Only the interest component is taxable. Rest all is tax free

1 Like

The Quarterly payout by these REITs have lots of components… One of them is dividend which is tax free, other is interest which is taxable… Others include amortization which is also tax free… Read the latest quarterly results of any REIT, you will get better understanding…

3 Likes

Results for the quarter ending Sept’22 came out y’day, post market.

Liked ![]() the Distribution mix …5.46 total (only 0.86 in interest and the rest in Dividend and Amortization)

the Distribution mix …5.46 total (only 0.86 in interest and the rest in Dividend and Amortization)

NAV is 400

Conf call recording

PS - Invested recently

4 Likes

We had another round of fall today (2%)…Looking at similar fall in Invit like PGInvit, I assume that it is related to the forthcoming rate hike by RBI…and not any other core issue that is contributing to the fall

The total payout by embassy is mentioned under taxable component in my 26AS. Is the dividend and other income taxable in the hands of receiver or completely tax free?

1 Like

Hi @dd1474 - while call and commentary seemed fine and discount to NAV has expanded with recent corrections, would be great to hear your point of view - thanks.

@Dev_S

Thanks for your kind message. In my understanding, there are times with no fundamental changes, the market prices moves away from core value like penddumlum swing. However, extreme optimism/pessimism is known only in hindsight. Currently, I see couple of factors driving decline in Embassy unit price in last quarter:

- Liquidation from the Promoters

- Expected increase in interest rate

- No substantial increase in distribution despite higher than anticipated performance hotel business. (On conference call management did mention that margin/cash for distribution are lower in percentage terms from hotel business then commercial rents)

Further, management did suggested exploration of development in new building in existing complex/SEZ related issues/ acquisition of Chennai office park. All these factors, while good in long terms, in medium term are unlikely to result in improvement in distribution. Hence, in my understanding, prices are likely move in range bound, till the distribution per unit increase. This is my understanding and may be completely wrong.

Discl: I have holdings in Embassy REIT. My view may be biased. Not a SEBI registered advisor. Not a substitute for debt class. Not recommending any investment action

11 Likes

Agree with Dev. The only other additional variable is the overall demand and incoming lease supply in the Bangalore micro market. My anecdotal understanding is that the micro market is tight for Grade A facilities although thanks to the low interest rates up untill now, additional supply is likely to come in. That may have some downward pressures on rentals. Typically there is a lag between interest rate cycles and physical demand and supply cycle. However long term would still say fundamentals look decent

2 Likes

There has been some negative development in respect of Embassy Property Development group as per Credit rating report from Acuite. I am enclosing copy of the document.

While it does not have direct impact on Embassy REIT, still the unit offered by Embassy Group as collateral for structured NCD, in case of stress may result in distress liquidation and may have impact on price in short term.

Discl: I continue to hold my investment with close monitoring on development. Investor shall consider his/her own risk profile and take investment decision. I may change my view and act on my investment (including selling) without informing forum.

Embassy Developer Acquite RR BB Rarting 11Nov2022.pdf (152.4 KB)

10 Likes

Thanks for pointing that out Dhiraj. A few things to note (playing devils advocate here) is that the information that this report provides around the 80 odd crs of delay in payment by EPDL has not been audited by the agency. Some of it has been mentioned as “verbal” in nature.

As far as Embassy REIT is concerned, I completely agree with you that there could be slight pressure on its stock price IF the report is accurate and there is distress liquidation since the units are offered as collateral against the NCDs.

Once again thanks for sharing and do let us know if you find any such updates ![]()

This is dated 24/10/22 and I am putting it here, for those, who did not get time to listen to the concall

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=668372da-5143-416e-85eb-677d758845c1

Highlight is the FY23 guidance of DPU of ₹21.70 per unit

And here is the half yearly report, that came out on 10th Nov

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=9b1927fe-a006-4c48-90f4-1e76c05531a7

The fall in REITs continues but embassy continues to fall, to a higher degree. I am part of various REIT specific whatsapp groups and there is panic, esp from people who are at 10-20% average, higher than the current price. In the meanwhile, the price action continues to be weak, esp in Embassy. A cocktail of factors (enumerated above) seems to be drowning it and I am not sure where it is going to halt…

PS - Adding small quantity in every fall but …with some degree of fear. The only thing that makes me think is this factor - look at the investors, who would hv loaded up when IRB Invit fell between 2017-2020 (different sector, different style compared to REITs but.,)

I think based on Q2FY23 con calls of all REITS, things seem to be alright. EMBASSY have a guidance of 5msf of leasing for this qtr. They’ve actually managed to capture more than 60% of this already.

Other REITS also seem to be on track to meet guidance. We may be nearing the peak of interest rate hiking cycle. If interest rates peak out soon and rates start to fall, this would further add to the tailwind.

EMBASSY also said that a recessionary environment works in favor of India as offshoring work demand increases and MNCs get some of the best in class properties at less than a dollar psf.

Disclosure: I am also holding REITS and INVITS and I am adding with every fall. Near term price of REITS May see some pressure which may be a good opportunity to top up given that it gives a better yield.

2 Likes

Why reits have debt?

If they are supposed to distribute minimum 90 percent of operating cashflow, how are they supposed to pay interest on debt and keep on building new property.

2 Likes

Plese read this thread and REIT thread since beginning. After reading, in case you have any question,please directly write to me or put on forum.

4 Likes

This may have been answered earlier, but unable to get full clarity on below points about REIT distribution:

- Dividend component is well understood: Rental income after expenses

- Interest component: How is REIT able to generate Interest income? In fact they should have interest expenses for the loan they take for new constructions

- Return of capital: On one side REIT is taking loan or issuing new shares for new construction, and on the other side they are returning capital to existing shareholders. This is not adding up. Is this just to keep DPU artificially high? If yes, then we should remove this component from our yield calculation as they are returning our own money by raising capital somewhere else.

Can someone throw light on #2 and #3.

Thanks!

3 Likes

This is interesting. I wonder how insulated is the management of Embassy REIT from the Embassy group?

1 Like

Yes truly that is a risk. The article almost expects the REIT to buy the Chennai property of Embassy group, which should not be a foregone conclusion.

Now with Embassy Group + Blackstone shareholding below 40%, I hope the institutions vote against buying of properties which don’t add substantial value to the REIT.

Buying the Chennai asset must not be rushed through with dilution at these low prices

4 Likes

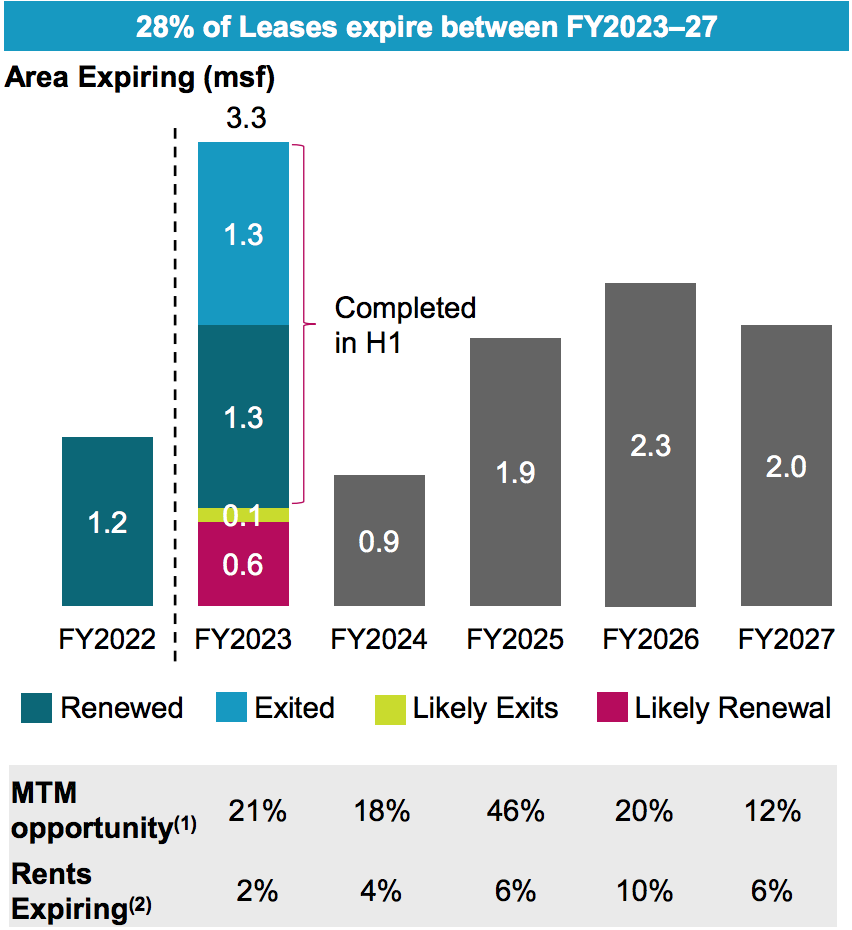

The investor presentations mention MTM opportunities on the rent charged for the following years but i have some question to more experience members who have watched the reit over the years

-

have the mtm opportunities actually played out in the past or is there a leakage

-

Generally that is the increase in DPU you’re woking with ?

1 Like

Prices for REIT according to me are the most affected by interest rates. I like to treat them more as a debt part of my portfolio. The alternatives I have currently for this portion of my portfolio are-

- Fixed Deposits- Currently one can get about 6-7% pa return in any bank’s FD with least risk on principal. After taxation of 30% this amounts to anywhere around 4.2-4.9% pa.

- Debt Mutual Funds- Currently we can find good funds with 100% funds in AAA rated securities with yield to maturity anywhere around 7.25%. Post taxation this return would be around 5.01% (STCG) and 5.8% (LTCG) if invested in a growth variant.

- REIT’s- Embassy Reit currently with ₹21.70 DPU and about 85% of this being tax free gives a yield about 6.2% (at cmp-330).

For me this higher yield with optionality of principal to grow (which is absent in other 2 alternatives) acts as the deciding factor in choosing Embassy REIT at cmp. Even higher yields if prices fall further should act as support. At all time low of 310 this yield would increase to 6.65%.

Around 29% (9.8msf ) of completed area (33.4msf) is under construction, rent escalations of 15% every 3 years,19% MTM of rent and increase rental of SEZ if Desh Bill plays out are some growth triggers for growth of rents and hence DPU in mid to long term.

Risks I can see are-

- Liquidation by Embassy and Blackstone (Weak shareholding pattern by Sponsors).-This along with interest rate hikes has played out and is the reason for such sharp fall in prices. This for me will be the biggest risk if the horizon is short term.

- Further increase in interest rates- According to most reports the interest rate hike will peak with one more hike of 50bps as inflation is under control in India currently.

If that happens the all time lows may get tested again but yield of 6.65% should act as support.

- Recession led vacancies- I don’t consider this as a risk as India is seeing high growth and even more interest from foreign companies. Increased outsourcing in India to reduce costs should also lead to filling up of office spaces.

Disclaimer: Recently bought Embassy REIT and will add in second tranche after December rate hike. Please consider your own risk profile before taking any investment decision.

11 Likes