the effect in next quarters

H2 is more robust from a disbursement perspective, this will help in maintaining RoA

If interest rates remain the same or go down, it will help the bank as 85% of the loans are fixed rate loans

Opex grows sharply in the first half (staff costs) and decreases opex towards the end of the year

18.3% yield on disbursement in Q2FY24,16.96% yield in SBL and CV. These yields are going up QoQ, effects will be realised over time as it is a fixed rate loan book

Incremental growth in deposits has slightly affected NIMs

Slippages are marginally higher and this is due to CV, weak collections. But these will be covered up soon