ENIL Seems to be in good shape now as it holds cash/liquid funds worth 320crs (370cr on Sep 13) On face of the numbers its ROE seems to be avg 15%, but if we subtract 320crs from its Net-worth of 500crs to get its true operational returns, then we get almost close to 28% after excluding other income of 17crs earned from investing. Also other thing is I feel ENIL reported earnings understate true economic earnings. Reason one is it is able to earn higher returns on capital and second is the amount of money its spending on building Brand. Its ad spent last year was 66crs vs 55crs last year. As a result it was able to grow higher than its industry growth thus gain market share. Question is So should we treat this expense as capex and not just a revenue item? If that were to be the case then Return On Equity will be much much higher then my reworked number. Last years Pre tax op cashflow was 100crs so would be interesting if we get this company at 300/- or 1400cr mcap.

hi

indeed enil is good…market leader with good cash flow…however the only thing missing which i look in companies is how the profits/cash flow is reinvested…that is somewhat missing because as co is not able to deploy cash into business…i look for companies which are able to deploy cash generated into same business and still can get high roce on that investment…and that goes on and on…(if a co is not able to deploy much cash into same business…they may tend to show excess expenditure(under the table-over invoicing etc) yet having good profits…but investors wont be able to get the benefits…increasing cash in bs wont make it a multibagger–but will make it a safe investment…

however still the sector is yet to explode…and new auction for radio station awaited…this will absorb the cash…good company to buy in bear market because it will rise again and would be safe in uncertain times…still a company worth in portfolio.

hi

another co that comes to mind is zee media corp(zee news)…mkt cap at 300 cr with revenue touching 250-300 cr and ebitda from old business in range of 25-30%(new business /channels take time to become ebitda positive- at present negative ebitda of new businesses offsetting old business ebitda partly…hence 14% ebitda margin)…

the co is into a business of 25-30% ebitda at least…(compare zee entertainment revenue breakup etc).hence im getting a co with mkt cap of 300 cr and 60-90 cr ebitda in media sector…subscription revenue is 100 cr per year…something great…adding directly to the bottomline…

for me its a multibagger stock for future with minimum risk(zee ent is a 26000 cr mkt cap company)…

it is one of the best investment with minimum risk…with sure profits…wont be surprised to see it become a 3000-5000 cr mkt cap company when full effect of cas rolls out…

Hey Jatin,

Check out this article,clearly highlights the problems faced by the Radio industry.

Highlights of the call by Capital Mkt;

The mgmt said that during this year, radio industry has grown by 11% - 13% against just under 10% growth of television and 7% - 10% growth of newspaper industry.

On standalone basis, the company’s net revenue for December 2013 quarter was up by 13% to Rs 98.52 crore. OPM inclined by 430 bps to 38.8%. The net profit was up by 38% to Rs 25.88 crore due to increase in operating margin.

Top-line growth was driven by volume, effective rate (ER) hike and multiple income streams.

Revenue growth was driven by 5.5% - 6% volume growth and 4.5% price hike growth.

The mgmt said that the phase III auctions would start in next six months as all the radio operators have given their suggestions on the consultation paper floated by Trai. Election will have no impact on auction.

The mgmt said that it is gearing itself for Phase III expansion and that would increase opex in next 4 quarters as company would be investing in brand building and team building. This would impact the margin and PAT in FY15.

Q4 will be tough quarter because of high base effect.

The mgmt said that ad rate will see hike in Q1 FY15, led by election spending and in Q3 FY15, driven by festive season. The company expects yield improvement led revenue growth in FY15 as utilization has already peaked.

The mgmt said that in Phase III, the major part of the revenue would come from multiple frequencies in Metros and key Urban markets while smaller stations would just increase geographical reach. But overall pricing power will be added, due to additional stations in addition to present 32 stations. The mgmt expects same kind of margin from new stations.

Election led spending contributed just 2% of the revenues during Q3. The election led spending from general election will be seen in Q1 FY15. The election commission is expected to relax norms on election spending by contesting candidates, which would drive ad growth in coming quarter.

The blended inventory utilization level was at 89% (on 13 min ad per hour basis). Utilization in top 8 stations was at 112%, while for remaining 24 stations it was 81%.

For Q3, the blended realization for the company is in the region of about Rs 10016.

The company leads in 22 markets out of 32 markets it is present.

As Phase II is also set to go for renewal, the mgmt expects renewal of Phase II license cost will be up by 50% compared to that of earlier period, as this time the license period would increase from 10 years to 15 years.

Total cash at the end of Q3 FY14 stood at Rs 390 crore.

|

Mr Prashant Panday Executive Director CEO;Key Highlights of call by Capital Mkt

As per the management, Phase 3 time line is confirmed from the government and auction will be held by end of Dec'14 or in Jan'15. Auction cannot get delayed any more.Phase 2 licenses as per the TRAI formulae of extension of licensees are likely to be accepted by the Ministry and if at all, the payments will be required to be made by April'15. The company currently on a blended basis is operating at around 98% capacity utilization and has still headroom left for busy quarters. 8 top cities operated at capacity utilization of around 110% and rest were at 93%.The company has Rs 464 crore of cash as on June'14. As per the management this would be sufficient for Phase 3 expansion program and no debt will be taken.Management is confident that volume will continue to remain high in Q2 FY'15 as well. There were some price hikes made in Q1 FY'15 and further price hike will be made in Sep'14, but more or less will help in mitigating any additional advertisement and sales promotion expenditure for Phase 3 or for other promotional events.Some additional marketing spend will come in FY'15, but will be more or less in same range of last year During Q1 FY'15, due to elections, political advertising were higher and stood around Rs 75 crore. However because of this, the government advertising was low. Overall put together the growth would have been around 25% YoY.The company is trying to transform from a pure Radio company to a solution provider in entire media space. Going forward the growth will come from overall improvement in pricing, higher capacity and inventory utilsation in new centers and in small locations in Tier 2 and 3 cities. Company is also open for acquisitions. |

Call was add by Mr Prashant Panday Executive Director CEO. Key Highlights by Capital Mkt;

Radio industry as a whole has done well in Q2 FY’15. Underlying economy continues to remain under pressure while higher spends and advertisement on Radio generally does well in such environment. As and when the economy improves, Radio will do even better.

Some of the sectors that are driving advertising growth in Radio are Retail, Media entertainment, Real estate, Auto FMCG, other services while Telecom and BIFS are a bit on the laggard side.Ecommerce business is a new sector which has great potential for Radio. The growth in this segment is phenomenal and is helping higher ad revenues.

Strong growth in Q2 FY’15 was also helped by lower base of Q2 FY’14 where there was some Un utilized inventory which got filled up this year. Prices were increased by about 5% on YoY basis.There was no political nor Govt of India advertising in Q2 FY’15. In Q3 FY’15, especially in the month of Oct’14 so far, the elections in Maharashtra saw some additional political advertisements.

Phase 3 auction process got delayed further. But the auction will happen in FY 2015. Management does not expect any irrational bidding in Phase 3 auctions.17*18% growth in Q2 Radio industry vis a vis 21% growth for ENIL.Non Radio portfolio also has grown well and is profitable even though margin is lower. These businesses include Activation business, multimedia solutions business, Event management business etc. Non Radio business will improve further and thus the overall margins of ENIL will go higher with years to come.

Marketing expenses was up by 38% YoY due to brand expenditure in preparation of Phase 3 auction.The company operated at overall blended 101% capacity utilization.The company has cash equivalent of about Rs 480 crore as on Sep’14.

|

Con Call Key Highlights by Capital Mkt; The Radio industry grew by around 15% in Q3 FY'15 and the company grew slightly better and was able to grab the market share. During the quarter, almost all the sectors grew and there was no extreme fall or rise of growth in any of the sector for advertisement income. There was a broad based growth in volumes across the sectors Margins were slightly under pressure on YoY basis largely due to continuous investments in HR and marketing side by the company. As per the management, they have just started on advertising and it will increase only from here on. Phase 3 auction is under way. Government information memo already being out and prebid conference has already happened. Management expects the acution to happen by the end of March 2015. However the Government has announced only 135 frequencies in first batch for auction to be bid for. These frequencies are the left over frequencies of Phase 2 which was supposed to be auctioned in 2006. Playes whose licenses were about to expire, they will also be able to migrate the current licenses for next 3 years. With regards to the remaining 700 frequencies TRAI has been asked to look at Reserve fee once again. Trai will come out with recommendations soon as players have already complained government about the higher Reserve fee. Current Blended utilization for the company stands at 110% for top 8 radio stations which are operating for 17 hours per day. At peak levels, the company can increase the utilization to 140% as well. The company has cash and cash equivalent of around Rs 514 crore. The company expects the surplus cash to be utilized for new license bidding and for M&A if any. |

ICICI Direct has issued a detailed report on this company in the last month. The price target of 670 is already surpassed.

http://www.moneycontrol.com/mccode/news/article/article_pdf.php?autono=1310838&num=0

Below are sum observations, based on which I believe the share has run ahead of itself IMHO :

=The radio industry size at present is expected to reach Rs.3360 Cr by FY18. The present mkt cap of ENIL is Rs.3357 Cr.

=The PAT is expected to grow at CAGR 15.2% till FY17E. The stock is already trading at 33x. The PEG is > 2).

=At reserve price, the company will have shell out ~ Rs.280 Cr for license renewal. The cash & cash eq are 514 Cr (as per above concall transcript), more than half of which will be gone in license renewal. How aggressively it bids for new frequencies remains to be seen, which will burn more cash.

=The stock price has been news driven and likely to provide exit opportunity at even higher levels at around auction timings

How about the threat from online radio? If anybody has any idea about global listed radio companies, kindly share their performance so as to compare.

Request all esteemed forum members to share their views / feedback.

Disc: Invested.

While there seems no immediate threats from online radio/music sites but it’s certainly attracting music lovers IMO. I myself prefer to listen music on saavn, gaana instead of radio channels which is usually full of crappy/real-estate/political ads.

Conference Call - from Capital Markets

H2 FY’16 will be relatively better in terms of both volume and prices

The company held its conference call on 20th May’15 and was addressed by key management

Key Highlights

• There was a mismatch in revenue and expense booking in Q4 FY'15. Major revenue lines like Mirchi Top 20 event, which was booked in Q4 FY'14 was preponed and booked in Q3 FY'15 for FY'14-15 period. So Q3 FY'15, revenue on like to like basis have actually grown by about 14% YoY as compared to about 18% reported on YoY basis. On similar line, revenue growth on like to like basis for Q4 FY'15 stood at 13% instead of reported 8%.

• Further, there were many expenditure in Q4 FY'15 which were not present in Q4 FY'14 like CSR expenditure, hiring of consultants, research etc for Phase 3 and acquisition of TV Today's radio business related expenditure. Thus on like to like basis, the Ebidta growth stands at 21% instead of reported 10% growth on YoY basis.

• During Q4 FY'15, about 2/3 revenue growth came from price increases while, rest 1/3rd from volume growth. There was a price increase made across the segments and sectors of the industries of about 4-5% in Q4 FY'15.

• This was possible as, most of the local companies and players are becoming national, so they need a national radio presence. However, challenges in the economy continue and it will be very difficult now for the company to increase prices, at least in H1 FY'16.

• Management expects relatively lower growth in H1 FY'16 while H2 FY'16 will be relatively better in terms of both volume and prices.

• Phase 3 now is clearly divided into 2 parts. In first part, about 135 frequencies covering the peak cities will come to auction somewhere in June 2015. The process is delayed by couple of months. Management expects smooth migration of existing frequencies to Phase 3. Further, the actual and full fetch operationalization of these new frequencies will be from Q4 FY'16 onwards.

• The Government has rejected the acquisition offer of the company of the Radio business of TV Today company. As per the Government, this is not within the framework of the policies. The company has challenged the decision and has gone to Delhi High court and the matter is pending.

• Current Blended utilization for the company stands at 107% for top 8 radio stations which are operating for 17 hours per day. At peak levels, the company can increase the utilization to 135% as well.

• Overall, management expects the Radio industry should grow around 10-12% in FY'16.

• As on Mar'15, company has free cash flow of around Rs 556 crore.

Disc: Not Invested. But on watchlist.

The threat from online streaming is real but it will take time to materialize. Cheap 4G internet from reliance coupled with subsidized handsets could bring the threat to reality much faster for example.

It has 6 radio stations on the Gaana App, but there too questions remain on whether Gaana can be built in to as strong a brand as Radio Mirchi is. The other competitors are Saavn and Wynk which is backed by Airtel. Other players like T-series/Saregama could easily launch an app for music streaming since they already hold the music rights and have a substantial library to boast of.

In South Korea despite having broadband internet for years, the average radio consumption is 61 minutes per day per person and is higher than internet consumption of 42 minutes per day per person.

http://www.pressreference.com/Sa-Sw/South-Korea.html

For USA too, though the stats are not recent, it shows that just having an internet connection does not mean people will flock like bees towards honey to streaming apps.

I quote from the web page whose link is given below:

( Radio is the second most powerful medium in the United States, reaching 59 percent of the country’s population daily. In comparison, 49 percent are reached by the Internet while print media accounts for 13 percent. Only TV, with a daily reach of 80 percent, is consumed on a daily basis by a broader audience. Online radio

is, somewhat surprisingly, used by just 15 percent of American radio

listeners, even though close to 80 percent of the U.S. population has access to the internet.)

http://www.newsgeneration.com/broadcast-resources/radio-facts-and-figures/

Whether the same will be replicated in India as it has in Korea and USA, only time will tell.

Disclosure: Invested

Stock trading at 30x FY15 P/E. Next couple of quarters expected to be weak (as mentioned by management on the concall). Then you have the radio auctions in next 3 months which could get aggressive. They will shell out 280crs and upwards for just license renewal in existing frequencies. New frequencies will cost more.

Disclosure: Was invested from lower levels. Have sold out

Call was addressed by Prashant Panday MD and CEO.Highlights by Capital Mkt

Sep’15 quarter earnings include costs that are built in for Phase 3 auction. On like to like basis, Ebidta would have grown by 20% and PAT by 26% for Sep’15 quarter on YoY basis.The entire revenue growth of 11.6% for Sep’15 quarter was led by price increase and better product mix. There was a price increase of about 7.5% in Sep’15 quarter and volume de-growth of about 3%.Volumes in major metros were higher on YoY basis, while in other market were lower on YoY basis.The company operated at 97.5% capacity utilization led by Metros. The entire focus in Sep’15 quarter was on pricing and company let go some of the volumes. Also the company increased its distribution of frequency in late night stations. Distribution of delivery was planned very well during the quarter.

Metros have done stronger due to E-commerce sector. E-commerce contributed about 11% of total revenue as compared to 4.7% YoY. Other sectors that positively contributed include Government, Auto and Automobile sector, BFSI sector. Some sluggishness was seen in sectors like Retail, Durables, Telecom and Media and Entertainment etc.The company bid very rationally in Phase 3 auction and there was no overbid. Entire migration of 36 stations was done at almost same license price. The company now holds license for next 15 years.

The company added new cities like Kochi, Chandigarh, Calicut, Gawahati, Jammu, Srinagar and 4 stations were acquired from TV today. With this, the company has now presence in more than 40 cities in the country.The company also acquired 2nd frequency and 2nd brand in the 12 out of total top 13 markets in the country. These 13 markets contribute about 70% of total revenues. This 2nd frequency will generate higher Ebidta as most of the programming and other costs are more or less the same. The company plans to do more with the product and will launch gradually.In all, the company spent about Rs 340 crore in Auctions of Phase 3 and on Migration led costs.Overall, management expects the Radio industry should grow around 12% in FY’16.

Introduction:

• ENIL is subsidiary of Times Infotainment Media Limited, the holding company promoted by Bennet Coleman & Company Limited – A flagship company of the Times of India group.

• Company is a leading FM radio broadcaster in the country with 32 operating stations spread across India with total listenership of more than 37 million. It operates the FM radio network with Radio Mirchi brand.

• ENIL is one of the oldest players in radio broadcasting business with its first station becoming operational as early as year 2000. It also has the distinction of being the only radio broadcasters to have consistently reported operating and net profit for last many years while all other players struggled to stay afloat.

• ENIL is an undisputable market leader with 33-35% revenue market share in spite of some of its peers having much larger foot print and operations in terms of number of stations. According to the last IRS radio listenership survey done Q4 2012, Radio Mirchi is way ahead of its competitors with weekly listenership base of 37.5 million, 50% more than the listenership of its nearest competitor.

• ENIL aspires to be a complete solution provider for the advertisers through multiple touch-points across various media. ENIL is slowly and steadily scaling up its non-radio businesses such as digital, activation and TV properties.

Industry:

Opportunity Size & Future Growth

• As compared to other media segments, FM radio industry in India is still in its early years. Private FM radio industry started its journey from 2001 with award of frequency to private broadcasters under Phase-I licensing. Thus, the FM radio industry is barely 14 years old in the country while other media like print and TV have been in existence since many years.

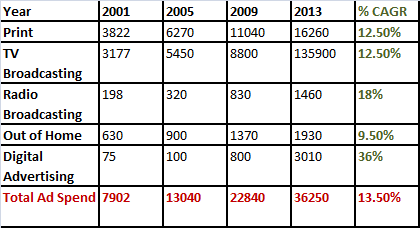

• Indian FM radio industry has grown at significantly higher rate as compared to other media as is evident from the below table.

Value in Rs. Crore

• Radio broadcasting market has grown at 18% CAGR from 2001 to 2013 increasing the share of radio broadcasting market in overall advertising spend from 2.5% to 4%. The only media segment that has performed the radio is digital advertising.

Key Drivers of Radio Industry’s Future Growth

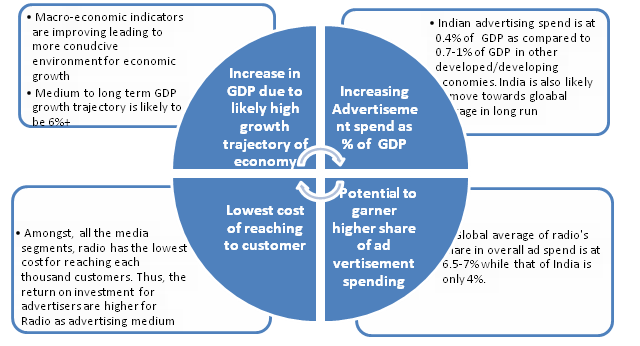

- Even though, radio industry has grown at brisk rate, it is likely that the industry is likely to grow at brisk rate due to the confluence of following 4 factors

-

Based on following range of possibilities on key assumptions India’s

-

GDP in nominal terms in 2014 is USD 2 trillion

-

In next 5 years, Indian GDP growing in the range of 6-8%;

-

Advertising spending accounting for 0.5%-0.7% the total GDP

-

Radio garnering 5% -7% share in the overall advertising spending

The size of the Indian radio industry may reach anywhere between INR 4000 Crore to 6000 Crore in 2019 in next 5-8 years implying 20-25% CAGR.

- Even though, none of the above numbers are sacrosanct, it is reasonably safe to infer that size of the Indian radio industry is going to grow significantly higher than its current size in next 5 years with growth for next five years at least equalling the historical growth rate of radio industry in last 5 years (18% CAGR)

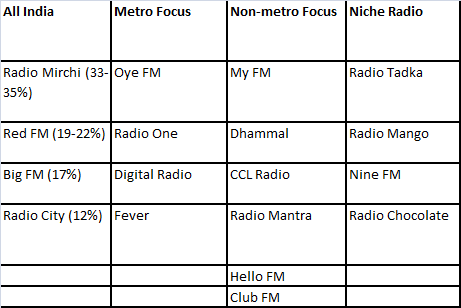

Competitive Landscape

• In all there are 19 players in FM radio space other than All India radio. However, in terms of countrywide presence, there are only 4 major players which have pan-India presence, well spread out network and geographical & social reach

Thus, two aspects are clear from the above analysis

o Pan India FM radio broadcasting market is an oligopoly with 4 large players

o ENIL enjoys the dominant position in the industry with market share of 33-35% which is 50% more than that of its nearest competitor

Salient characteristics of the business model:

• Company’s pre-dominant revenue stream comes from Advertisement. Total ad-revenue is a function of

1) number of operational channels

2) advertising rates

3) number of ad slots in an hour and

4) Number of operating hours in a day.

Out of the four variables, two variables i.e. number of ad slots in an hours (typical range is from 13-18 minutes) and number of operating hours in a day (in the range from 16-20 hrs) have physical cap. Thus, once company reaches an optimal number on both these variables at existing stations, the incremental growth shall be driven by the other two variables

• Only 7-8% of the ENIL’s cost is strictly variable cost while the rest is fixed cost. Hence there is huge operating leverage present in the business. Thus, after the operations reach break even point, large portion of incremental revenue will flow to the bottom line.

• Company, in a steady state operation, shall be able to achieve EBIDTA in the range of 32-36%

• Company, from time to time, would need to pay large one-time fee for getting the new license/renewal of license for FM bandwidth that it intends to use. This onetime payment is then amortized as cost over the period of license period. This peculiarity will require company to slowly accumulate and maintain decent amount of cash on the books for renewal of existing license or acquisition of new license.

•The above trait also implies that since company would have paid the onetime fee upfront, the amortization of the license fee is a non-cash expense. Thus, in most of the years, the cash flow may be much higher than the reported profit.

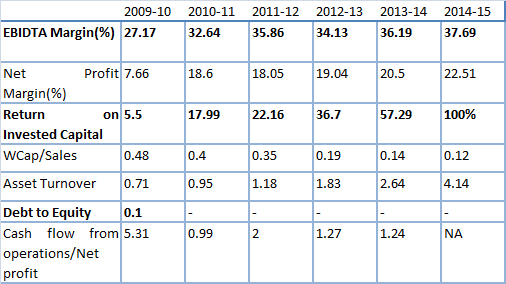

Financial Analysis:

-

In last 5 years, company’s top line has grown at 14% CAGR from 231 Crores in 2009-10 to 438 Crores in 2014-15. In year 2004-05, company had top line of 75 Crores. Thus, over last 10 years, company’s top line has grown at CAGR of 18%.

-

Company’s net profit has grown 37.5% CAGR in last 5 years from 17.9 Crores in 2009-10 to 105.98 crores in 2013-14. Over last 10 years, ENIL’s net profit has grown CAGR 25%.

-

Company has maintained a very healthy balance sheet throughout last 5 years. Company had marginal leverage in 2009-10, however since 2010-11, company has zero debt. In last 10 years, in only 4 years, company had debt on its balance sheet

-

Company has consistently increased its investment (mostly parked in liquid mutual funds) from 40 Crores in 2009-10 to 549 Crores in 2014-15. This clearly suggests that there is significant free cash flow in the business. Company has been parking the cash in liquid investment, quite aligned with the peculiar business requirement of making large one-time payment for renewal of license and acquiring new licenses.

-

Working capital management reflects effectiveness of the management in running the operations. ENIL’s working capital requirement has consistently declined from 48% of revenue in 2009-10 to 14% of revenue in 2013-14.

Key Ratio Analysis

-

It is important to recognize that for ENIL, ROIC is a much better measure return profile of the business and not ROE or ROCE. The primary reason lies in the inherent business model where Company retains and accumulates cash generated from it to be utilized for acquiring more frequencies in the next round of auction. Thus, ROE and ROCE during this capital accumulation phase, will look artificially subdued. However, ROIC, over a long duration will give a more realistic view of the business.

-

However, it is important to recognize that, from time to time, as company deploys additional cash for acquiring new frequencies and renewing existing frequencies, the return ratio will dip for the time being (as the money spent will increased the fixed asset-e.g. period from 2007-10) till the depreciation will reduce the gross block and income will start flowing from new stations. I believe that looking at the business model of ENIL (and other radio companies), IRR is the right matrix to evaluate the company’s capital deployment efficiency

Key Growth Drivers

Phase-III Auction: Currently, there are 245 operating FM channels present across 88 cities spread through the country. At present, FM channels are mainly present in larger cities with very limited presence in smaller towns. Since 2005-06, there has been no new channel awarded and hence, the volume growth and reach of the industry has stagnated. Under Phase-III, GoI is planning to issue FM channel license in additional 227 cities and total number of channels is going to increase to 839, which is more than 200% increase from current level. Higher number of channels will improve the inventory for the ENIL and thus aid volume growth. On the other hand, increased reach will lead to higher realization for the company as national advertisers will be able to pay more for addressing the larger audience base. Thus, Phase-III expansion, in medium term will drive both volume and value growth.

In the first batch of phase-III auction, ENIL has won frequencies in to 7 new cities and 10 new frequencies in existing market. This combined with its acquisition of TV Today’s radio business, it has acquired 4 frequencies in new markets and may acquire 3 additional frequencies in Delhi/Mumbai/Kolkata if the MIB approves the transfer of frequency. In all, it’s number of channels have increased from 33 to 52 and may go to 55 if the Delhi/Mumbai/Kolkata frequency transfer is approved by MIB.

Improved Realization: Even though ENIL enjoys significant lead in terms of listenership over its peers in number of cities that it operates in, it has not increased the advertising rates for last many years due to sluggish economy, idling inventory and lack of awareness about radio’s attractiveness as advertising medium. Typically, for a 10 second slot across network, the realization for ENIL is 10,000 while the same is 100,000 for a TV chanel (General Enterntainment). Thus, there exist a vast difference in advertising rates, which even if adjusted for the lack of visual impact (present in TV advertisement), may provide good room for radio players to increase the pricing.

Now, as the sentiments are improving in the economy with revival is in sight and inventory levels getting utilized more than 100%, company has initiated the price hike from December 2014 across most of its markets. Thus, this will be another kicker for growth in medium to long term. In the Q2, FY 16, management indicated that the pricing has increased by 7.5% YOY and management intends to continue focus on increasing pricing.

Activation & Event Business: In addition to the radio business, ENIL has also successfully experimented and scaled up non-radio business which caters to events and activation by leveraging the brand and reach of the radio business. We believe that this business is still taking baby steps, however with increasing reach of the network, ENIL’s creative and marketing teams’ ability to create value proposition for advertisers and demonstrated track record of activation/events to generate decent return for advertisers, in the long run, this can provide fillip to the overall growth of the company

Monetizing Digital Presence & Other Opportunities:

ENIL was the early adopter in radio industry in going digital. It has launched highest number of channels (currently stands at 13) in association with gaana.com. Management has indicated that they have started monetizing this digital properties and though the current contribution from digital is miniscule it is likely to go up significantly.

ENIL is also looking at other innovative opportunities like running airport radio at the large terminals. It recently entered into agreement with Delhi International Airport Limited (DIAL) to start providing airport radio services at T3. Though, at the moment, it is still at early stage, such unique opportunities can be monetized and provide fillip to the base business.

Competitive Advantage:

Strength

Company enjoys reasonably strong competitive advantage due to combination of

• Strong brand of “Radio Mirchi”

• Pan-India presence with presence across all A and A+ category cities

• Pedigree of Bennet Collemn& Co which provides a distinct advantage for sourcing the advertisement and cross selling to existing client of the group

In addition to above, another significant advantage for the company isits profitable operations during the testing times in last decade when most of its peers lost money heavily. This has provided company with very strong balance sheet and a war chest enabling it to take maximum advantage of upcoming auctions and carve out future growth path. Ability of financial resources may be a constraint for some of the existing players during the Phase-III auctions.

Sustainability

We believe that combination of “brand” and “reach” has created a competitive advantage which is sustainable at least in medium term. Management has clearly identified the strategic importance of brand has invested significant sums of money in brand building consistently over last few years.

We believe that the strong brand of “Radio Mirchi”, management’s focused and sustained efforts to build the brand, its leadership and presence in most of the metros/category A cities and increase in its reach post Phase-III expansion will not only ensure the sustainability of its competitive advantage but also strengthen it further.

Quantification of Competitive Advantage

I strongly believe that mere mention of “competitive advantage” or “moat” may be misleading and may tempt us to rationalize some mediocre aspects as competitive advantage. Thus, it is important to look for the competitive advantage translating into/reflected in numbers in at least one of the following ways for company to benefit from it.

• Pricing power (ability to command higher prices as compared to peers)

• High Entry barriers (high market share for a long time)

• Cost leadership (ability to be lowest cost producer without impacting margin for long time)

Pricing Power:

ENIL is enjoying significant pricing power as compared to its peers. In fact, a close analysis at advertising rates data (compiled from publicly available sources as attached in separate Excel file ENIL_Premium_pricing.xlsx (15.6 KB)) suggest following

• In 21 out of 32 cities that it operates in, ENIL commands more than 20% higher price than its nearest competitors.

• In 15 out of 32 cities, ENIL commands more than 50% price premium over its competitors

• In only 6 cities out of 32 cities, ENIL’s pricing is at discount to its nearest competitor

Management Quality

Capital Allocation:

Positives:

• Management is very focused on deploying the capital efficiently and this point has been reiterated by the management time and again during its conference call commentary.

One of the events that may lead to sub optimal use of capital is Over paying during the auction to acquire new frequency to achieve higher growth Management is extremely cautious in this regard and has consistently maintained that they will not pay “irrational price” for new frequency just to ensure growth. Management has indicated number of times that company’s focus is on becoming the most profitable network and not on becoming the biggest network. In fact, one of the important reasons for ENIL remaining profitable while other players incurred significant losses during last many years, was that ENIL refrained from overpaying for acquiring new frequencies during Phase-I & Phase-II.

• Company has consistently maintained that it will retain the cash with it to ensure the sufficient war chest for bidding in Phase-III. This is appropriate considering high return generated on the capital employed by the company.

• Management has also indicated that after accounting for the capital needed for Phase-III bidding and expansion, surplus cash will be distributed liberally to the shareholders as dividend.

Negatives:

• In the past, company had invested money into non-radio media businesses such as outdoor media and made loss during the slow down. However, realizing that it was a very asset heavy business, management sold the business off.

Corporate Governance

• Company has been run by professionals and there seems to be no interference of the promoters in the day to day running of the operations.

• Company’s annual reports are fairly good and provide a good overview of the business.

• Company conducts regular conference calls and management makes all effort to provide satisfactory answer to investors’ queries

• Accounting policy are prudent and disclosure norms are adequate

Valuation:

Currently company has market capitalization of 3157 Crores. In FY 15, company made net profit of 105 odd crores and cash flow of 95 Crores. Thus, company is trading at 30 times TTM basis. Without factoring in Phase-III business opportunity and base business growth of 15%, the business is available at 25 times FY 16 earnings.

Disclosure: Invested in ENIL at average price of 450 with allocation of 10%

Disclaimer: This is not an recommendation and Investors shall do their own due diligence before taking an investment decision.

@desaidhwanil Thanks for prompt reply. I do agree that the IRR assumption does seem to be quite conservative. I am also cognizant of the fact that having multiple frequencies in their key markets will allow them to earn incremental revenues on much higher margins due to operating leverage. But just to play the devil’s advocate, let me try to put things in numbers.

ENIL has invested close to 350 crores in the auctions, which means that in order to meet the post tax IRR assumption, they’re need to earn additional cash profits of 55 crores (350 crores X 16%) or so. Additionally, they will also need to recover close to 25 crores they will lose by way of interest income (post tax). So essentially, they will need to earn an additional 80 crores at the end of their stated gestation period of 2 years in order to justify the Investment.

Currently they earn between 120-130 crores post tax cash profit (after adding amortisation charges)

I feel is that this will be a steep challenge. I have no doubt on the management’s capability but I think if anything goes wrong the downside is not protected at these valuation levels

But I would love to see your calculation on the IRR if you don’t mind sharing it. Just so that I know where I’m thinking incorrectly.

Hi Sachit,

Here is my sample calculations of IRR for old stations (post migration fees) and new frequencies. ENIL_IRR.xlsx (13.3 KB)One can put in specific numbers for a city such OTEF (cash out flow), capacity utilization, realizations etc. It is important to note that the IRR is as right or wrong as our assumptions. ![]() Hence the critical thing is to get our assumptions right. Following is the basis of my assumotions

Hence the critical thing is to get our assumptions right. Following is the basis of my assumotions

Capacity utilization: Conservative than Phase-II utilization in initial years (50-60% in 2 years)

Number of slots: 17 hours a day- 14 minutes (@100%) in an hour - 6 10 second slots in a minute

Realizations: Lower/equivalent than existing realization from the city or based on other player’s realization

EBIDTA: conservative than estimated Phase-III EBIDTA margins

Tax rate: 30% flat

It is important to remember that this is all equity IRR. Any leverage will improve the IRR. You will also notice that migration has come at very low rates and IRRs are excellent going forward. Even management has acknowledged the same.

Though, I have not calaculated IRR on overall basis, one can replicate this sheet and change assumptions/variables to arrive at cumulative IRR.

Thanks for sharing the insights from industry insiders.It really helps in crystallizing the thought process. .

You are quite right in pointing out that ROIC may go down. I think that is the nature of the business and the way accounting is done. In fact, the best way to look at this business is through IRR model as company incurs one time license fees and then the capex is amortized over the life of the license period. It is very very similar to project financing.

Having said that, since large portion of fixed cost increase (non-cash) in P&L is going to come from amortization charges thus impact on EBIDA will not be much but PAT will be impacted. On the other hand, the accurate reflection of such businesses shall be cash flow and not PAT. Thus one must look/value the business based on cash flow instead of PAT. Your point of high fixed cost being double edged sword is very valid as most of the time when we talk about “operating leverage”, we discuss that in positive light, but that is not how situations pan out in business.

On drop in margins, in fact, management on record, has mentioned that even after incremental fixed cost and initial expense for new launches, on overall basis they do not expect EBIDTA margin to dip by more than 1%. That came as positive suprise to me as I was expecting decent dip in margins due to negative operating leverage. This minimal impact is due to couple of factors

- There is very low additional fixed cost incurred for second and third frequency

- Compared to Phase-II, radio industry has matured much more thus capacity utilization ramp up will be much faster. In fact, if they can achieve 30-40% capacity utilization, they may break even at EBIDTA level

desaidhwanil,

Latest presentation of 2Q16 shows a debt of 139cr. mgmt previously said cash balance is sufficient for phase - iii auction fee, looks like it is not the case now.

Also can you help understand why do you say roe is not good measure for enil? investor will not benefit if most of the accumulated cash is used for frequency acquisition right? I was expecting roe to reach some good number after some time from frequency auction. Is that expectation wrong? last 10year/5year/3yr roe from screener is 10.25/13.6/13.87 which is not great number.

Thanks in advance !

Hi Arjun,

In my understanding, management had always maintained that it will need some debt to fund the renewal of existing frequency and acquiring new frequency in Phase-III. In fact, management had indicated in Q2 Concall, that they had spent around 50 odd crores more than what they had budgeted for which I feel is commendable in the context of extraordinary high prices paid for some frequencies by some bidders. So, My understanding is that 150-200 Crore debt was always on cards and it quite manageable in the context of their very strong cash flows of 100 odd crores + (and growing!)

Coming to ROE, as I mentioned business has two distinct characteristics

- Cash flow is much more than PAT after few years of auction thus ROE (which is PAT/Total equity) is not an accurate measure as it understates the returns from the business

- Secondly, by very nature, this is a business where business accumulates cash an then deploys it at once (during auctions and renewals). Typically, such cash flow focused businesses are evaluated on IRR basis and ROE may not be a right measure.

Though, ROE is very good measure for most of the businesses, it may not be an optimal one for few. This is one such business where ROE may give a wrong impression of the business characteristics