There was peculiar commentary during the company FY25Q2 concal. I will summuraise the gist of it:

The company is planning to acquire some paper company for 50 crores only for its land and then use it as mortgage for banking facilities. The paper company has annual revenue of 50 to 60 crores but the company is not interested in running the plant and would scrap it. I mean acquiring land by paying money and then using it as collateral for banking.

Why do this: is it because company has the excess cash and wants to buy a fixed asset and lose the value of money over time?

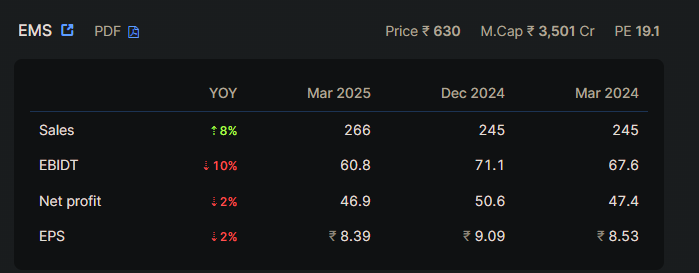

Growth and Performance: EMS Limited has shown strong financial growth over recent years, with significant increases in revenue, EBITDA, and net profit.

Corporate Governance Concerns: There have been past issues related to safety and reporting inaccuracies, which have led to penalties from authorities. These issues suggest potential concerns regarding the company’s corporate governance practices.

Dependence on Government Projects: The company’s reliance on government projects poses a risk, as changes in regulations or government priorities could affect its revenue streams.

Overall, while EMS Limited has demonstrated solid financial performance, the past issues with authorities and the dependence on government projects are areas that investors might consider as potential risks. It is important for the company to address these governance concerns to maintain investor confidence.

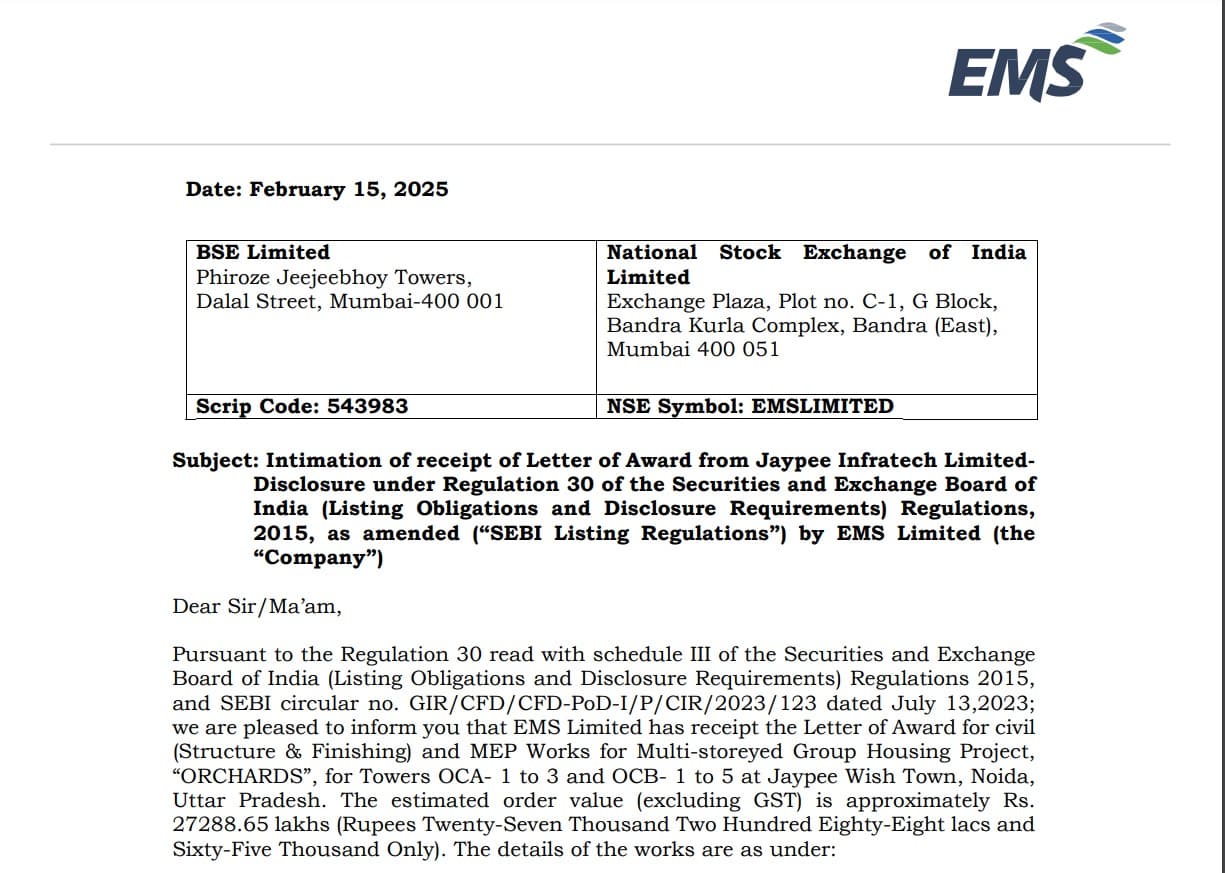

Receipt of letter of award from Deltabulk Shipping India Private Limited of Rs 105.08 cr for Development, Operation and Maintenance of the Multimodal Logistics Park (MMLP) at Nagpur at Sindi, in Wardha District in the State of Maharashtra through Public Private Partnership on Design, Build, Finance, Operate and Transfer (DBFOT) Basis

I want to understand one thing. They bought BRIJBIHARI PULP AND PAPER PRIVATE LIMITED for 50 crores, where Ramveer Singh is already a promoter. They mentioned that they acquired it through NCLT. They claim they are not interested in the machinery or operations, only in the land, to use it as collateral for debt.

How can we be sure that the land is actually worth 50 crores? What if the market price is much lower? This seems like a red flag to me.

Does any fellow investor have information about that land or any other insights?

slight concern though here as promoter has pledged a fair amount of his shares. especially with the gensol saga that has just happened. would like to get community’s view on this