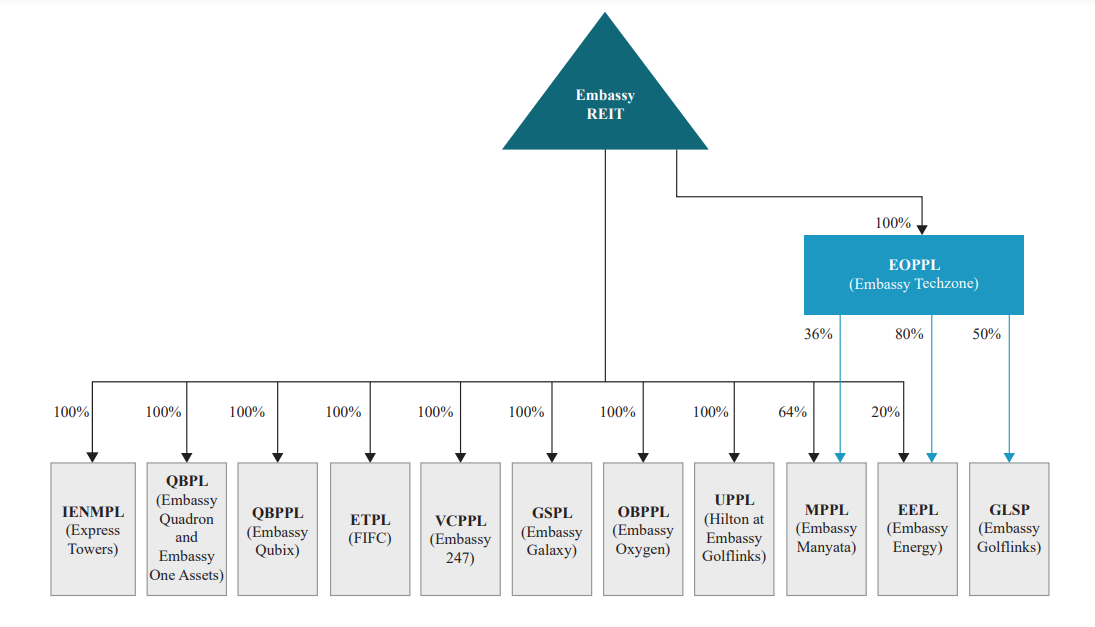

As Embassy REITs holds only 50% through Equity in Golflinks, It will receive 3 types of cash inflows from Golflinks : A) Dividends (Subject to approval from Golflinks unit holders, essentially includes rental incomes) B) Debt repayment C) Interest on the debt.

Hope this explains.

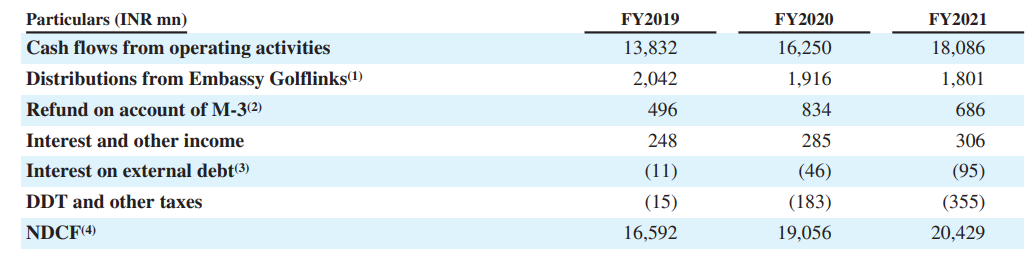

Source : DRHP document Embassy REITs

Disc. Invested

I have also wondered about this, but could not understand the report filings. Thanks for the info. Also thanks to @valuegrowth for asking the question.

There are mutiple factors which work in valuation of REIT, which include Net asset value, occupancy, lease rental, micro market real estate prospects of the REIT, distribution and expected growth prospects. Currently, Mindspace is offering maximum distribution for the investors in tax efficient way. While gross yield is lower than Embassy REIT, the post tax yield for each individual would depend on their marginal income tax. For highest tax bracket investors, due to tax efficient pattern, Mindspace REIT may offer maximum return and hence may be willing to invest at higher price. That could be one reason for difference in discount/premium to NAV market. There could be mutiple other facrtors like expected distribution acceretive new assets, financing high cost debt with lower cost debt, expected major lease announcements or reduction in occupancy rates which would vary over the periods. So very difficult to put one or two specific reasons for differences in valuation. I know that my answer is not specific, but this is best answee I know.

Thanks for seeking my view. Wish you happy investing

Discl: I have investment in Embassy REIT, hence my view may be biased.

I wouldn’t know exact reasons. As @dd1474 highlighted, there could be many. I can also add couple of more possible reason, recently Blackstone sold a part of their holdings in Embassy, this could have put some short term pressure on it’s stock price. Another reason I could think of is that largest presence of Mindspace is in Hyderabad market and most of those parks are new or upcoming. I think market could be factoring in occupancy increases here. Hyderabad market is very hot.

For me, I always buy equal quantity of units of Embassy and Mindspace, it gives me good exposure to Bengaluru, Mumbai, Pune and Hyderabad markets. If someone is interested in Noida / Kolkata markets then he / she can also look at Brookfield REIT. (I am also waiting for DLF REIT to add exposure to Gurgaon market).

Interesting you would buy all 4 REITs if listed…how much percentage allocation to overall portfolio do you think is appropriate for REITs? Also I think NCR, Kolkata and Gurgaon market may not be as lucrative as west and some parts of South India with these two belts encompassing both financial and technology capitals & surroundings of India…

I can see the capital appreciation angle in REITs but all of them are in the 4-6% yield range post tax, whereas the 2 invits (Indigrid, IRB ) can double that yield. This is the reason, I stay away from REITs

I am not buying Brookefield REIT… For now I am staying out with Embassy and Mindspace, will add DLF when it comes and if priced reasonably. I am primarily interested in Mumbai / Pune / Bengaluru / Gurgaon / Hyderabad and Chennai markets.

Allocation, I am not sure, I guess it’s different for each individual.

PropShare fractional investment was supposed to acquire near Embassy Tech Hub (Phillips office) in Bangalore but has lost the opportunity to Embassy REIT. In general REIT will have favoured buying power, just posting as scuttlebutt info!

Embassy REIT has corrected significantly recently. Any one aware of specific reason here.

Mindspace is quite steady here compared to Embassy price erosion.

The prices of Embassy REIT may be have declined mainly due to selling of Units by Promoter group Blackstone entities. Further, increase in interest may also impact adversely in short, the currnet hike in interest rate is due to higher inflation rate, which shall be good for REIT sector in long term, in my view. While finance cost would increse due to higher interest, the increase in lease from inflation would result in higher surplus cashflow for distribution in next 2-3 years. There could be some other reasons like change in office demand due to WFH culture. If that factor is playing, then i would be very cautius for my holding. We would get that answers probably in second quarter results. Till then i would continue to hold by investment.

Disclosure: I consider InvIT/REIT as my fixed income portfolio. Embassy REIT is my second largest holding after RBI Bonds. Hence my view may be positively biased. Not A SEBI registeed advisor. No trade in last 3 months. Not recommending any investment actions.