@pskrishnan

If I’m not mistaken the value of ETV was checked by two independent sources and they then purchased it at a 4.6 percent discount to that valuation. I can’t find who the two independent valuators were though but that looks like standard procedure for valuating projects. Are their names available anywhere so we can check if they are related to Embassy in anyway?

Also, Is what you’ve heard from the commercial RE circles available in public domain?

I’ve seen Virmani’s name come up quite often regards governance issues but I’ve not really found anything tangible so far. What’s the view regards him in these circles?

Regards Valuations of commercial property… I don’t think anyone really knows the actual value of anything regards commercial projects in India and hence why it’s considered beneficial to buy companies like these only at a discount. In the future I’m not sure if it’s even possible to know if Embassy are overpaying or underpaying for a property so tracking Rtps could be fruitless… but buying at discount to NAV gives a margin of safety here for investors.

Cheers

Disc: invested

@Malkd The ETV valuations were done by iVAS (CBRE) and Shubhendu Saha (Independent Valuer). The info around overpaying for ETV is not available on public domain, I have heard this from one of the leading Commercial Real Estate property consultant (likes of JLL, CBRE, Cushman types). I will try and get some additional info around the rumor on valuation mismatch

Agree with @Malkd on Real Estate valuations they are indeed very tricky. Would be interested to hear from group members on their views around the credibility of the NAV data provided by REITs.

The good part is, at 310, Embassy REIT is at around 10% discount to the recent QIP price, there is some comfort around that hoping that the QIP subscribers would have good due diligence to justify the QIP valuations

@pskrishnan, @Malkd Both the valuation reports are available at Embassy REIT website. 1st one is from CBRE and 2nd from Cushman and Wakefield. Valuation work seems to be very detailed.

Results and earnings presentation updated on website: Investor Relations - Embassy Office Parks

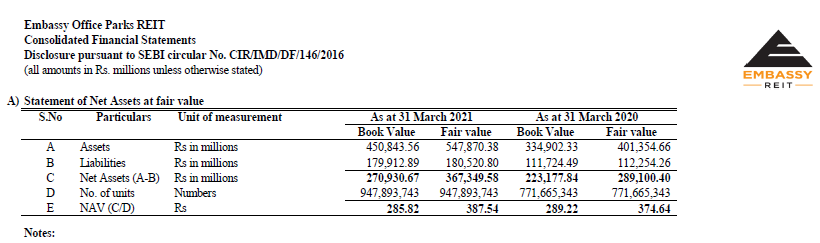

Income is stable, rent collection at 99.8 percent, rental renewals on track, short/mid/long term outlooks given in fantastic detail for anyone interested in the WFH argument. Occupancy hit a bit at 88.9 percent but medium/long term it looks like it will improve according to the presentation but is one of the things to look out for during concall. NAV valuated at rs. 387.54. Lots of details for anyone interested in the commercial Office space overall.

Distribution of rs. 5.6 for Q4 FY21. Best part is the new tax regime is confirmed at 78 percent tax free which is higher than I’d imagined!

Conference call today at 6.30 pm.

Edit on 30/04:

Attended the concall. Here are my thoughts… attended it yesterday so I may have misremembered some parts

- Even with covid raging they managed to increase rental rates by double digits. Shows that clients aren’t willing to let go of their under market rate rent

- Occupancy has been hit and with leases ending will continue to be hit for next 2/3 quarters. However, a lot of current clients and potentially new ones already negotiating for new space to accommodate huge surge in hiring. They are very bullish on the business post 3 quarters and they have no WFH fears

- ETV is already DPU accretive and they are changing the structure to make it tax efficient by September

- Debt at just 22 percent and they can use 126 billion to grow. This will be for developing within and with new complexes. These are covered in the Presentation… I can’t remember details now. Balance sheet is strong.

- They spoke about their debt via NCDs and maturing date + call options but tbh I can’t remember what was said in detail and don’t want to misquote it. It was asked by someone halfway through the call and should clear the doubts regarding debt that was discussed above.

- No guidance for FY22 understandably. They said they’ll give guidance around second half of FY22.

Tbh what I’ve summarised is a drop in the ocean. The opening comments alone clocked in at 35 minutes. Very professional concall as per usual and every little nagging doubt I had is gone.

Disc: Invested heavily at rs. 306. Doubled down straight away today morning at open post the concall.

Few quarters of patience will be needed but imo considering the class management and robust business model that allowed distribution during covid(in the USA most commercial office REITs I know of did not give a rupee/cent) along with growth in NOI, acquisitions, a strong balance sheet during this covid period bodes well for the future.

Not a sebi advisor

Today there is a full page ad of its previous year financial results in Economic times , Kolkata

Book Value is stated at Rs285.82.

Seems to be reasonably valued at CMP of Rs315 as of today

In my view, we need to take NAV based on market value. As per disclosure in Consolidated financial statement, the NAV based on market value has increased to Rs 387.54 per unit as on 31 March 2021 as against Rs 374.64 per unit as on 31 March 2020.

I am enclosing relevant extract.

Discl: Same as last post

Anyone has information about the JP Morgan 1.1msf leasing was done at what rate or it will be decided once the project is completed in Sep-Oct? Any other terms conditions of the same project like once delivered, it will start generating revenue ? I doubt they will get a few months rent free as its being build specially for then

@dd1474

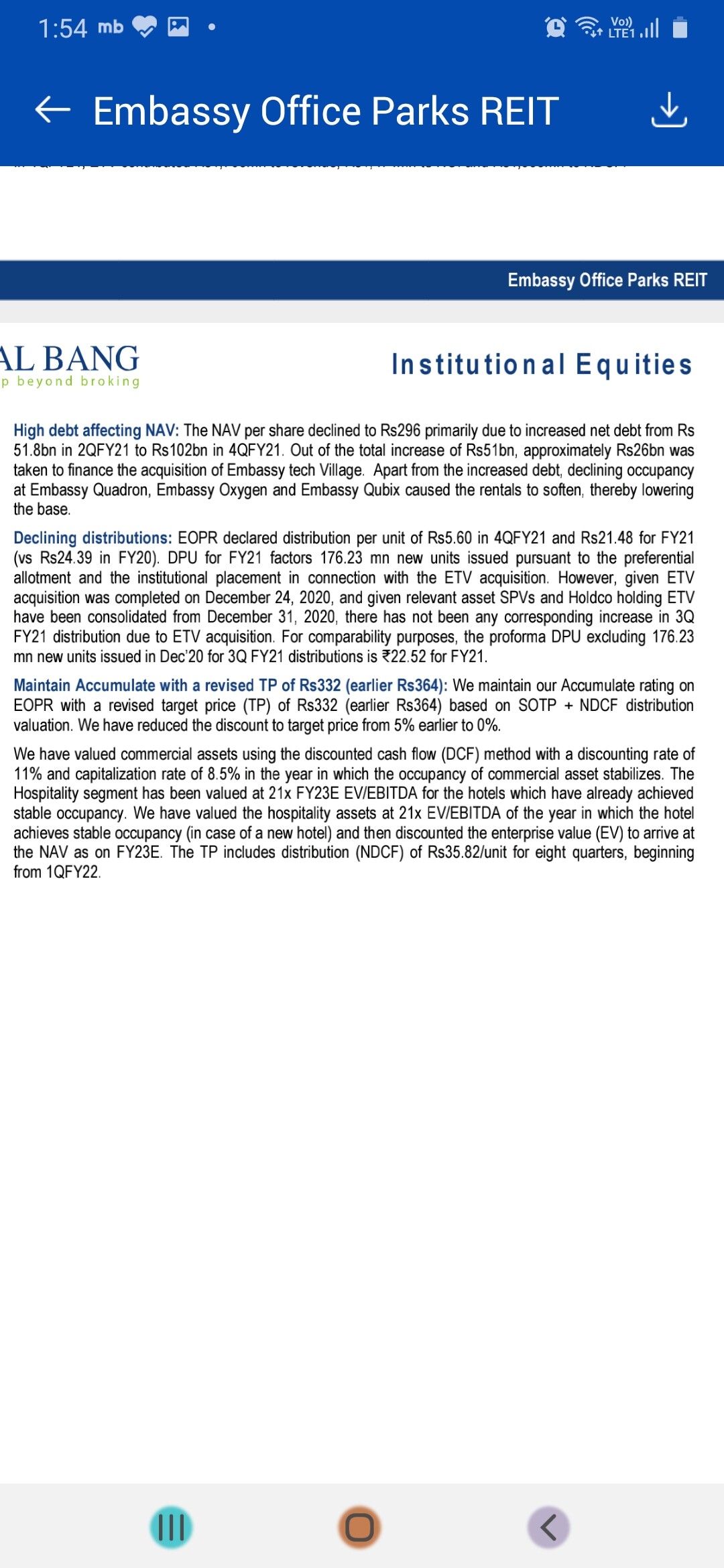

In the latest Nirmal bang report(it’s available for free in trendlyne so I’m assuming it’s safe to post a screenshot) they have reported NAV per unit as rs. 296/- due to increase in net debt. I can’t quite figure out why they’ve calculated it as 296 Vs the company calculating NAV at 387.54 per unit. Any thoughts regarding the discrepancy? Are they considering some other factors to calculate this?

Screenshot below:

Thanks @dd1474 … dint want to create a new post and clutter the thread so just edited this as a reply to your answer below. Looks like they have done their own independent analysis which highlights the wide range of valuations when valuating real estate. Managed to download the entire report below. Again, it’s freely available on the free plan of trendlyne so I’m assuming it’s safe to post. If not il delete:

File_1619945059241.pdf (463.4 KB)

I am not able to understand enclosed report working from summary part. It is my limitation. When the valuation report are providing cashflow, in my view, it would be better to work on that number with adjustment then to do separate working on sum of part method. While the method of Bang would be independent assessment, still has its assumption of capitalisation rata discount rate for real estate property. From enclosed sanpshot, only understanding I can develop is they have done for their own projection of cashflow with certain assumption and valued hotel assets from EV/EBITDA basis. Whether there assumption, I.e. projected cashflow, capitalisation rate, discount rate and Hotel EV/EBITDA is correct or wrong, I am among least competent person to comment on same. My apology for not being able to answer your queries.

@dd1474 my reading of the valuation report (being from the industry), probably can say if you want to be conservative their is a 10% -15% adjustment you can do to the valuation report shared here.

Plus, as a REIT investor - REIT management expenses and CAM Expenses are additional income to the sponsor (we should adjust)

Going through the results. While I largely agree with the longer-term view, it seems the short-term pain is not going to go away anytime soon.

They had 0.6m SF expiries during the quarter of which they were able to lease out 0.1m SF only. For FY22, they have ~1.9m SF expiries. With virus raging, it’s anybody’s guess how much they will lease out. Going by the current pace of leasing, the occupancy might fall further (~85%ish). Looking at this, the DPU for the next few quarters is likely to drop to Rs ~5 per quarter (or below?).

Although this all depends upon the virus spread and the pace of vaccinations.

@rishi87

Agreed. Next few quarters should be hit really badly. Dpu should be at approx rs. 5 too. And that’s the reason it’s available sub 320. Occupancy will fall to approx 85 percent too(on the plus side demand looks like it will come back with a flurry post covid increasing mark to market rentals for the vacated spaces)

Would the ideal situation be to wait for everything to improve and DPU to increase to rs. 7+ per quarter next financial year?

Yes.

Would Embassy still be available at this price when the situation normalises, WFH worries disappear completely and DPU increases?

Definitely not.

It would be priced closer to NAV by then. Considering this is a super long term investment and the amounts to be invested here makes sense to me only when it’s a significant part of my net worth the cheaper I get it and the higher yield the better from both risk(capital protection) and returns(yield and appreciation) perspective since I use it as a quasi debt instrument.

My main questions were:

Will demand for office space come back long term?

How will Embassy handle this horrible year?

Are growth plans in tact?

Will they survive and thrive post this period?

Will my capital be protected at sub rs 310(my average price is 308) and will my yield potentially increase to a majority tax free 9+ percent in 2 to 3 years?

And all my questions were answered satisfactorily post the ppt and concall and personally I feel I’ve got a sufficient margin of safety by buying at a discount which barely priced in the current Q4 tax free distribution too hence giving a nice cushion to weather the next few quarters.

Note: not a sebi advisor. A lot of personal opinions were shared by me in this post but I thought it was necessary to answer the question. So please flag if inappropriate.

It would be interesting to know what proportion of Embassy’s tenants are locked in as the live load along Outer Ring Road, Bangalore has been around 5-10% in most tech parks and we have not seen mass cancellation of lease contracts. Most companies wouldn’t have stayed the course for a year now if they didn’t need the space. I personally can’t see how work from home can continue in its current form as it is impossible to inculcate culture and look forward to career progression without physical interaction. Furthermore, with respect to Embassy’s assets in Bangalore, largely along ORR, the metro project has been approved which will be a long-term positive for the underlying assets; plus, the Bangalore-story continues to be strong compared to other markets in India. Does anybody know if Embassy’s delay’s on the residential side of the business has the potential to shakeup the shareholding/management of the REIT?

In my opinion, Embassy construction activity in residential market of business are in sponsor company. Being Trust structure, expect for maintenance work, new assets acquisition from Sponsor and Sponsor holding in REIT, Embassy construction future is no way connected. Even if in worst case scenario, Embassy group face insolvency, the way REIT would affect are from change on Unit ownership (Embassy unit being sold to new investor) and termination of ROFO (Right of first offer to completed real estate property). There is no impact on current operations and working of Embassy REIT in my view.

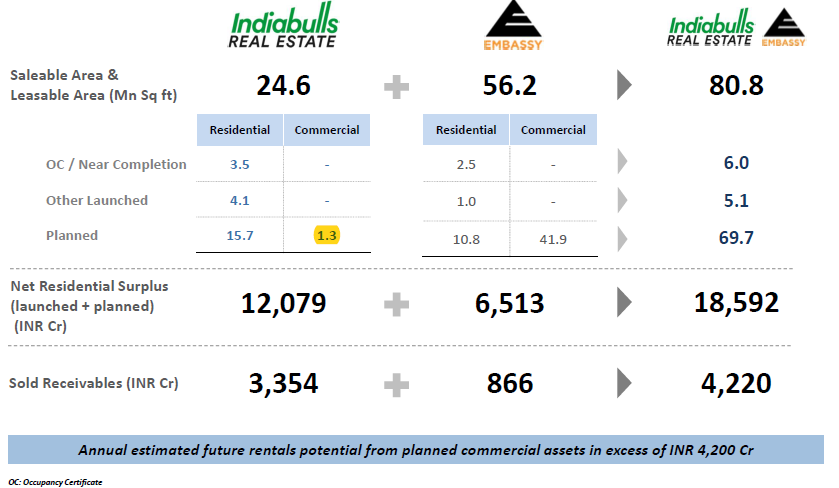

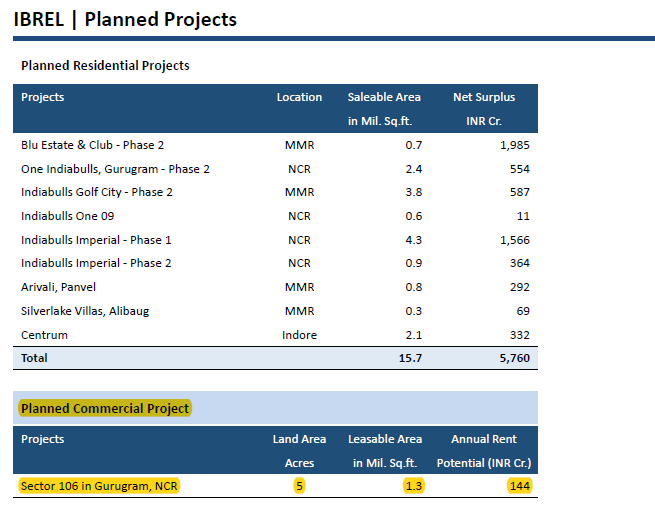

I tried to understand impact of proposed merger of IndiaBulls with Embassy group. There was a presentation done in August 2020. That presentation contained one slide which was relevant for Embassy REIT in my opinion which I am enclosing herewith:

As we can, see IndiaBulls Real estate has Planned Commercial estate of 1.3 mn sq ft. This is as compared with nearly 15.7 mn sq ft residential plan development for Indiabulls and nearly 41.9 mn sq ft commerical estate for Embassy.

The proposed 1.1 mn sq ft planned commercial real estate project is based on Gurugram, NCR region, with potential Annual rent potential of Rs 144 Cr as per same presentation.

Given that Embassy REIT mandate is to acquire and manage A Grade office building (commercial real estate), with just 1.1 mn sq ft of planned commercial real estate, the proposed IndiaBulls and Embassy merger is unlikely to have major impact for Embassy REIT in my opinion in medium term. The future would be broadly driven by acquisition from Embassy Group only which has lion share in planned commercial real estate. This is my view and it may be wrong.

This is based on US market. It might be dangerous to assume that same trend to apply to indian market although there are signs it might.

I work at Google. Google is considering flexible work for all its workers. This makes me consider working out of other locations (ex bangalore). If google starts offering this option, would create huge competitive advantage versus its other fortune 500 peers. They might eventually have to follow. This can lead to some demand going towards other tier 1 or tier 2 cities. For embassy to shift their strategy and build offices in such locations could take more time. There can be short term term (6-7 year. 7 years is short term for me when thinking about REITs) pain here.

Disc: Invested