Initiating a second thread on EMS Limited, because the previous one here is locked.

EMS Limited is a multi-disciplinary EPC company, headquartered in Delhi that specializes in providing turnkey services in water and wastewater collection, treatment and disposal. EMS provides complete, single-source services from engineering and design to construction and installation of water, wastewater and domestic waste treatment facilities. - Screener.in

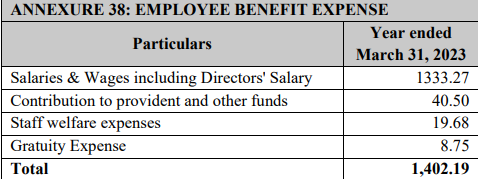

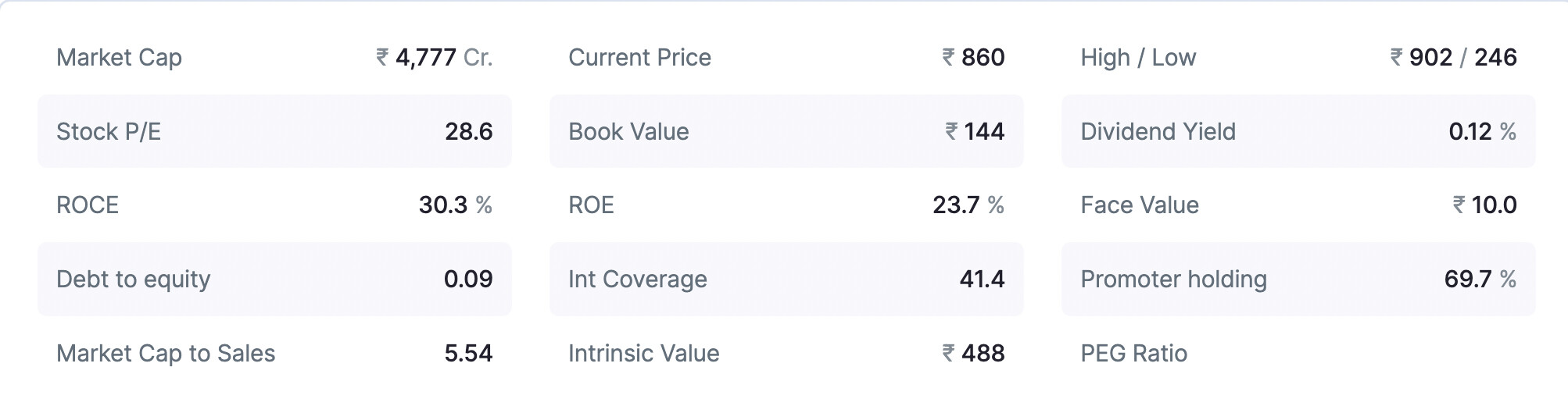

Financials -

Note:

- Current P/E is higher than the historical P/E (~24) of the stock. This can mainly be attributed to the increased national budget allocation towards water supply and waste management projects.

- Low on debt.

- Decent ROE.

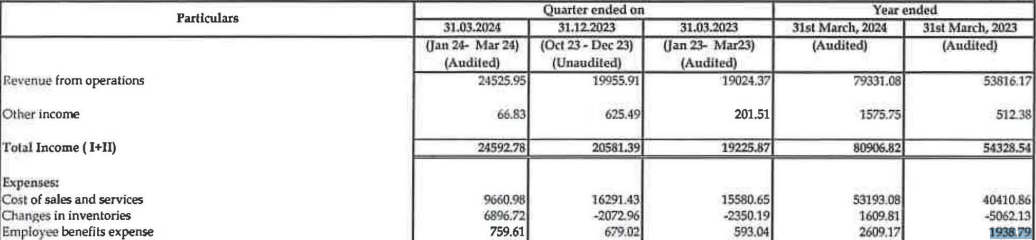

Profit and Loss -

Note:

-

Consistent top-line and bottom-line growth.

- Top-line growth from the past 2 financial years has been around 48%. Bottom-line has grown around 39% in the same time period.

- The TTM top-line growth is around 43%.

- In the February 2024 con-call, the management has guided towards a growth of 35-40% in the current FY.

-

OPMs are decreasing with scale. Still significantly higher than competitors, ION Exchange and VA Tech who have averaged around 10-13% OPM.

Promoters -

Couldn’t find anything interesting about the promoters Mr. Ramveer Singh and Mr. Ashish Tomar other than what is mentioned on the company website, here.

Business Overview -

The operations of the company can be broken down into the following broad categories.

-

Sewage Networks

- 60-70% of the order book.

- Commands higher margins. This is the main reason behind the higher margins enjoyed by EMS limited compared to its peers.

- Promoters say, since there is a lot of work to do in this sector, they’ll maintain this share of sewage work in the order book and thus continue enjoying the higher OPMs.

-

STP and other construction.

- 30-40% of the order book.

-

O&M is currently 10% of annual revenue but according to the promoters this should increase with time.

According to ICRA, by the end of January 2024, the pending order book of the company stands at ~2093cr, which is to be completed in the next 2-3 years.

Recently the company was awarded two more orders,

- First from UP Jal Nigam, an STP project worth 119cr, where EMS would have a 26% share in a JV.

- Second from Uttarakhand Power Corporation. An infrastructure project to reduce energy loss during power distribution. EMS has a 95% in the project.

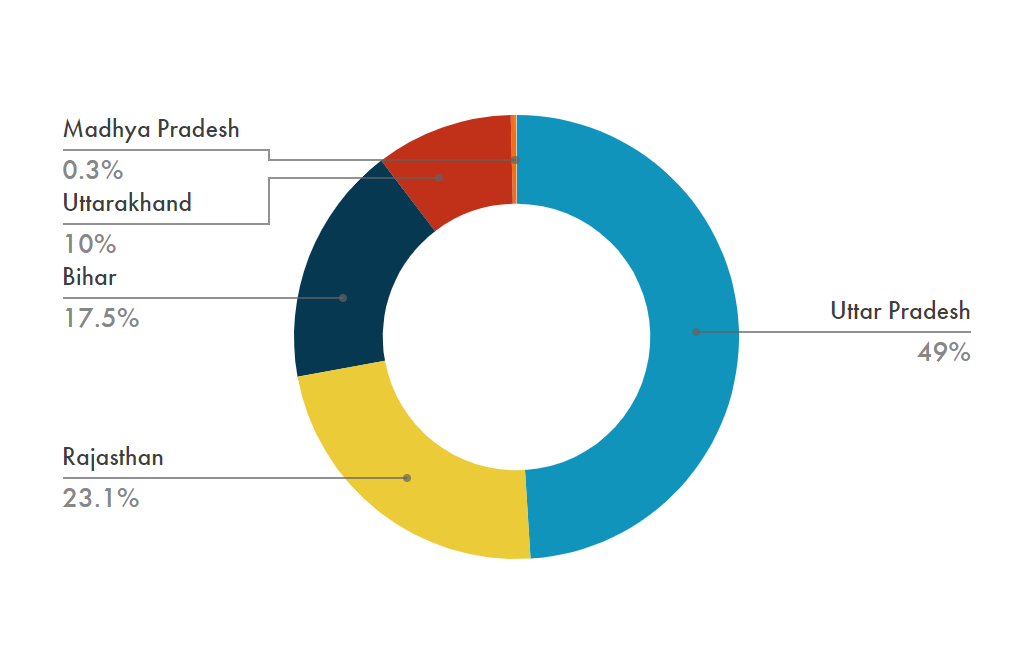

The company’s main revenue comes from north India, mainly from Rajasthan, Uttarakhand, Uttar Pradesh and Bihar. The company is also bidding in MP, Jharkhand and West Bengal. They have also shared the intent to expand to other states, but haven’t given anything concrete yet.

The company directly deals with the government and does not do any subcontracting for the work. Only labour is sourced from contracting. The equipment is sourced via rentals and thus company capex is very low.

Company’s projects are usually funded by the central government or agencies like, Asian Development Bank, World Bank, etc. So the company doesn’t generally face any payment or funding related issues.

The company has announced acquiring Brijbihari Pulp and Paper Pvt Ltd. It is not clear how this acquisition fits into the competencies of the company.

Key Risks -

-

Business relies on government spending and thus is susceptible to policy changes.

-

The company is a little defensive about project choices and wants to ensure higher margins. Increase in competition might hamper the order wins and margins of the company. As of now, the company is awarded only 12% of the orders it bids for.

-

Troubles with the law

- The company was recently investigated for GST irregularities.

- The company was black-listed by two government agencies for the death of 5 labourers due to lack of adequate safety equipment (only read it here).

- Another unrelated black-listing order was quashed by the Bihar High Court.

Disclosure - Invested from lower levels.